Global| Jul 19 2004

Global| Jul 19 2004German & Swiss PPI Rise Modestly; Inflation Potential Unclear

Summary

Times of economic transition are often the hardest periods to interpret as they exhibit mixed tendencies. So it was last week that we published here almost contradictory comments about CPI inflation in various countries. In some [...]

Times of economic transition are often the hardest periods to interpret as they exhibit mixed tendencies. So it was last week that we published here almost contradictory comments about CPI inflation in various countries. In some places, it remains quiescent, while elsewhere, it is picking up noticeably. So one can't generalize about the present evolution of price trends

Today brought PPI data for Germany and Switzerland for June. In these countries as well as the US, producer prices have firmed. But the inflationary potential in these figures varies widely. German and Swiss manufactured goods prices are rising, but they remain on modest uptrends: 1.5% year-on-year in Germany and 1.4% in Switzerland. But in Germany this pace is actually a bit slower than what prevailed at the end of 2003. Energy accounts for that, as those prices have moderated considerably in Germany since late last year. Excluding energy, German factory goods prices are also on a firming trend, although they were up just a modest 1.3% in June from a year earlier. Swiss producer prices look to be picking up across many categories, but all at a very modest pace.

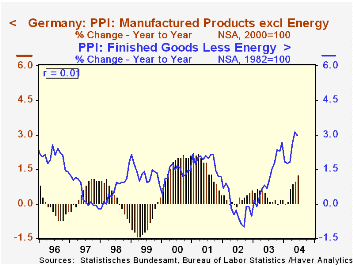

US factory prices are on a rampage by comparison, gaining at a 4%-5% pace through June, year-on-year, measured as total manufacturing industry prices or total finished goods prices. Energy accounts for a notable portion of the advance in finished goods, as seen in the table below, but even removing it, we are still left with 3% year-on-year in recent months. And food appears to explain a good bit of that. Other price moves show wide variation. So, even though the total US PPI is showing some strength in the aggregate, it is quite uneven among sectors, so that the overall inflation potential in these wholesale prices is far from clear. Moreover, as the accompanying chart shows, there is virtually no correlation of producer prices excluding energy in Germany and the US.

| June 2004 | May 2004 | Apr 2004 | 2003 | 2002 | 2001 | |

|---|---|---|---|---|---|---|

| Germany: Manufacturing | 1.54 | 1.64 | 0.86 | 1.76 | 0.59 | 0.10 |

| Germany: Manufacturing ex Energy |

1.27 | 0.98 | 0.88 | 0.20 | 0.59 | 0.40 |

| Switzerland: Manufacturing | 1.40 | 1.50 | 1.10 | 0.50 | -0.50 | 0.00 |

| US Manufacturing | 4.92 | 5.60 | 4.04 | 2.76 | 1.82 | -2.01 |

| US Finished Goods | 3.99 | 5.00 | 3.66 | 3.96 | 1.16 | -1.65 |

| US Finished Goods ex Energy |

2.97 | 3.10 | 2.56 | 2.65 | -0.54 | 1.16 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief