Global| Jun 30 2016

Global| Jun 30 2016German Retail Sales Rebound

Summary

German retail sales ex-autos rose by 0.8% in May after a skinny gain of 0.1% in April. The three-month growth rate is zero. Over six-months, sales are up at a 0.5% pace. Over 12-months, sales are up at a 0.7% pace. Sales are [...]

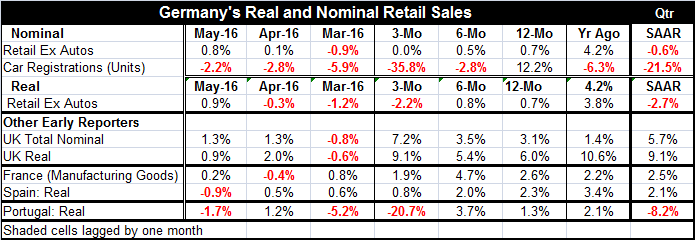

German retail sales ex-autos rose by 0.8% in May after a skinny gain of 0.1% in April. The three-month growth rate is zero. Over six-months, sales are up at a 0.5% pace. Over 12-months, sales are up at a 0.7% pace. Sales are decelerating on this timeline albeit at a very slow pace of erosion. And real retail sales (ex-autos) also are on a decelerating path with the recent three-month growth rate showing a decline.

German retail sales ex-autos rose by 0.8% in May after a skinny gain of 0.1% in April. The three-month growth rate is zero. Over six-months, sales are up at a 0.5% pace. Over 12-months, sales are up at a 0.7% pace. Sales are decelerating on this timeline albeit at a very slow pace of erosion. And real retail sales (ex-autos) also are on a decelerating path with the recent three-month growth rate showing a decline.

Car registrations are falling in each of the last three-months and are decelerating sharply on that 12-month to six-month to three-month timeline.

In the quarter-to-date, German retail sales ex-autos, the same series in real terms and car registration all are contracting. Registrations are contracting at a very rapid pace.

The Brexit shock is not exactly catching German spending at its strongest point in this cycle, but the German economy is doing better than retail sales suggest. For one the GfK look-ahead reading on consumer climate for July already is estimated to have risen. That index is up to its highest reading since August 2015 and is in the top 1% of all its historic series readings (which extends back to 2002). That certainly is more impressive-looking than the retail sales result. Moreover, a new reading on German unemployment was just released today; the rate remains at a low point since German reunification. The number unemployed continues to drop. That is another set of signals pointing to overall German economic strength as well as to positive momentum, unlike retail sales.

The German consumer has been relatively more active in this expansion period than usual, but consumption is not the source of strength for the German economy. Moreover, spending trends recently have been fading. German economic strength simply does not help the rest of Europe very much because the economy is not generally focused on consumption. And for now, the German economy is much stronger than consumer spending would make it seem.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief