Global| Sep 09 2009

Global| Sep 09 2009German Prices Fall Yr/Yr Again-ButIt's NOT Deflation

Summary

German consumer prices fall Yr/Yr! - The headlines may read that German inflation on the HICP measure is down again Yr/Yr but don’t bite on that headline or on the nuance that it might be deflation time in Europe. Nothing is farther [...]

German consumer prices fall Yr/Yr! - The headlines may read

that German inflation on the HICP measure is down again Yr/Yr but don’t

bite on that headline or on the nuance that it might be deflation time

in Europe. Nothing is farther form the truth. First of all, Germany’s

headline inflation rose by 0.7% from July even as it fell from August

of one year ago. Next, the German domestic inflation gauge rose by 0.5%

in the month and is up by a narrow 0.1% Yr/Yr, failing to confirm any

downtrend. Moreover, German domestic core (ex food and energy)

inflation rose by 0.2% and is up by 1.1% Yr/Yr. Inflation in Germany is

tame the core pace is steady, and deflation is nowhere in sight.

The cards are stacked against deflation - For those who might

harbor deflation dreams let’s note that we are looking at data from

August. In September the German HICP index will rise by 0.1 index

points in 2008. So any rise less than 0.1 index points (less than 0.1%)

in Sept 2009, will take the headline German HICP lower again. But then

from September 2008 to August of 2009 every single month’s headline

price index (the index LEVEL) is below that of September 2008. If

German deflation is going to set in, that will have to happen on the

strength of current prices falling month-by-month in the future not

just rising more slowly than they did one year ago.

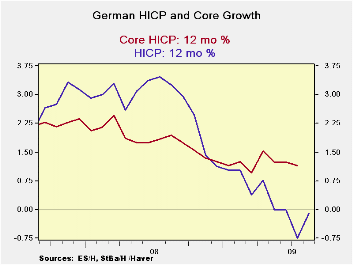

There is no real deflation trend - Headline HICP inflation is

up in eight of the last nine months in terms of its month-to-month

changes. There is no real evidence that deflation has taken any hold in

Germany. Indeed, the chart on German Yr/Yr headline and core HICP

inflation shows that the headline rate, while still negative, has

upward momentum building.

Growth is taking root - With German industrial orders up

strongly and orders in Europe expanding and revivals in consumer

sentiment being experienced, it seems that Europe and Germany are on

their way back to better times. While the economies on the continent

may continue to fall short of being in full employment, there is no

evidence to suggest that prices have much downside risk.

| German HICP | |||||||

|---|---|---|---|---|---|---|---|

| Mo/Mo % | Saar % | Yr/Yr | |||||

| Aug-09 | Jul-09 | Jun-09 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| HICP Total | 0.7% | -0.5% | 0.5% | 2.6% | 0.6% | -0.1% | 3.3% |

| Core | #N/A | 0.1% | 0.2% | #N/A | #N/A | #N/A | 1.9% |

| CPI | |||||||

| All | 0.5% | -0.4% | 0.4% | 1.9% | 0.6% | 0.1% | 3.1% |

| CPIxF&E | 0.2% | 0.3% | 0.0% | 1.9% | 1.3% | 1.1% | 1.8% |

| Food | -0.4% | -0.4% | 0.5% | -1.1% | -3.0% | -2.7% | 7.0% |

| Alcohol | 0.4% | -0.8% | 0.5% | 0.0% | -0.7% | -1.5% | 4.2% |

| Clothing & Shoes | 1.9% | -1.5% | -0.3% | 0.4% | -0.4% | 1.5% | 1.5% |

| Rent &Util | 0.3% | -0.4% | 0.2% | 0.4% | -0.7% | -0.2% | 3.9% |

| Health Care | 0.0% | 0.1% | -0.1% | 0.0% | 1.6% | 0.7% | 1.9% |

| Transport | 2.4% | -1.1% | 0.8% | 8.9% | 3.6% | -2.0% | 4.8% |

| Communication | 0.0% | 0.0% | 0.1% | 0.4% | -0.9% | -1.6% | -3.6% |

| Rec &Culture | 0.5% | 0.5% | -0.1% | 3.6% | 2.4% | 2.1% | 0.4% |

| Education | -0.5% | 0.8% | -0.2% | 0.6% | -8.2% | -5.1% | 3.4% |

| Restaurant & Hotel | -0.1% | 0.2% | -0.2% | -0.4% | 0.4% | 1.7% | 2.4% |

| Other | 0.4% | 0.3% | 0.1% | 3.0% | 2.6% | 1.8% | 1.8% |

| Diffusion | -- | -- | -- | 81.8% | 54.5% | 18.2% | -- |

| Type: | Diffusion: Current Compared to | 6-mo | 12-mo | Yr-Ago | -- | ||

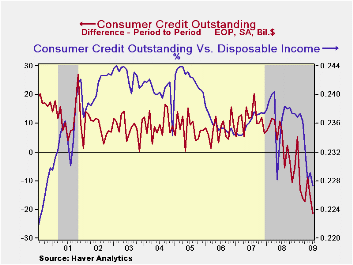

Consumer Credit Outstanding Falls For An Unprecedented Sixth Straight Month

by Tom Moeller September 09, 2009

The

deteriorating job market and uncertain prospects for improvement, plus

over-leverage from past spending, has prompted an end to the growth in

consumer credit. The Federal Reserve reported late-yesterday that

consumer credit outstanding fell during July for the sixth straight

month and for the tenth month since last summer. Perhaps more

impressive, however, is the magnitude of the cutbacks. The $21.5B July

decline was the record for any one month and double-digit monthly

declines have prevailed all this year.

The

deteriorating job market and uncertain prospects for improvement, plus

over-leverage from past spending, has prompted an end to the growth in

consumer credit. The Federal Reserve reported late-yesterday that

consumer credit outstanding fell during July for the sixth straight

month and for the tenth month since last summer. Perhaps more

impressive, however, is the magnitude of the cutbacks. The $21.5B July

decline was the record for any one month and double-digit monthly

declines have prevailed all this year.  On a percentage basis the 4.2%

y/y decline is a record.

On a percentage basis the 4.2%

y/y decline is a record.

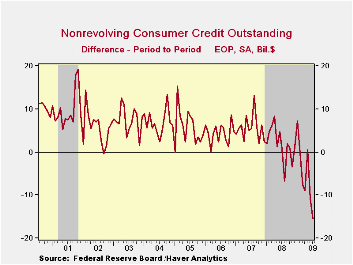

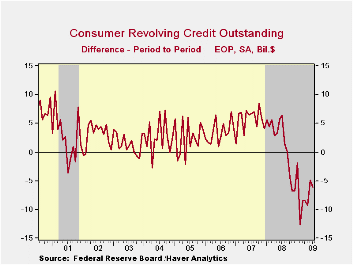

Usage of non-revolving credit (autos & other consumer durables), which accounts for nearly two-thirds of the total, fell a record $15.4B after a $10.7B June drop. Except for the mid-1970s, these declines were enough to pull the retrenchment to near the record for a two-month period in dollar terms as well as on a percentage basis. The 2.6% y/y decline is near the record. Additionally weighing on overall credit has been the tight rein on revolving credit usage. During July, revolving credit outstanding fell $6.1B for the tenth consecutive monthly drop. In percentage terms the decline pulled the outstanding total down a record 7.1%.

Despite

these huge declines, there arguably is more to come. Consumers have

been successful in reducing credit outstanding as a percentage of

disposable income to 22.7% from its 2005 high of 24.4%.  However, these

levels compare to the lows near 16% in the early-1990s. Now that the

"shop-till-you-drop" mantra has been diffused by the aging population

of the U.S., a return to some lower level of credit usage is likely.

However, these

levels compare to the lows near 16% in the early-1990s. Now that the

"shop-till-you-drop" mantra has been diffused by the aging population

of the U.S., a return to some lower level of credit usage is likely.

These figures are the major input to the Fed's quarterly Flow of Funds accounts for the household sector.

Credit data are available in

Haver's USECON database. The Flow of

Funds data are in Haver's FFUNDS database.

The latest Beige Book from the U.S. Federal Reserve Board can be found here.

The Credit Crisis and Cycle-Proof Regulation from the Federal Reserve Bank of St. Louis is available here.

| Consumer Credit Outstanding (m/m Chg, SAAR) | July | June | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Total | $-21.5B | $-15.6B | -4.2% | 1.6% | 5.6% | 4.1% |

| Revolving | $-6.1B | $-4.9B | -7.0% | 1.9% | 7.8% | 5.0% |

| Non-revolving | $-15.4B | $-10.7B | -2.6% | 1.4% | 4.4% | 3.6% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief