Global| Jun 09 2016

Global| Jun 09 2016German Trade Surplus Moves Higher: Fiddle Dee Dee Europe

Summary

German trade flows came up lame in April as exports were flat and imports fell by 0.2%. These performances follow a 1.9% gain for exports in March and a 2.3% drop for imports. Exports grow but imports stay slow or worse Suddenly [...]

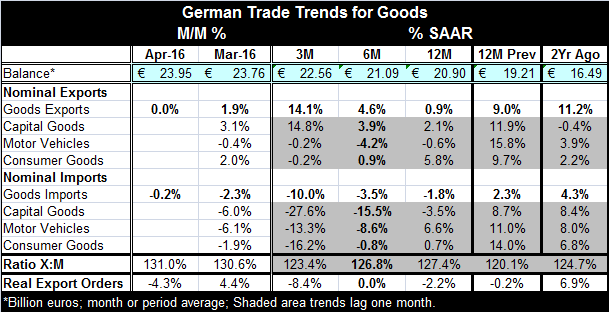

German trade flows came up lame in April as exports were flat and imports fell by 0.2%. These performances follow a 1.9% gain for exports in March and a 2.3% drop for imports.

German trade flows came up lame in April as exports were flat and imports fell by 0.2%. These performances follow a 1.9% gain for exports in March and a 2.3% drop for imports.

Exports grow but imports stay slow or worse

Suddenly (Poof!) out of thin air German exports have lift off. They are accelerating from a 0.9% pace over 12-month to 4.6% over six-month to a pace of 14.1% over three-month. Imports, however, are hopelessly mired in a declining phase. They are net lower by 1.8% over 12-month, falling at a 3.5% pace over six-month and falling at a 10% pace over three-month. Germany is not spreading the `joy' of its economic performance across Europe or the world by increasing its imports. Far from it. The German economy is ploughing ahead. German exports are now actually surging but the German import appetite is like that of an anorexic fashion model.

Widespread import weakness

We could blame weak German imports on falling oil prices in the past, but oil prices are firming. And import detail (where data lag by one month) show that over three months German imports are falling for capital goods (at a -27.6% annual rate!), for motor vehicles (-13.3% annual rate), and for consumer goods (-16.2% annual rate).

Export/Import relative performance

The current ratio of exports to import is up to 1.31 (131%). This is its highest ratio value since May 2004 (more than a decade!). Germany's trade balance, already one of the largest in the world, especially relative to GDP, continues to hold at a high level and even to work higher.

Forgotten goals and mechanisms

The principles of economic adjustment are being undermined by the hijacked global monetary system and by countries' failures to implement correct policies at home. While there is a focus on the risk of excessive monetary policy, there is nothing being said about the forced diet off of fiscal policy. There is no debate that fiscal policy, too, has been overused. But the sharp and near-global shut off of the fiscal channel at a time of diminished growth and slack global demand has left global conditions in the hands of a private sector that itself is struggling with change and economic pressures-and with its adjustment mechanism spigots turned to an `OFF' setting. As a result, countries with surpluses are keeping them or making them larger and countries with deficits continue to keep and run deficits. There is no adjustment. Funds continue to transfer into low wage high savings (low spending) regions damping the global growth multipliers and steeping the slope of the hill we need to climb to achieve growth.

You can't use the pump because the vandals stole the handle

There is no adjusting exchange rate mechanism; for all intents and purposes, it does not exist. Surplus country currencies do NOT rise to choke off current account surpluses and restore balance. Deficit country currencies (hint USA) do not fall (enough or consistently enough). Exchange rates have become the dominion of various nations' economic policies and are used to secure export-led economic growth- not as a cyclical mechanism to readjust trade balances when they get out of kilter. In the case of the euro area, Germany is deeply embedded in a secure economic zone, nestled inside a troubled area so that the currency its shares with these struggling nations reflects their weakness instead of its strength. Germany benefits from being in a weak currency zone: its exports are made stronger; its import weaker. Meanwhile, Germany takes no countervailing domestic actions to diminish its surplus even though EU rules demand that it do so. Germans are good at pointing out other countries' shortcoming and at the same time ignoring the rules it finds inconvenient for itself. And that is what we see in the EMU and Germany.

ECB policy options (buy a lottery ticket and pray)

At the ECB (today!), we hear Mario Draghi begging for structural change and that is only because he cannot beg for the use of fiscal policy when countries are over their Maastricht (sounds like, mass-trick) allotment. You can believe that Germany is watching everyone else's budget very carefully while its own pot-belly of current account surplus spills over its own belt.

ECB credibility is being eroded

Germany sees ECB credibility as damaged and as damaged by its novel policies and bloated balance sheet size. Much of the rest of Europe sees ECB credibility damaged too but sees it as damaged by three years of inability to hit its inflation target while Germany blocked every attempt by the ECB to use an innovative policy. Germany refuses to admit that blood of ECB failure is all over its hands. In fact, most Germans do not even see ECB policy as `failed' since the ECB (successfully!) is keeping inflation below 2% and to them all is fine even though it is not the ECB mandate. Some Germans (astonishingly!) think that `to regain credibility' the ECB should boost interest rates back to `normal' now! Other analysts look at EMU inflation and worry about deflation. Germans call the inflation environment `moderate'- not even low! Today Mario Draghi is warning that Europe could be scarred permanently by this period of too-low growth and inflation. But German unemployment is at a reunification low. Germans do not feel the pain. They have a `get out of deflation-free card.' They have created a Shangri-la-la-la economy that thrives even in the moribund euro area.

Germany's rigid and selective view of rules hurts EMU

When the dust settles, Germany wins. Its economy is meant to operate in first gear and is still pounding ahead - inch by centimeter. And yet because of Angela Merkel, it has absorbed a sharp rise in migrants and now various crime problems including backlash hate crimes being reported in Germany. Apart from this one act of self-sacrifice -that many Germans seem to oppose and that has been abruptly slowed- Germany is doing little (actually nothing) to make the way easier for fellow EMU members despite its own cushy environment. Germany refuses to obey rules it is violating that could help fellow EMU members. Obeying the rules on deficit reduction would help. And that will happen... when pigs fly and all the beer gardens close and probably not before.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief