Global| Sep 05 2008

Global| Sep 05 2008German Sector Trends are Clear and Weak

Summary

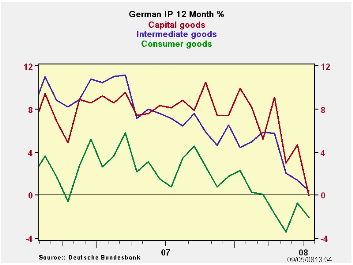

German statistics have been weakening and the weakness in orders reported yesterday was a shock to some. Today the process of being shocked continues with stark and unexpected weakness in German industrial output. Output is off for [...]

German statistics have been weakening and the weakness in orders reported yesterday was a shock to some. Today the process of being shocked continues with stark and unexpected weakness in German industrial output. Output is off for the second time in two months and by a severe 1.8% m/m. Yr/Yr the drop is -0.6%. MFG IP is off by 2% in the month. Sequential growth rates generally show that the weakness is still cumulating (construction and consumer spending are exceptions of sorts). In the new quarter to date (Q3) output is falling at a 13.3% annual rate, led by weakness in capital goods. While the drop in consumer goods output is the most severe on a Yr/Yr basis, the deceleration is the greatest for capital goods where output seems to stay so high for so long. This it turns out was mirage like Wiley Coyote standing on thin air waving to the Road Runner before gravity took hold. German capital goods output too seemed to defy the gravity and domestic weakness and the overly strong euro. But now that resilience is a thing of the past.

German authorities have tried to argue that the weakness is partly due to the start of the school year. But they hasten to add the trends are going to be lower. There should be fewer denials of encroaching weakness in Germany since the bottom fell out of orders and IP and that has happened just over the past two days.

Things change. And they did not elect either Obama or McCain.

Still the ECB has decided to tighten up its collateral acceptance parameters, and that action will impair liquidity in the Zone and at a time when economic weakness seems to be taking greater hold. In the US two speeches, one by Reserve Bank president Yellen, the other by Reserve Bank president Fisher, talked in less than glowing terms about the US economy. Fisher worries more about inflation prospects while Yellen reports that the next move by the Fed is more likely to be up than down but she reiterated Fed fallibility. Central bankers clearly are not plugged into the news that reveals accelerating weakness. Even the Bush Administration today took the opportunity to say that a new stimulus program was not needed.

While the economic data are worsening central banks seem to be taking the opportunity to let weaker growth drag inflation lower, rather than to move to offset the weakness. This is done by ignoring the weakening (Trichet), denying it (Germany, at least so far) or by making inflation the greater threat (Richard Fisher, and others).

| Total German IP | |||||||

|---|---|---|---|---|---|---|---|

| Saar exept m/m | Jul-08 | Jun-08 | May-08 | 3-mo | 6-mo | 12-mo | Quarter-to-Date |

| IP total | -1.8% | 0.1% | -1.8% | -13.3% | -8.0% | -0.6% | -13.3% |

| Consumer | -1.7% | 0.4% | -0.3% | -6.2% | -8.6% | -2.1% | -8.8% |

| Capital | -3.7% | 1.7% | -3.7% | -21.0% | -11.7% | -0.1% | -21.2% |

| Intermediate | -0.6% | -0.5% | -1.0% | -8.2% | -3.4% | 0.4% | -7.5% |

| Memo | |||||||

| Construction | -2.0% | -2.4% | 2.4% | -8.2% | -23.1% | -2.8% | -15.8% |

| MFG IP | -2.0% | 0.5% | -1.9% | -13.1% | -7.8% | -0.2% | -13.3% |

| MFG Orders | -1.7% | -2.6% | -1.3% | -20.0% | -15.2% | -4.1% | -20.7% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief