Global| Oct 11 2016

Global| Oct 11 2016German ZEW Index Moves Higher

Summary

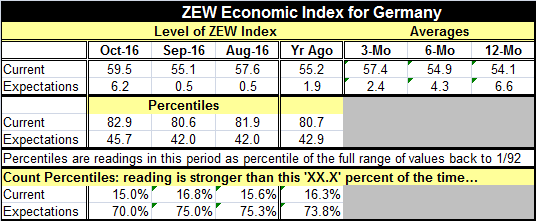

The closely watched ZEW expectations index rose by nearly 6 points in October, rising to 6.2 from 0.5 in September. The current index advanced to 59.5 from 55.1, a gain of about four points. These are not large monthly gains and they [...]

The closely watched ZEW expectations index rose by nearly 6 points in October, rising to 6.2 from 0.5 in September. The current index advanced to 59.5 from 55.1, a gain of about four points. These are not large monthly gains and they do not affect the signals from these two indicators very much. For the ZEW expectations component, the import of this month's signal is that it is not falling any more...at least for now.

The closely watched ZEW expectations index rose by nearly 6 points in October, rising to 6.2 from 0.5 in September. The current index advanced to 59.5 from 55.1, a gain of about four points. These are not large monthly gains and they do not affect the signals from these two indicators very much. For the ZEW expectations component, the import of this month's signal is that it is not falling any more...at least for now.

So high... so low...

Year-over-year both the current and expectations indices are higher each by less than three points. The current index is so strong that it has been higher historically only about 15% of the time. The expectations index is so weak that it has been higher historically about 70% of the time.

Swirling facts machine

Recent data and market events tell a story of swirling facts about the Europe and the euro area. In the U.K. today, the FTSE has hit a new intraday high; the pound (not-so-sterling) continues under downward pressure. Same store sales (like-for-like) rose in the U.K., but their gain is smaller than it was one month ago. For all of Europe, the Sentix index is on the same page as the German ZEW index as both are on a four month high. Yet, in France, Airbus is slowing its assembly line to generate only one new plane per month. Yesterday, Italy reported out stronger IP for the second straight month.

More question marks than exclamation marks in Asia ???>!

In Asia, conditions are touch and go with S&P reporting that Chinese banks need a recapitalization of about $1.7 trillion by 2020; but S&P sees China neglecting that need so it expect the actual requirement will be much larger down the road when it is finally addressed. In Japan, the current account surplus surged on falling exports as imports plunged. That's not a good sign for evolving domestic demand. Also raising warning flags about domestic sources of growth, a survey of Japanese retailers found them to be glum and not at all sharing the optimism of Mr. Kuroda at the BOJ.

Globalism's tentacles entangle all

As I said, events are swirling...in Europe, in Asia, and there are cross currents. Banks need help from Italy to China. The Fed seems to think that it can hike rates without any significant blowback effects from the international economy which it regards as stable. Oh? Is it? Actually it is until it isn't as the Fed found out last year when it put policy on hold in September on international concerns then too-soon thereafter signaled the 'all-clear,' and ramped up rates in December. Overseas markets came unraveled early in 2016 in the wake of the Fed's rate hike and its bombast about how many more hikes there were to come before yearend. Is the Fed able to think ahead and to see the foreign entanglements? Or is it unable to see the rough terrain until it actually stubs its toe on it?

ZEW outlook beyond Germany

The ZEW survey viewed, more expansively, also gives us assessments of other economies. The ZEW financial experts saw some improvement in their expectations in October for Germany, the U.K. and a small improvement for France. There was almost no change for Italy and a setback for the U.S. Only Germany saw a monthly increase in current conditions of 3 points or better on the month in its current assessment. The U.S. and Japan were both downgraded on their current performance.

Got inflation? Interest rates?

With oil prices higher, the ZEW experts are seeing inflation expectations rise nearly across the board (not in the U.S., however) and that expectation includes Japan (good news!). Short-term interest rate expectations are negative in absolute terms everywhere except in the U.S. and elsewhere expectations are being elevated from what they were in September and August. Long-term rate expectations are moving up as well.

Liking stocks

The ZEW experts are upbeat on equities in the EMU, Germany, the U.S., and the U.K. However, by historic standards their ranking of the equity sector across countries is still weak. They have shaved expectations for Japan, France and Italy.

Oil...OPEC?

It is not clear what the ZEW experts think about the new OPEC oil deal, but they generally expect oil prices to continue to rise. Their consensus on higher oil prices has been higher only 10% of the time. Currently, markets are going back and forth on whether the oil OPEC deal has real credibility or not even with Russia saying that it is in.

Summing up

On balance, October is a pretty good month for the performance of the German economy; expectations concerning the German economy have firmed but remain in the touch-and-go zone. In a broader context ZEW experts still see a great deal of global turbulence and uncertainty. Of course, they see continued growth. Only the U.K. has a negative expectation reading (that couples with a negative current reading, albeit one that has been improving). Still, we should not view growth as 'in the bag' with the ZEW expectation standings at or below their respective 30th percentiles of their historic positions everywhere: Germany, the U.S., Japan, the U.K., France, and Italy. The U.K. measure has been weaker only 2.4% of the time. Growth (expectations) is hardly in the cat-bird's seat.

ZEW members' consistency

The ZEW assessments for current conditions and for expectations roughly line up with the relative assessments that the financial experts offer for national stock markets with each explaining about 75% of the variance in stock value assessments cross-sectionally. The experts also have been true to making changes in their forecasts as the 12-month change in their assessments of current conditions and expectations explain even more, 78% to 86% in the change in the assessments of the national equity markets. What the ZEW experts think about economy clearly matters to what they think about current and future financial conditions. For now there is nothing here that is all that reassuring despite somewhat better assessments for Germany on the month. The ZEW experts remain wary.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief