Global| Jan 20 2017

Global| Jan 20 2017German PPI Takes Wing...Even Excluding Energy

Summary

As the ECB met this past week, policy was kept on an even keel despite pressures from rising oil prices. ECB President Mario Draghi has said that he is unconvinced that there is an underlying trend to inflation. Draghi sees energy, a [...]

As the ECB met this past week, policy was kept on an even keel despite pressures from rising oil prices. ECB President Mario Draghi has said that he is unconvinced that there is an underlying trend to inflation. Draghi sees energy, a transient factor as driving inflation higher. ECB policy is not inclined right now to react to transient factors.

As the ECB met this past week, policy was kept on an even keel despite pressures from rising oil prices. ECB President Mario Draghi has said that he is unconvinced that there is an underlying trend to inflation. Draghi sees energy, a transient factor as driving inflation higher. ECB policy is not inclined right now to react to transient factors.

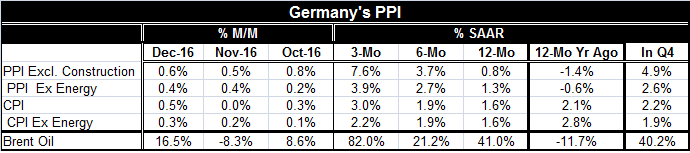

However, for Germany, PPI inflation excluding energy is pushing relentlessly higher. The German CPI is accelerating to a 12-month pace of 1.6% and rising at an annualized pace of 3% over three months. The German CPI excluding energy is up by 1.6% over 12 months and rising at a 2.2% annualized rate over three months. In Germany, there seems to be a good flush of inflation excluding energy unless this is just an energy pass through rippling through the German price indices at an accelerated pace.

Of course, Germany is not the whole of the EMU. But Germany has a heavy weight in overall EMU data and the German inflation experience is going to be reflected, even if watered down, in the EMU-wide results. And EMU-wide there are going to be energy price pressures since everyone pays (more or less) the same amount for energy by source.

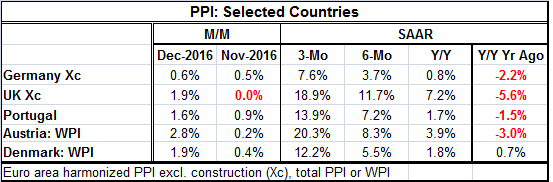

In that regard, there are four other European nations (two other original EMU members) that have reported their PPI data as early as Germany. Early reports from other nations often do not provide 'core' inflation or even excluding-energy measures. The overall PPI or WPI results tell a pretty clear story. With energy embedded in the overall index, inflation in each of these early reporters is surging. In fact, the German PPI rise is weakest at a three-month annualized pace of 7.6%. Everywhere else the annualized three-month pace is well into double digits. Everywhere inflation is accelerating: year-over-year compared to the rate of 12 months earlier; over six months compared to 12 months; and, over three months compared to over six months. These progressions are represented in each of the early reporters.

The acceleration in the annualized headline PPI rate, comparing the 12-month pace to the six-month pace, ranges from a low of 2.9% to a high acceleration of 5.4% in Portugal. I am measuring acceleration as the difference between the six-month and 12-month annualized growth rates in the respective PPIs here. For the time horizon of three-month vs. six-month, the fastest acceleration is in Austria with an acceleration of 12 percentage points compared to Germany at 4 percentage points. For each of these nations, the six-month pace exceeds the 12-month pace. And the acceleration gets progressively faster over shorter time spans. The inflation effect on the headline PPI or WPI is intensifying.

The behavior of the PPI is quite horrifying on its own. But the PPI is far more susceptible to distortions from energy inflation than is the CPI. Still, we can see that for Germany at least the CPI excluding energy also is accelerating. But the statistical relationship between the CPI and PPI is not tight and that helps to break the chain of worry. For Germany, the one-year PPI to CPI correlation is only 0.22. That makes the R-squared relationship only 0.05. The PPI explains only a very tiny among of the variation in the CPI. The PPI is much more volatile than the German CPI as well with a standard deviation of one-year inflation at 1.8 percentage points. By comparison, the CPIs standard deviation over the same period is 0.4 percentage points - more than four times less volatile.

The German economy clearly is running hotter than the EMU economy overall. Draghi senses that. But a number of EMU members and non-EMU members are having substantial price pressures of their own. The German unemployment rate is on its all-time (post reunification) low. But the unemployment rate for all of the EMU is still several percentage points above its low and the same gap calculated country by country for original EMU members shows considerably more slack than that. It makes sense that Germany should have more home-grown inflation than other EMU members. But with the German's being hyper-sensitive to the inflation rate and with the ongoing gains in energy prices, ECB forbearance would seem to be on a short leash. The ECB is a single mandate central bank and will have a hard time maintaining stimulative policies regardless of EMU-wide rates of unemployment and GDP growth as oil prices continue to pulse through to CPI and HICP prices. Draghi can turn a 'blind eye' to what are coming to be pretty impressive uptrends for inflation for only so long. If OPEC hangs together, it's a fair bet that EMU stimulus will not endure.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief