Global| Aug 03 2009

Global| Aug 03 2009German Retail Sales Take A Dive - Without The Swan

Summary

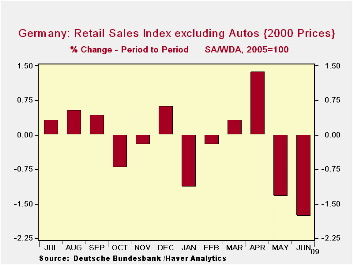

The FACT: German ex-auto retail sales fell sharply in June, the second sharp drop in a row after posting a strong gain in April. THE REVERSAL: After a terrible January German non-auto retail sales have been on a nice strong recovery [...]

The FACT: German ex-auto retail sales fell

sharply in June, the second sharp drop in a row after posting a strong

gain in April.

THE REVERSAL: After a terrible January

German non-auto retail sales have been on a nice strong recovery path

as sales cut their decline of over 1% (m/m) in January to drop of -0.2%

in February then rose in March and rose strongly in April by 1.8%. That

was before this new episode in which they have posted back to back

large drops in May and in June.

THE IMPACT: Despite the disappointing

numbers in the last two months, earlier increases will hold retail

sales ex-autos flat in real terms; the nominal numbers will rise by

1.7% at an annual rate in Q2.

THE PARADOX: The retail sales report was a

bitter one for June and it comes in a day that Europe-wide and German

MFG PMI results we better-than-expected. The EMU report registered its

second highest month-to-month gain in its relatively modest history-

still an impressive jump. The German MFG reading rose to 45.7 on its

largest point gain ever, reaching a ten-month high, although still

indicating a declining state. All of that is impressive.

THE UPSHOT: So the day’s reports are mixed.

In Europe and in Germany manufacturing is making a strong step toward

recovery. Still, the level of the reading tells us that the strong

month-to-month improvement leaves industry output contracting. The

retailing sector that had begun to look like it was in a state of

repair is now looking much worse. While the quarter will not end too

badly for German retail sales that is because of past strength. The

recent collapse in retail sales should be a warning to policymakers

about complacency – even in the face of a manufacturing turnaround that

is in progress.

THE FUTURE: The new bout of retail weakness

puts retail sales in a deep hole from which to start off in 2009-Q3.

For example if German retail sales do not rise in July they will carry

a growth rate off the previous quarter of -6.4% at annual rate in Q3

over Q2. This is a big inherited weakness that is unlikely to spur any

increase in the output of consumer goods in Germany – setting aside the

auto sector where special incentives are having a positive impact. The

optimistic spin here is that all of consumer attention is going into

the auto incentives and that is leaving other retail behind. Things may

not be as weak as they seem by looking at non-auto retail sales alone.

That may be true, but that is only a matter of solace if attention and

spending in the non-auto sector turns up, because it is starting off Q3

in a really deep hole. The auto sales revival in Q2 will only make it

that much more difficult to get Q3 sales higher. In other words if the

auto incentives don’t stay in place and do not continue to have a

strong positive impact, German overall retail sales will become a heavy

negative weight on German GDP in Q3.

| German Real and Nominal Retail Sales | QTR | |||||||

|---|---|---|---|---|---|---|---|---|

| Nominal | Jun-09 | May-09 | Apr-09 | 3-MO | 6-MO | 12-MO | Year Ago | Saar |

| Retail Ex auto | -1.6% | -1.4% | 1.8% | -4.7% | -3.9% | -2.2% | 1.6% | 1.7% |

| Real | ||||||||

| Retail Ex auto | -1.8% | -1.3% | 1.4% | -6.9% | -5.5% | -1.9% | -1.7% | 0.0% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief