Global| Feb 06 2015

Global| Feb 06 2015German Output Advances

Summary

German industrial production keeps dialing up positive growth rates even if they are small gains. The sequential growth rates from one-year and in show overall output accelerating, moving up from -0.4% of 12 months to an annualized [...]

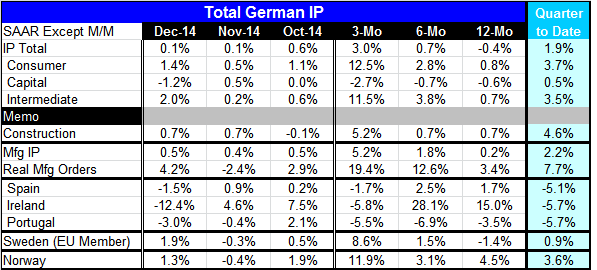

German industrial production keeps dialing up positive growth rates even if they are small gains. The sequential growth rates from one-year and in show overall output accelerating, moving up from -0.4% of 12 months to an annualized pace of 3% over the most recent three months.

German industrial production keeps dialing up positive growth rates even if they are small gains. The sequential growth rates from one-year and in show overall output accelerating, moving up from -0.4% of 12 months to an annualized pace of 3% over the most recent three months.

However, the picture of annual rates of growth by sector still reveals a lot of lethargy. Indeed, even the `acceleration' to a 3% pace over the recent three months is a hardly strong growth.

There is strong output growth in the German consumer goods sector where IP is advancing at a 12.5% annual rate over three months. This contrasts to the usual backbone of German industry, capital goods, where output trends are decelerating and output is shrinking at a 2.7% pace over three months.

The German construction sector is advancing and accelerating at a 5.2% annual rate over three months. Construction output is up for two months running.

For all of manufacturing, output is also accelerating and advancing at a 5.2% annual rate over three months. Moreover, real manufacturing orders that tend to precede trends in manufacturing show stronger acceleration in train, rising at a 19.4% clip over three months after posting a 12.6% annual rate over six months.

Early EMU reporters are few and far between. Ireland that has been strong but also mercurial was off by 12.4% in December following simple monthly gains of 4.6% in November and 7.5% in October. Spain posted a surprise drop of 1.5% in December. Portugal's IP also dropped. All three show net negative IP growth rates over three months, but only Portugal is also falling on balance over 12 months.

The recently completed quarter finds German output rising at a 1.9% pace with manufacturing up at a 2.2% pace and construction output up at a 4.6% pace. In the quarter, manufacturing orders are up at a 7.7% pace.

Events in the EMU still have debt negotiations with Greece in flux and region is set to meet and talk about Greece on February 11. Meanwhile, a peace initiative is being promoted by Hollande and Merkel for Ukraine. There is for now a ceasefire in place as they shop the pan to Putin.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.