Global| Aug 08 2007

Global| Aug 08 2007German Surplus in Trade Remained in June but was Narrowed Sharply by Surging Imports

Summary

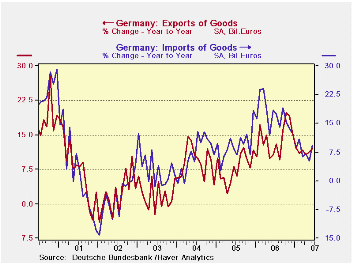

German trade trends are showing sharp wild swings in their interval growth rates. The trends on the accompanying chart show a more stable longer pattern from early 2006 through early mid-2007 import trends worked lower. Export trends [...]

German trade trends are showing sharp wild swings in their interval growth rates. The trends on the accompanying chart show a more stable longer pattern from early 2006 through early mid-2007 import trends worked lower. Export trends worked lower from October 2006 through April of 2007. At mid-year German exports are showing some tendency for firmness while imports have jumped sharply. German chemical and machinery exports are continuing to hold up.

For the quarter exports have risen by 2.5% compared to a drop of 1.2% for imports. While these are nominal figures the inflation adjusted figures should show a contribution of net exports to GDP growth in 2007-Q2. But the surge in imports later in the second quarter could be laying the groundwork for a lasting import gain that could make net exports a drain on Q3 GDP. It is too soon to know about such things, but one thing Germany is continuing to look for is for the consumer sector to kick in to help out with second half growth. With the broad inflation adjusted euro at such a peak, more domestic demand help could be essential to maintaining the growth trend, especially if the import surge lasts.

| m/m% | % Saar | ||||

| Jun-07 | May-07 | 3M | 6M | 12M | |

| Balance* | €€ 14.88 | €€ 17.39 | €€ 16.04 | €€ 15.70 | €€ 15.30 |

| EXPORTS | |||||

| All Exports | 2.1% | -0.9% | 8.6% | 6.4% | 12.1% |

| Capital goods | -- | 1.0% | -6.6% | -6.5% | 9.4% |

| Motor Vehicles | -- | 3.4% | 1.9% | 14.0% | 7.7% |

| Consumer Goods | -- | -5.8% | -0.3% | 7.2% | 13.0% |

| IMPORTS | |||||

| All Imports | 6.7% | -3.6% | 15.8% | 6.0% | 9.2% |

| Capital goods | -- | -1.9% | -25.8% | -10.4% | 6.5% |

| Motor Vehicles | -- | 6.4% | 20.1% | 8.2% | 16.9% |

| Consumer goods | -- | -7.3% | -29.0% | -2.1% | 1.3% |

| *Billions of euros; monthly or period average; Shaded area trends lag one month | |||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief