Global| Sep 21 2015

Global| Sep 21 2015German PPI Trends Begin to Turn Lower Again

Summary

The chart displays the three key frequencies of growth I regularly calculate for the German PPI. It plots them and clearly reveals the last four cycles in German PPI pressure. The three-month percentage change leads the parade of [...]

The chart displays the three key frequencies of growth I regularly calculate for the German PPI. It plots them and clearly reveals the last four cycles in German PPI pressure. The three-month percentage change leads the parade of changes. After seeing three-month changes rise for few months, the series has peaked and is tuning lower again; another down-cycle is in gear. Here we are looking at a chart of the more stable ex-energy PPI, not the more fickle headline inflation series.

The chart displays the three key frequencies of growth I regularly calculate for the German PPI. It plots them and clearly reveals the last four cycles in German PPI pressure. The three-month percentage change leads the parade of changes. After seeing three-month changes rise for few months, the series has peaked and is tuning lower again; another down-cycle is in gear. Here we are looking at a chart of the more stable ex-energy PPI, not the more fickle headline inflation series.

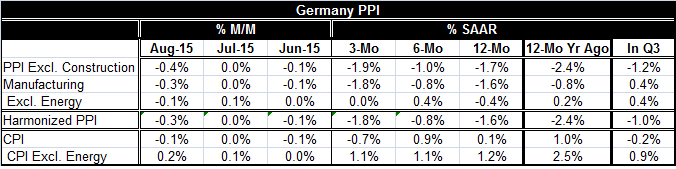

The table shows the growth rates for the PPI headline, manufacturing, manufacturing ex-energy and for two CPI measures. Sequential growth rates do not yet paint a perfectly clear picture of trends, but it is clear enough. For the most part, prices are down sharply in the PPI series over 12 months. Then the inflation picture shows less weakness over six months. Then over three months, the weakness is stepped up again and with a rate of change that is usually weaker than it was over 12 months. The PPI shows a clear onset of falling prices again, but not at a steady pace.

The CPI data show similar trends on different levels. CPI prices are less volatile and up over 12 months. The headline series rises faster over six months while the core series gets slightly weaker. Over three months, the headline CPI goes sharply negative while the core series stays at its slightly lowered six-month pace.

Mario Draghi has warned that the EMU could see falling prices again this year and the EMU again is on the cusp of just that. PPI prices, of course, are already there, showing clear declines on most horizons. The CPI series shows a declining headline in August and a year-over-gain in the CPI of just 0.1%, not far from showing declines again.

Oil prices have been falling and are the most visible deflation catalysts again. But there is also global weakness. Taiwan, an important global exporter, has reported today that its export orders have fallen for the fifth consecutive month. Price weakness is not simply about excesses in the oil patch although oil is a key weak price. On global markets, today oil firmed as we are finally starting to get some evidence of weaker drilling activity in the U.S. caused by low oil prices.

It's a hard global economy to keep you finger on its pulse. There are many irregular heartbeats. This weekend one loose end was tied up as in Greece Tsipras won a much easier election victory than expected. Greece seems to have avoided being a sour surprise for now. But the migrant issue still haunts Europe. Spain has elections coming in three months and it has its own internal dissent. The China beige book shows a still weakened economy and points to a much changed economy there. There is little in the global economy to be complacent about.

The Fed last week did choose to hold rates steady, but it made few promises for the future. Markets seem less sure of the Fed than at any time in recent memory. The migrant crisis weakens Europe and has it divided over how to deal with the problem. Meanwhile, key geopolitical hot spots remain hot. Inflation is moving lower and the best bet is that it will continue to do that for some time. It is not just some weakness riding on the back of fickle oil prices. There are global forces of weakness and deflation back in play.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief