Global| Oct 20 2008

Global| Oct 20 2008German PPI Pressure Still Lingers

Summary

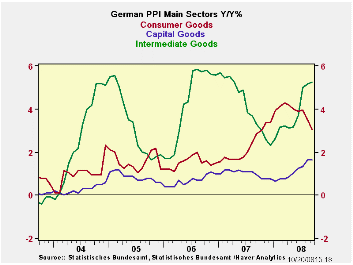

Consumer goods inflation has broken lower in Germany. But for capital goods and intermediate goods, inflation forces are lingering. Headline PPI inflation has spurted by 7.8% over three months, a far cry from the 2% limit on consumer [...]

Consumer goods inflation has broken lower in Germany. But for capital goods and intermediate goods, inflation forces are lingering. Headline PPI inflation has spurted by 7.8% over three months, a far cry from the 2% limit on consumer prices. The 0.4% headline PPI rise in prices in September offsets most of the 0.5% decline in August. For ex-energy prices the rise in September was a thin 0.1%. Over three months, however, the inflation rate is a still troubling 4.3% and the sequential growth rates show a ramping up of ex-energy inflation for 12 months to 6 months to 3 months.

Still, Jurgen Stark, a former Bundesbank member and currently an executive of the ECB says that, "We are seeing that due to the weakening in growth and the probability of very flat growth in 2009, the inflation rate will also probably fall somewhat more strongly than we had earlier expected."

Policy makers are looking at inflation and its trends very

differently these days. They are setting performance and trends aside

because oil prices have dropped so suddenly and economic growth has

dimmed so quickly. Apparently, few policymakers give much credence to

the notion that the OPEC meeting this week could re-boost oil prices in

a way to light a new fire under inflation. Central banks have gotten,

instead, to the point of being so worried about (or sure of) coming

economic weakness and its impact on prices that they are losing their

fear of inflation near term. This is very significant especially for a

central bank like the ECB that only has an inflation mandate – no

growth mandate.

| Germany PPI | ||||||||

|---|---|---|---|---|---|---|---|---|

| %m/m | %-SAAR | |||||||

| Sep-08 | Aug-08 | Jul-08 | 3-mo | 6-mo | 12-mo | 12-moY-Ago | IN Q3 | |

| MFG | 0.4% | -0.5% | 2.0% | 7.8% | 10.1% | 8.3% | 1.5% | 11.7% |

| Ex Energy | 0.1% | 0.2% | 0.8% | 4.3% | 3.9% | 3.5% | 2.5% | 5.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief