Global| Jun 07 2021

Global| Jun 07 2021German Orders Tick Lower in April

Summary

German orders ticked lower in April, dropping by 0.2% on weak domestic orders that fell by 4.3%; foreign orders in April rose by 2.7%. Both foreign and domestic orders were up strongly in March. Domestic orders also rose strongly in [...]

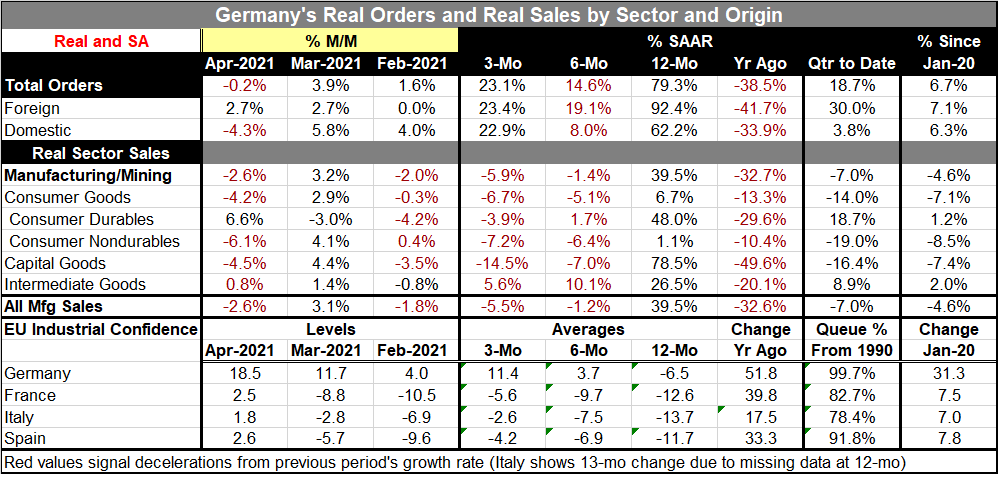

German orders ticked lower in April, dropping by 0.2% on weak domestic orders that fell by 4.3%; foreign orders in April rose by 2.7%. Both foreign and domestic orders were up strongly in March. Domestic orders also rose strongly in February when foreign orders were flat. As a result, the annualized three-month rates of growth show nearly identical gains of more than 20% for both foreign and domestic orders. The German order series seems to be very strong and solid.

German orders ticked lower in April, dropping by 0.2% on weak domestic orders that fell by 4.3%; foreign orders in April rose by 2.7%. Both foreign and domestic orders were up strongly in March. Domestic orders also rose strongly in February when foreign orders were flat. As a result, the annualized three-month rates of growth show nearly identical gains of more than 20% for both foreign and domestic orders. The German order series seems to be very strong and solid.

Over six months foreign orders are rising at a 19.1% pace while domestic orders are up at an 8% pace. Total orders are up at a 14.6% pace.

The 12-month gain is huge owing to comparisons with the year-ago period when Covid-19 struck and everything was shut down. Instead look at the raw gain from January. From January, both foreign and domestic orders are up by similar amounts: 7.1% for foreign orders compared to 6.3% for domestic orders. Total orders are up by 6.7%. These are solid gains for a 15-month period.

The German real sector sales data show broad sector declines in April following across the board strong gains in March. But March had followed a month of broad declines in February. As a result of all these choppy gains and losses, real sector sales are falling over three months in all sectors except for intermediate goods; but intermediate goods sales are decelerating over three months compared to six months. Over six months real sector sales in manufacturing slow and they also slow broadly although gains are stronger over six months for durable goods and for intermediate goods. Real sector sales are, like orders, up very strongly compared to their April 2020 levels. A better comparison is with January levels of real sales. That shows that sales are still behind their January levels by 4.6% overall. But as always, orders point the way ahead and they are pointing higher.

The quarter-to-date readings echo these same findings as orders are strong in the QTD period, but sector sales are falling. The discrepancy is quite sharp, but then Germany is only one month into its Q2 period.

The table also includes the EU Commission industrial confidence readings for the four largest economies in the EMU: Germany, France, Italy, and Spain. These show positive readings for each of these countries in April. And the averages show a progression toward strength from 12-month to six-month to three-month that sweeps across all four of these countries. Each of them shows a large gain over the past 12 months, both because of good ongoing gains and because of the weak base value for 12-months ago.

The rankings for industrial confidence are strong across all four countries. Germany is posting its strongest ranking since January 1990. But all the industrial values are solid; Italy has the weakest reading and it has a 78.4 percentile standing which is still quite good. Between the levels of the EU indexes and the momentum being logged, the industrial picture in Europe is quite solid.

Additionally, the gains since January 2020 show a massive jump of 31.3 points for Germany compared to smaller but highly similar gains of 7 to 7.8 points for France, Italy, and Spain over the same period.

For some time, the industrial data have been much stronger than the service sector and other eco-metrics. This month’s reports keep that process intact. The industrial sector data for Europe are solid. Despite a small setback in orders for Germany, its industrial sector seems quite secure in its ongoing, strong, rebound.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief