Global| Sep 20 2019

Global| Sep 20 2019German PPI Drops in Step with Oil

Summary

German PPI drops as Brent oil prices continue to descend The drop in the German PPI brings several thoughts to mind. One of them is that ongoing price declines are not good with inflation already undershooting and the European Central [...]

German PPI drops as Brent oil prices continue to descend

German PPI drops as Brent oil prices continue to descend

The drop in the German PPI brings several thoughts to mind. One of them is that ongoing price declines are not good with inflation already undershooting and the European Central Bank having just put a new stimulus deal in place- a deal that Mr. Draghi had to fight for and did so on his way out of office. Next, there is the tracking of German PPI prices with oil.

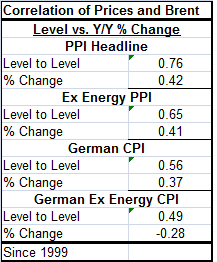

The small table below shows that looking at price level to level correlations for 12-month changes the link between inflation and oil is strongest for the PPI headline. Exclude oil from the PPI and the correlation to Brent drops from 0.76 to 0.65 and the correlation on the 12-month percentage change barely changes edging down to 0.41 from 0.42. However, the ECB looks at CPI prices and for Germany CPI ex energy price level correlation to Brent is 0.49 and the correlation of the CPI ex energy on a 1-month basis to Brent is -0.28.

The ECB is not as known as the Fed turn its gaze from the headline to the ex-energy price gauge or to the core gauge but certainly differential performance in the headline and core is something the ECB will be watching. As of June and July, ECB-wide PPI trends were showing broad based PPI drops across EMU members largely because of the drop in Brent.

The ECB is not as known as the Fed turn its gaze from the headline to the ex-energy price gauge or to the core gauge but certainly differential performance in the headline and core is something the ECB will be watching. As of June and July, ECB-wide PPI trends were showing broad based PPI drops across EMU members largely because of the drop in Brent.

But now there is a new trend in town. In the wake of the XXX? attack on Saudi Arabia, Brent prices have spiked and remain higher. Over the next few months, there will be some higher price pressures to send through the system as Brent will add to the inflation load. For now the Saudis are up beat on their ability to repair the damage on their facilities. But it is not yet clear how to handicap the future. It's about much more that the Saudi's ability to repair this damage.

The United States and Saudi Arabia blame Iran for what was a technologically advanced air strike few could have conduced; possibly using cruise missiles and drones. And if that is true, the future is quite murky. With that scenario, what might prompt the next strike? Will there be a next strike? If there is military retaliation by Saudi Arabia, Iran is already saying it is prepared for massive retaliation and war. What sort of damage could a follow up Saudi strike do? All sorts of questions linger about the future whether the attacks were by Iran or an Iran agent which seem to be the only real choices. The Saudis are convinced that this act can't be allowed to stand without a response, but Iran seems to have so much less to lose. Since oil does affect a broad array of prices, we should be wary although at the same time aware the core consumer prices will be much less affected. Still, a 'war' in the Gulf is one of the worst conceivable possibilities. Yet, can that worry empower Iran to do whatever it wants? Will Europe ever realize how much this behavior vindicates the U.S. position on Iran- Iran is wholly untrustable. It seems willing to destroy Saudi capabilities so that letting Iran pump and sell oil will be the only viable option!

Beyond oil there ae other difficult trends here...

What we see is that intermediate goods prices are falling obviously reflecting weak oil prices. Investment goods prices are holding their path, seemingly unaffected by oil. And consumer goods prices have stepped up their pace of increase. If we look at sector correlations to Brent, correlations show a 0.76 correlation between Brent and intermediate goods price levels and a 0.47 correlation to 12-month percent changes. Consumer prices have a price level correlation to Bent of 0.56 with a 12-month percent change correlation of 0.22. Capital goods or investment goods have a price level correlation to Brent of 0.42 with a 12-month percent change correlation that is negative at -0.29. These correlations speak to the influence oil prices have on German PPI sector prices and explain a lot about current pricing trends in the PPI except for consumer goods where the pace has turned higher despite a weak positive correlation to Brent price changes.

What we see is that intermediate goods prices are falling obviously reflecting weak oil prices. Investment goods prices are holding their path, seemingly unaffected by oil. And consumer goods prices have stepped up their pace of increase. If we look at sector correlations to Brent, correlations show a 0.76 correlation between Brent and intermediate goods price levels and a 0.47 correlation to 12-month percent changes. Consumer prices have a price level correlation to Bent of 0.56 with a 12-month percent change correlation of 0.22. Capital goods or investment goods have a price level correlation to Brent of 0.42 with a 12-month percent change correlation that is negative at -0.29. These correlations speak to the influence oil prices have on German PPI sector prices and explain a lot about current pricing trends in the PPI except for consumer goods where the pace has turned higher despite a weak positive correlation to Brent price changes.

Looking ahead, there is a lot of uncertainty. The ECB will have a new head who has promised to look at the effectiveness of negative interest rates. Christine Lagarde has been approved by the EU Parliament, but she will still have to 'win-over' the hard money German crowd in particular. Mario Draghi has left her with a legacy of extra stimulus which might give Lagarde some ability to give back to German demands without costing the EMU area much of its stimulus. But what lies ahead is certainly a different sort of period from what Europe has been though. Now that 'impossible has been done' and a lot of monetary stimulus is in place, inflation is still undershooting! Germany may be headed for recession too! But the Germans seem to care about that less than anyone else. Germany continues to pursue fiscal surplus in its domestic budget agenda. I guess that Keynes has been long dead on German soil. I think he was even banned in Germany under the Schengen despite already being dead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief