Global| Feb 03 2009

Global| Feb 03 2009German Retail Sales Head South For The Winter

Summary

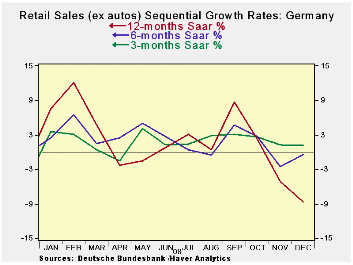

German nominal and real ex-auto retail sales are off for the third month in a row. In the fourth quarter nominal retail sales are off at a 4% pace; ex-auto real retail sales are dropping at a 2.1% pace. The sequential growth rates [...]

German nominal and real ex-auto retail sales are off for the

third month in a row. In the fourth quarter nominal retail sales are

off at a 4% pace; ex-auto real retail sales are dropping at a 2.1%

pace. The sequential growth rates show an accelerating pattern of

losses from 12-months to 6-months to 3-months, across the main

categories in the table.

The downturn has spreading across other measures as well, as

manufacturing has been notoriously weak. German consumers have not been

much of a prop to this economy for a long time. In the quarter ended

Sept 2008 they did rise by 1.9% Q/Q (saar), but that was after falling

by 3.2% (saar) in the previous quarter. Yr/Yr quarterly average real

(ex auto) retail sales have been negative in German since the quarter

ended December 2006. Ironically the 2008-Q4 retail sales figures on

this same basis are up by 0.1%, the first quarterly increase since

Q4-2008 and it comes as sales have turned tail to move sharply lower in

the quarter.

The German retailing association HDE is looking for retail

sales to decline in real terms in 2009. Manufacturing is coming apart

at the seams. Construction is weak, The German economy, Europe’s

largest, is under fire.

| German Real and Nominal Retail Sales | QTR | |||||||

|---|---|---|---|---|---|---|---|---|

| Nominal | Dec-08 | Nov-08 | Oct-08 | 3-MO | 6-MO | 12-MO | YrAgo | Saar |

| Retaill Ex auto | -0.6% | -0.8% | -0.9% | -8.7% | -0.4% | 1.2% | -4.6% | -4.0% |

| Food Bev & Tobacco | -1.5% | -1.6% | 0.0% | -11.6% | -1.1% | 1.2% | -3.2% | -2.6% |

| Clothing footwear | -0.9% | 1.1% | -4.4% | -15.9% | 4.3% | 1.1% | -2.7% | -5. |

| Real | ||||||||

| Retail Ex auto | -0.2% | -0.1% | -0.9% | -4.6% | 0.6% | 0.2% | -6.5% | -2.1% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief