Global| Dec 09 2020

Global| Dec 09 2020German Trade Surplus Widens As Exports Outpace Imports...Again

Summary

The chart, presenting the year-on-year trade flow percent changes and the monthly trade balance, offers a good perspective on the forces and timing of events affecting the German trade situation. The surplus reached its low point in [...]

The chart, presenting the year-on-year trade flow percent changes and the monthly trade balance, offers a good perspective on the forces and timing of events affecting the German trade situation. The surplus reached its low point in April as activity was shut down and since then has risen as the year-on-year gains in exports and imports have risen. German exports fell in April much harder than German imports and Germany was generally less affected by the virus that its EMU trade counterparties. But after a few months of lagging well behind imports, exports (and export growth) have ‘caught up’ and continue to track imports at an annual growth rate that is just a few ticks weaker. Both exports and imports in October are growing slower than they had been prior to the spread of the virus. The German trade surpluses are slightly lower as well. The chart displays well the impact of the virus, the hit to activity, the rebound, and then, the sense of the rebound being incomplete. That is an ongoing issue as the level of the trade surpluses and growth of exports and imports are below their pre-pandemic levels and trends and seem to be leveling out at that lower pace.

The chart, presenting the year-on-year trade flow percent changes and the monthly trade balance, offers a good perspective on the forces and timing of events affecting the German trade situation. The surplus reached its low point in April as activity was shut down and since then has risen as the year-on-year gains in exports and imports have risen. German exports fell in April much harder than German imports and Germany was generally less affected by the virus that its EMU trade counterparties. But after a few months of lagging well behind imports, exports (and export growth) have ‘caught up’ and continue to track imports at an annual growth rate that is just a few ticks weaker. Both exports and imports in October are growing slower than they had been prior to the spread of the virus. The German trade surpluses are slightly lower as well. The chart displays well the impact of the virus, the hit to activity, the rebound, and then, the sense of the rebound being incomplete. That is an ongoing issue as the level of the trade surpluses and growth of exports and imports are below their pre-pandemic levels and trends and seem to be leveling out at that lower pace.

Monthly data show that exports are outpacing imports again. On monthly changes, exports are growing faster than imports for two months in a row as well as for five times in the last six months. Exports are rallying back from what were huge shortfalls to import growth in March and April.

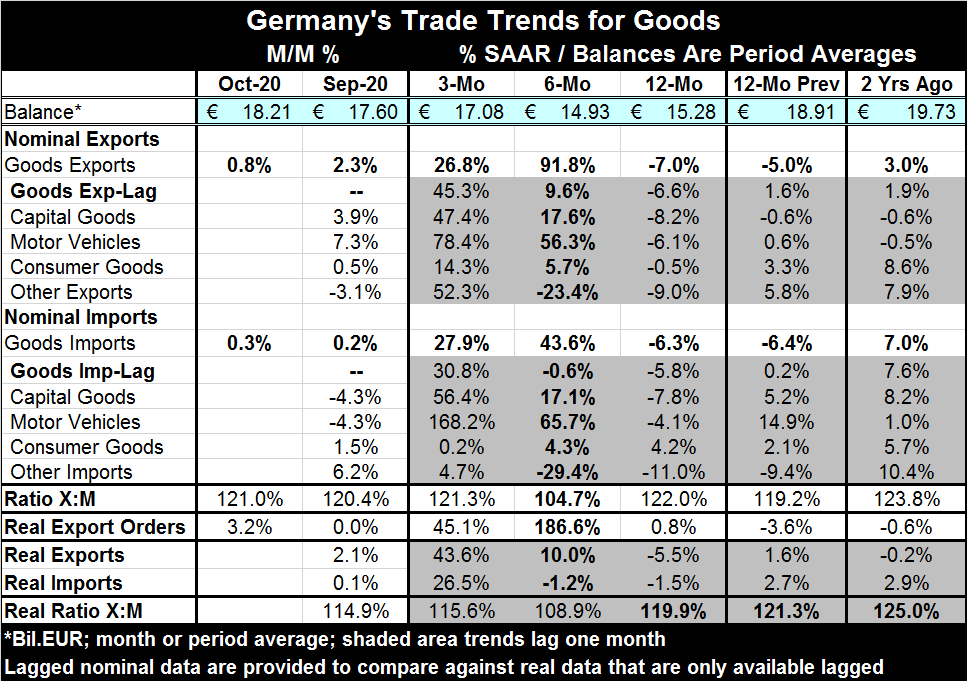

Both exports and imports show declines over 12 months, extremely sharp increases over six months, and slower, but still substantial double digit, growth over three months.

These data are through October and there is another economic slowdown period from actions taken to slow the virus spread in November. However, the impact on economic data will be much less than it was in April.

More detailed lagged data trends

On lagged trends, German export and imports mirror their respective headlines that themselves are similar to the unlagged trends. Nearly all German export and import detailed components show growth declines over 12 months. But the six-month changes on that lagged calculation take the base for that calculation back to March before much of the trade disruption. As a consequence, six-month changes are largely tempered with lagged overall exports up at a 9.6% annual rate and lagged import changes over six months falling at a 0.6% annual rate. And as a result of that shift, lagged three-month growth rates are slightly above their unlagged counterparts as the rebound has been slowing making the more recent three-month calculations weaker. Line item trade flow categories of exports and imports are all accelerating sharply over three months and accelerating over six months compared to 12 months with the exceptions of the ‘other’ (export and import) categories.

On balance, we see the timing dominating the export and import growth numbers and the two flows (exports and imports) being affected more of less equally by the disturbance.

These calculations remind us how much port activity (ports being opened or closed or impaired) will affect trade flows on both sides of the ledger. And as the flows react overtime, we also see how the virus is impacting trading partners more or less the same. As Germany has experienced a new setback with the virus in November so has much of Europe and we expect a minor replay of what we saw early in the year. We can see that manufacturing has been adversely affected by recent anti-virus actions and that implies knock-on effects for trade. However, as of December some of the virus slowdown-actions are being dismantled and soon growth should be more normalized. Right after that, the process of immunization should begin. We do not expect any significant economic changes to be in gear due to vaccinations until well after mid-year.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief