Global| Jun 30 2014

Global| Jun 30 2014German Retail Sales Contract Again as All Growth Rates Turn Lower

Summary

German retail trends are turning lower as three-month, six-month and twelve-month growth rates are all sub-zero. Moreover, sequentially the sales drop is getting progressively larger. Even car registrations are showing a sharp [...]

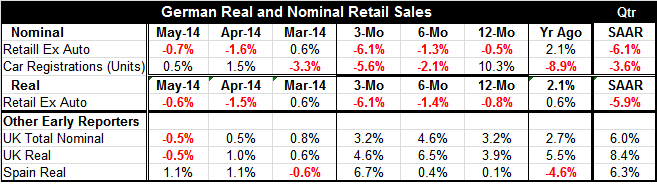

German retail trends are turning lower as three-month, six-month and twelve-month growth rates are all sub-zero. Moreover, sequentially the sales drop is getting progressively larger. Even car registrations are showing a sharp deceleration. The Ifo and ZEW surveys have been slipping, but the GfK survey dedicated to assessing consumer confidence continues to push higher. Yet, German consumers are pulling back. In the quarter-to-date (two of three quarters data are in) retail sales are falling at an impressively weak -6.1% annual rate (-5.9% in real terms). That's a big chunk of Germany GDP gone negative.

German retail trends are turning lower as three-month, six-month and twelve-month growth rates are all sub-zero. Moreover, sequentially the sales drop is getting progressively larger. Even car registrations are showing a sharp deceleration. The Ifo and ZEW surveys have been slipping, but the GfK survey dedicated to assessing consumer confidence continues to push higher. Yet, German consumers are pulling back. In the quarter-to-date (two of three quarters data are in) retail sales are falling at an impressively weak -6.1% annual rate (-5.9% in real terms). That's a big chunk of Germany GDP gone negative.

Real retail sales are steady or accelerating in the other early European reporters of retail trends. In the UK and Spain, real sales are growing at a pace of 8.4% and 6.3%, respectively in the unfolding quarter.

In other new data also released today, the EMU preliminary HICP shows EMU-wide inflation still at 0.5% year-over-year, keeping the European Central Bank still quite away from hitting its target. The ECB's new credit stimulus policies are too new to have had any impact on these reports just yet. But the incoming data make it clear that some action was necessary. In Italy, for example, year-over-year inflation is still decelerating, evidence that economic weakness is still taking its toll.

The sudden weakness in Germany's retail sales at a time that geopolitical instability is knocking on the door in Eastern Europe is not something to take lightly. While we see that the UK and Spain still seem to have good sales trends in place, the sharp drop in German retail sales is disturbing. It comes as there has been some softening in German industrial surveys such as the Ifo and ZEW. There is ongoing weakness in euro area wide inflation serving as another warning of underperforming growth.

Still, the Bank for International Settlements (BIS) today urged central banks to normalized interest rates, warning of dire consequences if interest rates are left too low for too long. The BIS is warning that monetary policy has lost its punch and that financial markets have soared while growth has languished. This, it argues, could breed unwanted consequences.

The slippage of German retail sales and emergence of weakness in the strongest economy in the euro zone is certainly an eye-opener, making us wonder if there is any policy response to it that it is needed or that could be effective. Despite the weakness in German industrial survey, German unemployment is still steady at 6.8%. Germany's retail weakness is a conundrum. We do not have consistent data for the German economy or for Europe. But the unevenness itself is a warning.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief