Global| Jun 18 2013

Global| Jun 18 2013German Zew Expectations Make Slight Rise as European Auto Sales Struggle

Summary

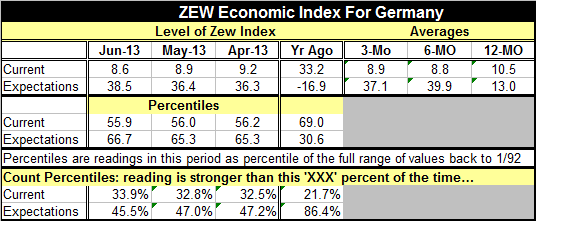

The Zew economic index for Germany saw its expectations component rise slightly to 38.5 from 36.4 in June. This is the second rise in a row for the expectations component, however, it is still substantially below the levels of 48.5 [...]

The Zew economic index for Germany saw its expectations component rise slightly to 38.5 from 36.4 in June. This is the second rise in a row for the expectations component, however, it is still substantially below the levels of 48.5 reached in March 2013 and 48.2 reached in February 2013. It is, however, still above the level of 31.5 reached in January 2013. Current conditions continue to slip and they have slipped for the third month in a row. At a level of 8.6 current conditions were last lower in February 2013.

The Zew economic index for Germany saw its expectations component rise slightly to 38.5 from 36.4 in June. This is the second rise in a row for the expectations component, however, it is still substantially below the levels of 48.5 reached in March 2013 and 48.2 reached in February 2013. It is, however, still above the level of 31.5 reached in January 2013. Current conditions continue to slip and they have slipped for the third month in a row. At a level of 8.6 current conditions were last lower in February 2013.

The current conditions reading, while at a low-seeming 8.6, is still are only stronger than this about 33% of the time. Expectations, at a reading of 38.5, are stronger than this about 45% of the time. So despite their respective numeric values the current reading is actually stronger relative to its history than is the expectations reading relative to its own history.

Investment professionals who contribute to this index rated stocks just slightly stronger in June compared to May. Bonds continue to receive a negative reading and one that's weaker in June compared to May. Expectations for profits in insurance stocks had one of the largest drops in June but this may be related to expected property and casualty claims with the extensive flooding that we've seen in central Europe in the past month. The outlook for profits in the vehicles sector and for consumption and trade industries has improved as has the outlook for profits in the construction sector. The outlook for profits in the services industry declined as it has been doing for the last several months. Still, if you look at expectations overall, profit expectations by industry in the business cycle are in an oscillating uptrend although there in a minor down-phase of that uptrend this month.

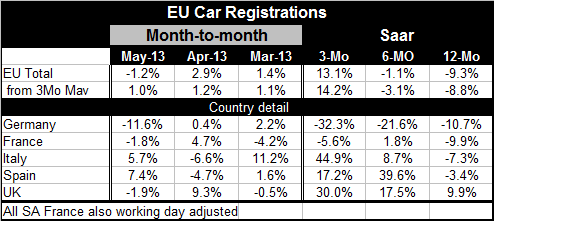

If we take the sector as an indication of confidence for the EU as a whole, conditions continue to be very weak but there is an improvement in vehicle registrations for the European Union as a whole as registrations are up 13.1% at an annual rate over three months. Italy shows a strong gain; that is mostly due to an incentive program that has been in place and is now expiring.

On balance the conditions in Germany as depicted by the Zew survey are more or less stable. The positioning of the two key indices is roughly consistent with the kind of ongoing recovery that we've seen in Germany. There's little reason from this survey to be more optimistic or more pessimistic about its speed. However, the results for automobile registrations for the economic union as a whole continue to paint a picture of the consumer that is still struggling to regain some confidence. The European auto industry is beleaguered just about everywhere except in the UK, where auto sales have held up remarkably well during the entire period of economic sluggishness.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief