Global| Sep 30 2020

Global| Sep 30 2020German Retail Sales Continue to Revive

Summary

While the virus is loose again in Europe, German retail sales logged a solid monthly gain rising by a strong 3.4% in August and propelling sales well above their pre-pandemic levels. Retail sales ex-autos are up by 6.6% from their [...]

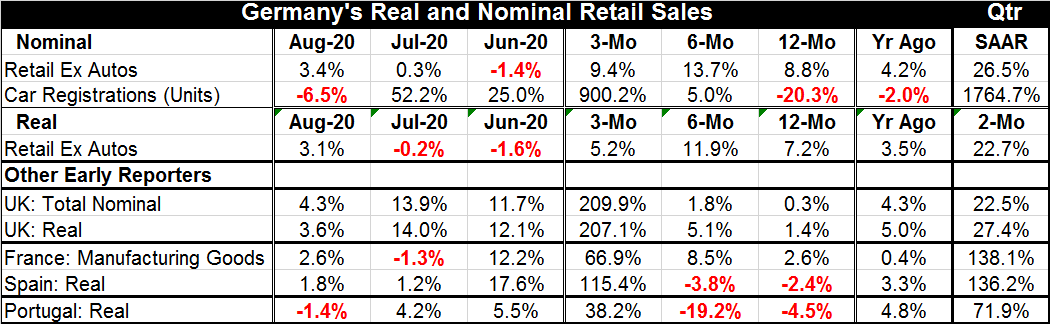

While the virus is loose again in Europe, German retail sales logged a solid monthly gain rising by a strong 3.4% in August and propelling sales well above their pre-pandemic levels. Retail sales ex-autos are up by 6.6% from their February mark, a 13.7% annualized rate. However, the last three-month gains have not been as strong with sales rising over three months at a still strong 9.4% but clearly slower annualized rate.

While the virus is loose again in Europe, German retail sales logged a solid monthly gain rising by a strong 3.4% in August and propelling sales well above their pre-pandemic levels. Retail sales ex-autos are up by 6.6% from their February mark, a 13.7% annualized rate. However, the last three-month gains have not been as strong with sales rising over three months at a still strong 9.4% but clearly slower annualized rate.

However, car registrations in Germany are less than tops. Registrations just fell by 6.5% in August, a sharp drop but not so sharp when contrasted to the 52.2% gain the previous month. Car registrations are volatile. But this is one important category of spending that is not so fully revered. The graphic show this fairly clearly. In terms of numbers, registrations are up by 2.5% from their February level (5% annualized rate). But they are net lower over 12 months and lower than their average for all of 2019. Car registrations are struggling in Germany, but other retail sales are not.

In the quarter-to-date (two months into Q3), both non-auto sales and car registrations are stirring (car registrations have an astronomical growth rate (1764.7%!). Real and nominal non-auto sales are growing in the 20-25% range (annualized).

Other early retail sales reporters are the United Kingdom, France, Spain and Portugal.

The message there is largely – but not wholly- the same. All those countries except Portugal have sales gains in August. The U.K. and Spain have gains in each of the last three months while Portugal and France have gains in two of the last three months – of course all of them had sharp gains four months ago in May as they all came out from whatever sort of lockdown they had been under.

The U.K. and France join Germany with solid gains in sales over six months; right now that calculation spans the covid-19 infection period as February was generally the high point for sales before the covid-19 crisis hit Europe. The U.K. has real sales rising at a 5% rate from that pre-covid-19 period while France has the sale of manufactured goods up at an 8.5% annualized rate. Spain and Portugal, however, lag on this recovery. Both have sales lower on balance since February. Their retail sectors have not recovered fully from the covid-19 lockdown. For Spain it's a drop in real sales at a 3.8% pace; for Portugal it's a much deeper drop at a 19.2% annualized pace. Spain's retail sales continue to advance, however, while Portugal's sales have just backtracked in August.

All of these countries are facing a new challenge from a spreading virus. It is either a relapse or a second wave. No one seems quite sure what to call it besides something that is bad and undesirable.

As I have been saying for some time, the virus is going to call the tune for economic growth. Most countries look to shift policies to reduce the pace of infection when it picks up and that usually means some sort of lockdown or economic interruption even if only on a localized level. Even though the ability to deal with the virus and to help those who are infected has improved and even though hospitalizations are less frequent and generally less serious, the policy is still virus avoidance – for everyone. One view is that the virus came through in phase one and took the lives of the most vulnerable and now it faces a less damaged and heartier population making it less of a risk to those who have survived thus far. The data on the virus are extremely clear. The virus preys on the weak and the sick and especially when the weak and sick are also old. Very few people without preexisting conditions die from this virus. And yet policy makers continue to treat it like it is a much more volatile and dangerous animal.

A better plan that might allow growth and the virus to coexist until a workable vaccine is found (if one is found). Such a plan needs to be formulated. Protecting those with compromised immune systems would be a big part of that. But running and hiding every time there is an outbreak is creating all kinds of economic stress as well as stress in other ways and as well as disrupting the education of children who have been shown to be nearly impervious to the disease unless they have one of the preexisting conditions that makes them vulnerable.

Governments continue to treat this virus as they have from the start rather than to craft new policies that build on what we know and what we have learned. Some health officials need to see good news in triplicate on unimpeachable academic frameworks before they are ready to endorse it and use it. We need to do better than that. Health officials need to realize that promising techniques used by frontline workers may be able to save lives even if those techniques have not been vetted in the most rigorous of tests. Waiting for undeniable proof costs lives too. Every decision has an upside and a downside.

Stopping the virus spread is not without costs and those costs are mounting while the virus shows signs of being less lethal not more lethal when properly dealt with. But it is getting late in the game and I get the sense that globally health officials have become ossified in their stance. Maybe part of this is that they do not what to make changes in public policy and risk being criticized for how they have handled things so far. Let's hope that is not driving policy. And at this point, let's hope that some of these vaccines work and are approved quickly.

Commentaries are the opinions of the author and do not reflect the views of Haver Analytics.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief