Global| Jul 08 2014

Global| Jul 08 2014German Trade Flows Slow; Is Germany Slowing?

Summary

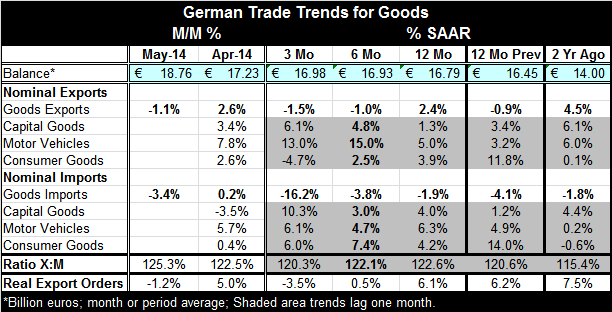

Germany's trade flows have slowed with both exports and imports falling in May. Exports fell by 1.1% following a strong 2.6% April gain. Imports fell by an outsized 3.4% after climbing by a skinny 0.2% in April. Import growth appears [...]

Germany's trade flows have slowed with both exports and imports falling in May. Exports fell by 1.1% following a strong 2.6% April gain. Imports fell by an outsized 3.4% after climbing by a skinny 0.2% in April. Import growth appears to be in trouble.

Germany's trade flows have slowed with both exports and imports falling in May. Exports fell by 1.1% following a strong 2.6% April gain. Imports fell by an outsized 3.4% after climbing by a skinny 0.2% in April. Import growth appears to be in trouble.

Both German exports and imports are showing withering trends. Imports, however, are withering at a much faster rate. Imports are declining at a 16.2% annual rate, a larger decline than the -3.8% pace over six months and the -1.9% pace over 12 months. For exports, goods exports are up by 2.4% over 12 months, down at a 1% annual rate over six months and down at 1.5% annual rate over three months. For exports, the weakness is possible to mistake the sluggishness because the recent declines are so shallow. But for imports, weakness represents outright and, in some cases, severe declines.

We have evidence on export and import flows by category, lagging one month. For exports, the category data we have is through April, when exports were strong. At that time, motor vehicles exports rose month-to-month by 7.8%, capital goods exports rose by 3.4% and consumer goods exports rose by 2.6%. Imports were weak in April, rising only by 0.2%; by category capital goods imports fell by 3.5%, motor vehicles imports rose by 5.7% and consumer goods imports rose by 0.4%.

Looking at the sequential growth rates for export categories, we find somewhat of a step up of growth rates for capital goods, culminating in a 6.1% annual rate over three months. Motor vehicles stepped up their pace to double digits over both three months and six months. However consumer goods slipped from a 3.9% growth rate over 12 months to drop at a 4.7% annual rate over three months.

On the import side, capital goods imports continue strong growing at a 10% annual rate over three months. Motor vehicles imports are strong at a 6.1% annual rate and consumer goods imports rose at a 6% annual rate staying steady. Clearly the import weakness was in other categories.

Although the German exports don't show the degree weakness of imports, since the German economy is geared to export, the export weakness is perhaps somewhat more disturbing. Real export orders fell in May but only after a sizable jump in April. Still, they are declining at a 3.5% annual rate over three months, a sharp change from the 6.1% gain over 12 months.

Germany, however, shows strong export trends within the euro area where exports rose by 4.2% year-over-year. However, Germany still does not play the role of locomotive within the monetary union. Its imports from other euro area members fell by 3.2% over the last 12 months. German exports to European Union members that were not members of the EMU rose by 9.4% while imports from this group rose by 7%. German exports to destinations outside of the EU rose by a small 2.1% while imports from destinations outside that union fell by 0.8%.

There has been recent and unexpected weakness in German industrial production, retail sales and now, trade. Since Germany is an export oriented economy, the weakness in its exports is somewhat troubling. However, the extremely sharp drop in imports is almost equally troubling because of its sharpness. The United Kingdom, not part of the single currency arrangement, also reported today a drop in its industrial production that was not expected. Germany's drop in industrial production, reported yesterday, was not expected. It's hard to say where this weakness has come from. In the case of Germany, we do have an economy that is plugged into trade relations with Eastern Europe and Russia. These flows may be affected adversely by the ongoing tensions with Russia and in Ukraine. At this point, it's hard to pin down the cause of the weakness. But it is not out of the blue. It is somewhat in line with weakness we've seen reported last month from the Ifo and the ZEW surveys. At that time, the more focused GfK consumer survey had showed continued strength on the part of consumers. However, the sharp drop in imports this month may bring that into focus and into the question. Clearly, there has been some slowing in Europe and we need to keep an eye on it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief