Global| Mar 31 2014

Global| Mar 31 2014German Retail Sales Post Strong Growth

Summary

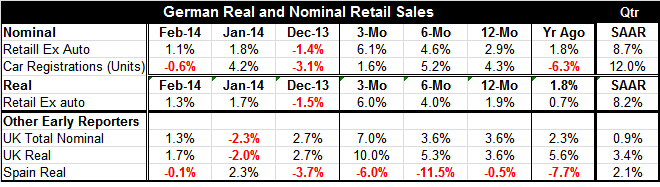

German retail sales are engaged in an unexpected pick up. Sales are up strongly for the two consecutive months. Sequential growth rates show clear acceleration in the retail sales spending patterns culminating in a 6.1% growth rate [...]

German retail sales are engaged in an unexpected pick up. Sales are up strongly for the two consecutive months.

German retail sales are engaged in an unexpected pick up. Sales are up strongly for the two consecutive months.

Sequential growth rates show clear acceleration in the retail sales spending patterns culminating in a 6.1% growth rate over three-months; also a gain of 6.1% annualized over three-months.

One thing that makes this picture just a little less believable is the lagging nature of auto registrations. While retail sales excluding autos are accelerating strongly, auto registrations have been up and down over the past months and longer.

In February, German auto registrations have fallen by 0.6%. Over three months, registrations are down to a 1.6% rate of growth. The previous strength in auto registrations has lapsed. However, in the quarter to date period (two months into Q1) both retail sales excluding autos and auto registrations are up strongly.

EU and EMU members the UK and Spain have issued early reports on retail sales as well. Spain's retail sales are still in a relatively steady state of contraction over the past year. Spain's real sales fell in February after a spike in January. However, because of that strength in January, Spain's quarter-to-date sales are actually rising at a respectable 2.1% annualized pace.

The UK shows real and nominal sales with their ups and downs over the past three-months. But viewed over the broader span of 3-month, 6-month and 12-month, UK sales are showing not only steady growth but acceleration in the pace of retail sales. Despite all that strength in the pipeline, UK annualized sales in the quarter-to-date are somewhat tepid. Real sales are up at a solid 3.4% pace in the quarter-to-date, but nominal sales are up at a pace just under 1%.

The picture emerging from these early EU sales reports is that of some firming in retail sales. Getting domestic demand moving up in the euro area is an important step in getting growth to be sustainable. These early results for February and for the unfolding first quarter are encouraging. Also getting a pick-up in German retail sales is a real plus since it is the most solid economy in Europe and is positioned to play more of a role of locomotive although that has not been the usual contribution of the German economy to Europe. If German retail strength was going to hold up, that would be a good development for growth prospects in the euro area.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.