Global| Jan 20 2016

Global| Jan 20 2016German PPI Continues to Weaken

Summary

Germany's PPI gauge fell by 0.4% in December as it continued a string of weakness. Manufactures prices also fell, extending their string of declines. Ex-energy manufactures prices were flat in December after a series of drops. Oil [...]

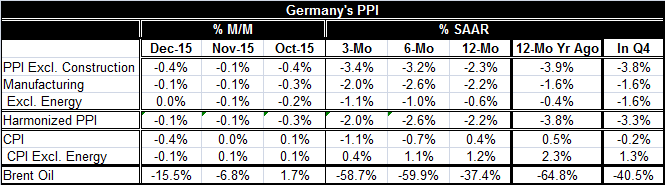

Germany's PPI gauge fell by 0.4% in December as it continued a string of weakness. Manufactures prices also fell, extending their string of declines. Ex-energy manufactures prices were flat in December after a series of drops. Oil prices, of course, have continued weak during this period and spot oil prices are still falling in early 2016 and creating severe disruptions in world markets and supply chains. The prospect for price declines to abate is still not good.

Germany's PPI gauge fell by 0.4% in December as it continued a string of weakness. Manufactures prices also fell, extending their string of declines. Ex-energy manufactures prices were flat in December after a series of drops. Oil prices, of course, have continued weak during this period and spot oil prices are still falling in early 2016 and creating severe disruptions in world markets and supply chains. The prospect for price declines to abate is still not good.

The sequential growth rates in the German PPI show progressively faster annual rates of declines from 12-months to six-months to three-months. Manufactures prices decline on all those horizons, but the pace of decline has let up over three-months compared to six-months and 12-months. Ex-energy prices, however, continue to show accelerated drops albeit at a slower pace than the headline. The German harmonized PPI is declining, but not quite as fast as the German domestic PPI gauge. Moreover, the HICP fails to show continually weaker sequential trends, as the drop in prices has let up in that index over three-months compared to six-months and 12-months.

Germany's more important CPI shows deceleration is in force for the headline as well as for the ex-energy gauge. While the ex-energy price index is up by 1.2% over 12-months, it is also up at just a 0.4% annualized rate over three-months. All price gauges show substantial ongoing declines in the fourth quarter. Oil in Q4 is falling at a 40% annualized rate.

ECB Governing Council member Ewald Nowotny today cited some progress in the ECB's asset purchase program but noted that the price target is hard to hit. Both Germany and the ECB economies display that same problem. Price weakness is a global problem with oil and other commodities being unhinged. No central bank that targets inflation is having much success in hitting its respective inflation target.

Central banks do take different approaches. The ECB has stepped up its market intervention. The Bank of Japan is continuing its program. The Bank of England has its various schemes on hold and declares no timetable for a rate hike but clearly is waiting for the time to be right to hike rates. The U.K. has just reported an all-time high employment rate so the U.K. economy is making progress.

But the Federal Reserve in the U.S. has to be the stalking horse. The Fed bit the bullet late in the year hiking rates ahead of everyone else despite lacking the conditions it had said would be necessary to begin its rate hike. The Fed downplayed the effects of dollar strength and oil weakness calling then reversible and temporary. The Fed's Vice Chairman has been vocal about how the U.S. markets are too complacent and that the Fed plans four rate hikes for this year, acceding to the notion of data-dependency along the way, even though that did not prevent the first hike from occurring. Since the Fed has done those things, markets have unraveled; the oil price drop has accelerated. The Fed is at risk of being another one of those central banks that tried to raise rates but was forced to rescind the rate hike. Certainly the Fed is going to have to recalibrate its forward guidance. Monetary policy worldwide is on autopilot on full stop stimulus. And yet it does not seem to do much good and only breeds malcontent among those who continue to believe in traditional inflation models.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief