Global| Sep 20 2016

Global| Sep 20 2016German PPI Shows Less Downward Pressure...And So?

Summary

The German PPI was flat in August. The PPI excluding energy was also flat. The CPI was flat in August. The CPI excluding energy was up by 0.1%. Is there a pattern here? Flat, flat, flat, and up by 0.1%. These are very moderate [...]

The German PPI was flat in August. The PPI excluding energy was also flat. The CPI was flat in August. The CPI excluding energy was up by 0.1%.

The German PPI was flat in August. The PPI excluding energy was also flat. The CPI was flat in August. The CPI excluding energy was up by 0.1%.

Is there a pattern here? Flat, flat, flat, and up by 0.1%. These are very moderate results. Yet, because prices have been falling; these are results that show `inflation acceleration'. Look out? NOT! Inflation may be in some technical sense rising. But trends are still broadly flat and look to be on their way to remain broadly low.

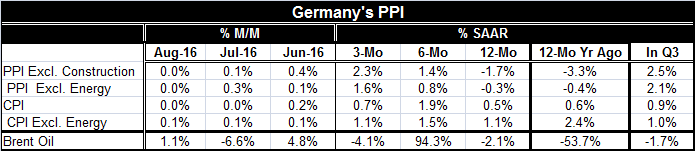

PPI prices rose both in June and in July. The table offers new PPI observations plus the most recent German CPI trends. They show that PPI inflation is accelerated steadily when expressed at annualized rates as they are in the table. But the CPI shows less of that. The headline and ex-energy CPI show no steady accelerating. The CPI headline is barely stronger over three-months than it is year-on-year (0.7% vs. 0.5%) while the CPI ex-energy has the same pace over three-months as over 12-months (1.1%).

Two months into the new quarter (Q3), the PPI headline is up at a 2.5% pace and by 2.1% excluding energy. This compares with a 0.9% gain for the CPI and a 1.0% pace for CPI ex-energy.

The impact of oil prices is both tranquil and insidious. Oil (Brent) is off by only 2.1% over 12-months and is lower at only a 4.1% annual rate over three-months. But in between, oil shows a 94.3% annual rate rise over six-months. Obviously, there is plenty of room for oil to be injecting some real pressure into prices given its move over six-months, but equally as obvious is the fact that more broadly oil prices have settled down near term as well as over the past 12-months. This lump of pressure will gradually pass through the PPI and become less of a factor - if oil continues to move sideways as it has.

The chart shows how much more volatile PPI prices are in Germany than the CPI, which is more the price index that the Bundesbank and ECB officials will care about. Since 2006, the PPI has swung widely from a gain as large as 4.8% to a drop of 3.3% year-on year excluding energy while the CPI on that basis has swung from 0.6% to 2.6% - a much narrower band. The year-over-year correlation between the two ex-energy measures on one-year percentage changes is only 0.2 as the PPI posts a standard deviation on annual percentage changes of 1.8% and the CPI of 0.4%.

The ex-energy PPI tends to signal changes in direction for the ex-energy CPI, but it can take huge changes in the PPI to generate small changes in the CPI. The history of these two series tells us that there is little pressure on the horizon for the German CPI which is now up by just 0.5% over 12-months and up at a 0.7% annual rate over three-months.

While German PPI prices are not falling as fast as they once were, they are not really signaling any pick-up in inflation for any measure that officials really care about. Oil prices are also losing their volatility. But the jury is always out on oil. I really only feel comfortable talking about what oil has done -not what its price will do. And I have a long history with oil prices having been forecasting oil prices since 1977. The current period is still marked by excess in oil output, but there continues to be shocks in Libya and Nigeria and weather effects in the Gulf of Mexico that affect oil operations here and there. Despite an ongoing oil glut, producers have been able to keep the oil price more or less even keeling. Oil production in the U.S. is slowly recovering as producers can make profits at current price levels, adding to the excess of oil. Globally, growth has been disappointing holding back demand estimates. Iran is till bringing more oil on stream but doing it very slowly. Meanwhile, the Saudis and Russians desperately want to hike prices but also face political and economic as well as oil market constraints. The oil market continues to be rife with certain kinds of tensions. The future for oil, as always, hangs in the balance and with oil you never know. That's why they call them `oil shocks.' For now, the coast seems clear, oil prices seem stable and inflation globally is somewhere between well-behaved and too low. But those conditions can be disrupted.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief