Global| Jun 09 2008

Global| Jun 09 2008German Trade Surplus Bulges Again in April

Summary

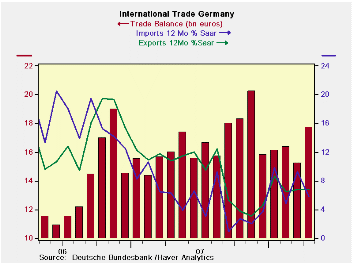

Despite weakening industrial output and fast decelerating orders German trade flows produced a larger surplus again in April. Exports rose by 1.2% in the month as imports dropped by a large 2.1%. Over the last three months import [...]

Despite weakening industrial output and fast decelerating

orders German trade flows produced a larger surplus again in April.

Exports rose by 1.2% in the month as imports dropped by a large 2.1%.

Over the last three months import growth is off at an 8% pace, while

for exports growth has decelerated from 6.8% Yr/Yr to 5% over six

months to 1% over 3-months.

The month’s rise in the surplus does not repeal the trend of

fading German export orders. German export trends themselves are still

fading. But the trade balance is, as the name suggests, a balance

between what is bought and what is sold. In April although exports are

still part of a declining trend, imports contracted and did so sharply,

thrusting the trade scene into a surplus.

Weak growth at home is another factor that will come to be

caused by a weakness in exports since Germany’s whole economy is

reliant on trade and on its ability to export. The signals from

weakening orders are due to hit the economy in time. For this month

there is nothing inconsistent about the broad export slowdown trend and

the rise in the trade surplus. The export slowdown is still in place.

| German Trade trends for goods | |||||||

|---|---|---|---|---|---|---|---|

| m/m% | % Saar | ||||||

| Apr-08 | Mar-08 | 3-M | 6-M | 12-M | 12-M Prev | 2-Yr Ago | |

| Balance* | €€ 17.73 | €€ 15.25 | €€ 16.44 | €€ 16.92 | €€ 16.93 | €€ 14.41 | €€ 12.66 |

| EXPORTS | |||||||

| All Exports | 1.2% | -0.8% | 1.0% | 5.0% | 6.8% | 18.3% | 36.1% |

| Capital Goods | -- | -0.8% | 2.8% | 0.6% | 5.0% | 7.3% | 10.7% |

| Motor Vehicles | -- | 0.8% | 6.0% | 5.0% | 7.2% | 10.1% | 9.8% |

| Consumer Goods | -- | -2.3% | 16.7% | 5.6% | 10.2% | 4.3% | 15.3% |

| IMPORTS | |||||||

| All Imports | -2.1% | 0.6% | -8.0% | 8.3% | 5.8% | 12.5% | 34.0% |

| Capital Goods | -- | 2.9% | 44.8% | 7.0% | 8.2% | -3.3% | 23.2% |

| Motor Vehicles | -- | 4.3% | 57.7% | 15.0% | 9.9% | 9.3% | 9.8% |

| Consumer Goods | -- | -4.1% | 6.7% | -2.0% | 0.7% | 3.6% | 21.3% |

| *Eur Blns; mo or period average; Shaded area trends lag one Month | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief