Global| Jan 31 2008

Global| Jan 31 2008German Retail Sales Continue to Slow

Summary

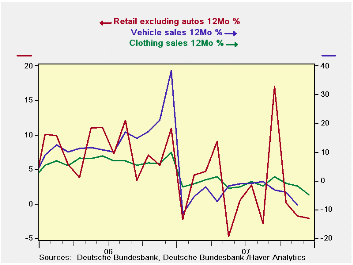

German retail sales in December did nothing to make large piles of presents appear under the old tanenbaum. Retail sales ex autos, German clothing sales and vehicle sales (that lag for now) each shows a dwindling trend. In the fourth [...]

German retail sales in December did nothing to make large piles of presents appear under the old tanenbaum. Retail sales ex autos, German clothing sales and vehicle sales (that lag for now) each shows a dwindling trend. In the fourth quarter, nominal ex auto sales are lower at a 7.4% annual rate; in real terms that becomes a -11.4% annual rate.

The German unemployment rate continues to drop but German unemployment still hovers above 8%. Despite ongoing e-Zone improvements the consumer remains a lagging sector and now creeping evidence shows a slowing across the e-Zone itself. Consumer confidence and retailing continue to be the lagging sectors that optimists look to become sources of growth as the Germany economy shifts into its next gear. The problem is that various consumer measures suggest that no such pick-up lies ahead for the consumer sentiment or for consumer spending. Strength in the euro, while a source of contentment to the ECB - and many Germans as well - is also a source of angst for what it means to German export prospects.

With the release of the EU Commission indexes today the German economy showed a drop to -1 in sentiment for the consumer sector in January. Retailing, too, saw sentiment fall back from a -18 rating in December to -22 in January. Germany’s industrial sector, the back bone of the economy, stepped back to post a +1 reading from +2 in December. The services and construction sectors (the latter still very weak) each posted month-to-month improvements. But by and large German sectors took a step back in January with Germany’s overall sentiment reading falling by two full points. The consumer sector does not seem about to get out of its rough patch at all.

| German Real and Nominal Retail Sales | ||||||||

|---|---|---|---|---|---|---|---|---|

| Nominal | Dec-07 | Nov-07 | Oct-07 | 3-Mo | 6-Mo | 12-Mo | Year Ago | SAAR (QTR) |

| Retail Ex Auto | -0.4% | -1.1% | -1.4% | -11.0% | -4.0% | -4.9% | 9.8% | -7.4% |

| Motor Vehicle and Parts | -- | -1.2% | 0.4% | -- | -- | -- | 38.2% | -- |

| Food Beverages & Tobacco | -1.4% | -2.3% | 0.1% | -13.5% | -5.3% | -3.3% | 5.7% | -4.5% |

| Clothing Footwear | 2.3% | -1.5% | -8.5% | -27.8% | -3.7% | -2.1% | 10.9% | -18.8% |

| Real | ||||||||

| Retail Ex Auto | -0.1% | -1.9% | -1.8% | -14.3% | -6.9% | -6.8% | 9.4% | -11.4% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief