Global| Jan 20 2015

Global| Jan 20 2015German ZEW Assessment Bounces Back

Summary

The ZEW financial experts contributing to the responses in the ZEW index are upbeat in January. The current index has jumped to 41.2 this month from 32.4 in December; it is stronger only 15% of the time. Since January 1994, the [...]

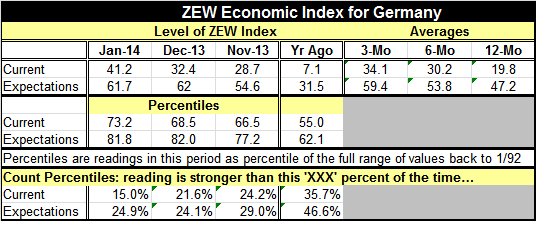

The ZEW financial experts contributing to the responses in the ZEW index are upbeat in January. The current index has jumped to 41.2 this month from 32.4 in December; it is stronger only 15% of the time. Since January 1994, the current index has jumped by more in one month only 24 times. The expectations index was generally steady on the month, edging slightly lower to 61.7 from 62 in December. At its present standing, that index is higher only about 25% of the time. The ZEW financial experts are decidedly upbeat on the German economy.

The ZEW financial experts contributing to the responses in the ZEW index are upbeat in January. The current index has jumped to 41.2 this month from 32.4 in December; it is stronger only 15% of the time. Since January 1994, the current index has jumped by more in one month only 24 times. The expectations index was generally steady on the month, edging slightly lower to 61.7 from 62 in December. At its present standing, that index is higher only about 25% of the time. The ZEW financial experts are decidedly upbeat on the German economy.

Low oil prices have had a positive influence on German consumers, although, because of taxes, Germans will not see the same impact as American consumers and the declines in the euro exchange rate will further blunt the impact of the decline for the German consumers. Still, there is a sense of improvement in their welfare that the ZEW financial experts detect.

The German PPI fell by 0.6% in December as the CPI fell by 0.5%, underscoring that the energy impact in Germany is still quite significant. German consumer prices are up 0.2% year-over-year and producer prices are lower by 1.6% on that basis.

Despite some German optimism, the IMF today cut its outlook today for global growth in 2015. The IMF, which previously saw 3.8% growth, is now trimming that back to 3.5%. China has recorded fourth quarter growth of 7.3%, better than expected but still part of an ongoing Chinese economic slowdown.

Germany's ZEW pick up is a milder reaction than the recent ramp up in the U.S. consumer sentiment index. However, put in historic context, the German index is quite a bit stronger than the U.S. consumer-focused index. Still, we are seeing economic climate assessments of various sorts show improvement on the back of lower oil prices even as growth under-performs.

Global cross currents are still very much in play. This morning oil prices (Brent) hovered at $49/bbl without any conviction whether prices could stay or would go lower. Supply/demand dynamics for oil are still poor. Consumers `get it,' they know there is a benefit for them in the lower prices. But the impact on the various global economies will be different, depending on the energy import-reliance of the local economy and depending on its energy efficiency.

The weak oil prices will also enhance the European Central Bank's undershoot of its price target. Without apology, the ECB has clung to targeting headline inflation. Policymakers will have to live with the shortfall this oil price drop that will exacerbate the ECB target miss. The ECB is planning to launch some sort of QE operation to defend its price target. Euro foreign exchange markets and global capital markets are already bracing for it. However, with rates so low, can QE be effective? It seems that the ECB- stalled by persistent German opposition- has finally paved the way for a policy whose time for effectiveness has passed. Still, we see no evidence that the German financial experts have any concern that the upcoming push of QE by the ECB could undermine its financial standing. If the ECB buys government bonds when some of the key national markets already have negative yields, what will happen if the program is at all successful and the euro area economy grows faster pushing interest rates higher on the bonds the ECB has accumulated to jump start and implement QE? The ECB has no cushion to push yield lower and make a profit on its earliest purchases. The ECB has very little opportunity to make any money off of QE before bond prices turn lower. I would have expected some of the ZEW experts to less upbeat on QE and on the German outlook for this reason. I guess they are not yet looking that far ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief