Global| Sep 06 2016

Global| Sep 06 2016German Orders Tick Higher

Summary

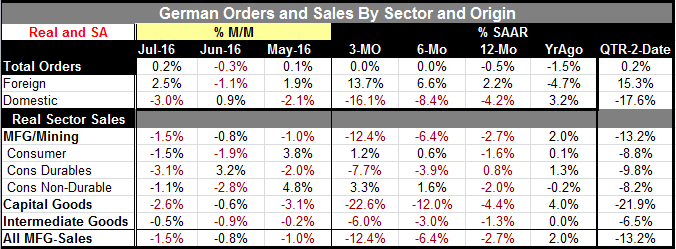

German orders continue their run of weakness rising by 0.2% in July after falling by 0.3% in June and after rising by 0.1% in May. Orders on balance are flat over 3-months and flat over six months and are lower by 0.5% over 12-months. [...]

German orders continue their run of weakness rising by 0.2% in July after falling by 0.3% in June and after rising by 0.1% in May. Orders on balance are flat over 3-months and flat over six months and are lower by 0.5% over 12-months.

German orders continue their run of weakness rising by 0.2% in July after falling by 0.3% in June and after rising by 0.1% in May. Orders on balance are flat over 3-months and flat over six months and are lower by 0.5% over 12-months.

Domestic new orders fell sharply by 3% in July and after dropping at a 6% annual rate over 3-months accelerating a downward move that has them falling at an 8.4% pace over six months and lower by 4.2% over 12-months.

Foreign orders were the counter weight this month as they surged by 2.5% after dropping by 1.1% in June. Foreign orders are up at a 13.7% annualized pace over 3-months and at a 6.6% pace over six months but are advancing only 2.2% over 12-months. New orders from the euro area were up 5.9% on the previous month; new orders from other countries increased by 0.6% compared to June 2016.

The manufacture of intermediate goods saw new orders unchanged in real terms (as always, adjusted for seasonally fluctuations and working-day variations) compared with June 2016. New orders for capital goods increased by 0.8% over their level of the previous month. Consumer goods saw a decrease in new orders of 4.3%.

Real sector sales show declines in manufacturing and mining overall in July. There are declines in consumer durables, in capital goods and for all manufacturing. Sales are falling on an accelerating basis at a 12.4% annual rate over three months, at a 6.4% annual rate over six months and at a 2.7% annual rate over 12-months. Sales are net lower year-over-year in all categories and on all horizons except for consumer goods and consumer nondurable goods.

In the quarter-to-date sales are falling in all sectors and falling overall at a 14.2% annual rate. Orders tick up at a 0.2% annual rate in the nascent quarter with plunging domestic orders offset by surging foreign orders.

Global conditions- still outrageously stifled

The recently released global PMI data show that global weakness continued in August. It was not a good month for global growth or trade. The JP Morgen total Global PMI for August ticked higher to 51.6 from 51.5 posting a level that is in the lower 23% of all values logged over the last five years, an extremely weak relative standing and that while being compared to a largely disappointing period of growth. Emerging markets also largely spun their wheels as the HSBC Emerging Markets Index edged lower to 51.6 from 51.7 but that level represents a 48 percentile standing over its last five years. Despite weakness among a large group of countries for which these indices are available, only France, the UK, Brazil and Hong Kong showed values below 50 (indicating contraction) in July. The UK and France moved up to register expansion in August while Japan slipped back to a sub-50 reading in August. As for manufacturing, a broad unweighted average for a large group of countries has been under a value of 51 since March of 2015. An weighted average of the composite index for the BRIC counties is below 50 in July and August.

On balance global growth remains weak. Despite all the actions by central banks, actions which have been ongoing for some time now, there is no sign of any stirring even in the sensitive PMI data either for the composite index or for either manufacturing or service sector components for developing or developed nations. While recession does not seem to threaten, the picture is nonetheless grim and the situation is a breeding ground for trouble.

G-20 meeting...Is it fooling itself?

The G-20 meeting in China concluded and the Chinese are calling it a success because they did not have the attention relentlessly focused on their South China Seas intransigence. And while there were the usual warnings not to succumb to the evils of protectionism, under the surface there seem to be more concerns than there were agreements out in the open. Such is the nature of diplomacy. China is itself is seen has having made it more difficult for foreign firms to operate there despite its own rhetoric in favor of freer trade, more transparency and less protectionism. Interestingly while there was a real focus at least in terms of rhetoric on trying to maintain impediment-free trade and on its importance, there are still no steps taken at all to assure that trade when it does occur occurs at something close to the proper market-determined exchange rates. Until or unless that can be assured trade expansion actually might not even be a worthy goal. And the G-20 leaders appear to be oblivious to that possibility - although the two primary U.S. presidential candidates are not.

Wrap up on Germany

Germany is an economy that has relied on trade. It has a good deal of trade in the euro-area as well as outside of it. It also runs a substantial current account surplus on its trade accounts. The industrial order data for July demonstrate how the weak global environment is beginning to take a toll on the German economy, despite its strong standing in terms of global efficiency. The weakness in its domestic economy has to be taken as a knock-on effect from ongoing global weakness since the German economy is manufacturing and export-oriented. In fat its wholly domestic construction sector is doing extremely well even in the face of such weak growth. Over the past year international orders are up while domestic-sourced orders are down. But neither series is very impressive. Global manufacturing remains impaired with various sectors dogged by huge excesses in capacity especially steel.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief