Global| Jul 09 2020

Global| Jul 09 2020German Trade Rebounds

Summary

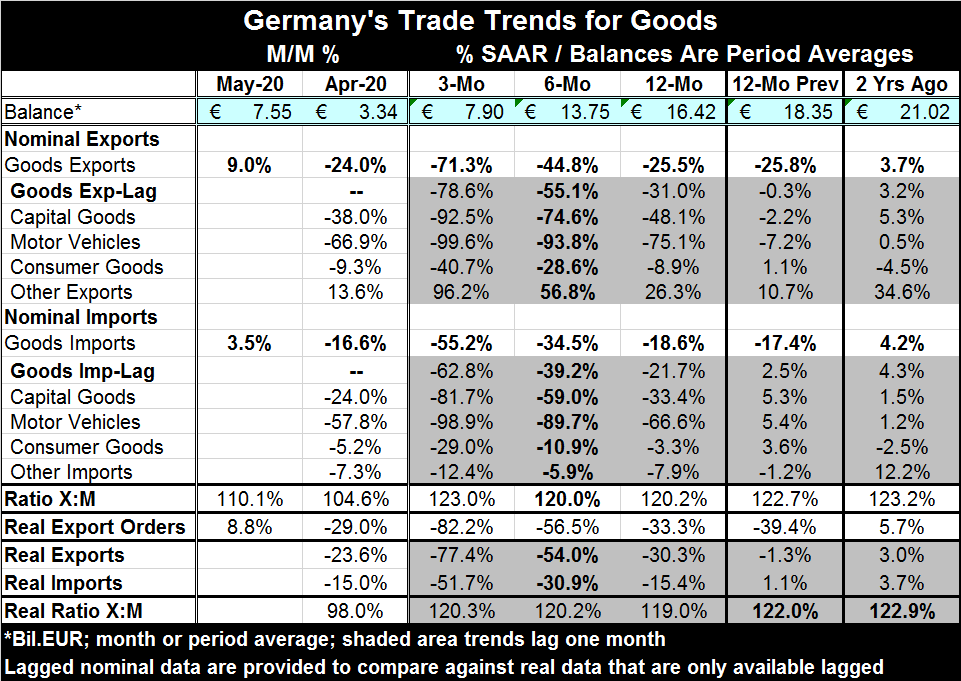

German exports gained sharply in May but not quite as sharply as expected, rising by 9.0% month-to-month. Despite that surge, exports are still declining at accelerating rates from 12-months to six-months to three-months. Imports also [...]

German exports gained sharply in May but not quite as sharply as expected, rising by 9.0% month-to-month. Despite that surge, exports are still declining at accelerating rates from 12-months to six-months to three-months.

German exports gained sharply in May but not quite as sharply as expected, rising by 9.0% month-to-month. Despite that surge, exports are still declining at accelerating rates from 12-months to six-months to three-months.

Imports also picked up but less robustly, gaining 3.5% month-to-month and also showing a steady decelerating pattern across sequential periods.

The chart shows the dramatic drop off on the German trade surplus as the virus struck. Similarly, the 'revival' in exports and imports is weak. German real orders also are steadily decelerating point to a still difficult outlook.

Real exports and real exports flows that lag one month also show decelerating trends.

The new Baltic dry index backtracked on the day but still retains an upswing. The outlook for global trade is improving, but it is not robust or even really dependable. Just today the BOJ reduced its assessment of conditions for all nine regions. Tokyo is experiencing a pick-up in virus infections as well.

The new Baltic dry index backtracked on the day but still retains an upswing. The outlook for global trade is improving, but it is not robust or even really dependable. Just today the BOJ reduced its assessment of conditions for all nine regions. Tokyo is experiencing a pick-up in virus infections as well.

Globally economic data are showing some revival or at least less weakness. While some reports, like PMI indexes, has showed some strong upward movements. The levels of the PMI readings continue to show moderation. The real problem is the new outbreak of virus that has global dimensions. Despite some sharp recovery on some statistics, the revival of the virus promises to blunt the strength of the budding recovery globally. That is the latest challenge to growth. For now, exports are showing some revival. But Germany is extremely export dependent and will need a robust international environment to drive growth. That still seems some way off.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief