Global| Feb 18 2005

Global| Feb 18 2005German PPI on Firm Uptrend; Could It Slow?

Summary

PPI data for Germany have shown a tendency toward stronger prices in recent months, The total PPI surged 0.8% in January, but this was mainly due to an abrupt upturn in energy, which swung from a 0.9% decline in December to a 2.8% [...]

PPI data for Germany have shown a tendency toward stronger prices in recent months, The total PPI surged 0.8% in January, but this was mainly due to an abrupt upturn in energy, which swung from a 0.9% decline in December to a 2.8% jump in January. Excluding energy, the PPI rose 0.3%, slower than the December increase of 0.5%. (This PPI is a comprehensive measure including finished products, semi-processed items and raw materials. The US "headline" figure called PPI, in comparison, covers only final goods.)

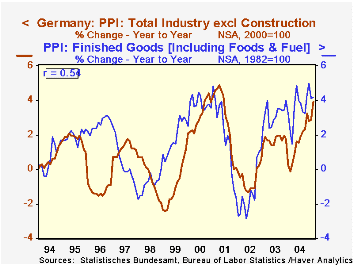

The year-on-year performance of the German PPI has been firm, and January continued that trend. The total index was up 3.9%, following a 2.9% yearly increase in December. These were the largest since the middle of 2001. Energy is clearly one component of this gain. Chemicals and plastics, which are petroleum related, have also risen more rapidly.

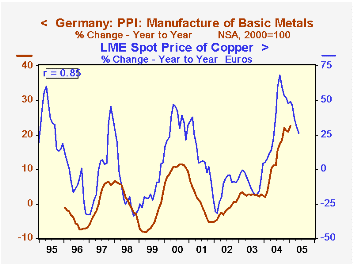

A third source of the increase in the German PPI is prices of metals and metal products. The dramatic increase in prices of basic metals is evident in the table and also in the second graph. Metals prices rose rapidly on world commodity markets last year. In the second graph, we show the closing spot price of copper on the London Metals Exchange; it is quoted there in US dollars and we converted that to euros. The correlation tool in Haver's DLX software indicates a substantial 85% correlation between that commodity price and the German PPI for basic metals. Further, the simple lead-lag feature of the software, implemented with the <CTRL> key and the right or left arrow, shows that the correlation is maximized at a 4-month lead for the commodity price. Thus, we can see in the chart that the pace of price increase in commodity markets has eased most recently, suggesting -- if this history is any guide -- the possibility for slowing during the next several months of the PPI for this very fundamental item in the production process.

| Germany: Producer Price Indexes (% chg) | Jan 2005 | Dec 2004 | Nov 2004 | Year/ Year | December/December|||

|---|---|---|---|---|---|---|---|

| 2004 | 2003 | 2002 | |||||

| PPI | 0.8 | 0.1 | -0.4 | 3.9 | 2.9 | 1.8 | 0.6 |

| ex Energy | 0.3 | 0.5 | 0.1 | 3.0 | 2.8 | 0.2 | 0.6 |

| Energy | 2.8 | -0.9 | -2.1 | 7.3 | 3.3 | 8.0 | 0.5 |

| Manufacturing | 0.3 | 0.1 | -0.4 | 3.4 | 3.2 | 0.2 | 1.1 |

| Basic Metals | 1.7 | 0.0 | 0.2 | 22.6 | 21.0 | 2.3 | 1.7 |

| Fabricated Metals | 1.1 | 0.1 | 0.2 | 5.9 | 4.8 | 0.2 | 0.7 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief