Global| May 06 2010

Global| May 06 2010German Orders Take A Strong Hold On Growth

Summary

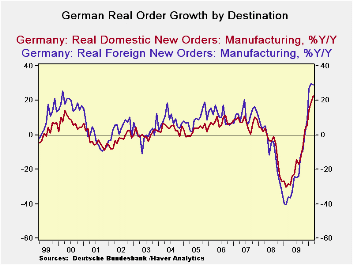

In March German orders spurted beyond expectations rising by 5% after being flat in February. Foreign orders built on a 1.7% gain in February rising by 4.7% in March. Domestic orders spurted by 5.4% coming off a 1.7% decline in [...]

In March German orders spurted beyond expectations rising by 5% after being flat in February. Foreign orders built on a 1.7% gain in February rising by 4.7% in March. Domestic orders spurted by 5.4% coming off a 1.7% decline in February. Over three months domestic and foreign orders are growing at almost identical 48% compounded growth rates; over six month their growth is clearly identical as well. Yr/Yr foreign orders are stronger, rising by 29% compared to nearly 23% for domestic orders. German orders are strong no matter how you slice them. But not all sectors are strong.

Consumer orders remain mixed in Germany. Consumer durables goods orders did better in March by reducing the pace at which they declined to -0.7% from -2.4% in February. Consumer durable goods orders are rising over three months, however, at a compounded annual rate pace of just 3.7%, up from 1.8% over six months. Consumer nondurables orders spiked by 5.4% in March, after dropping by 2.2% in February. They are still declining at an 8.2% annual rate over three months, however.

Capital goods are the backbone of the German recovery. Those orders rose by 2.4% in March after rising by 0.5% in February. Over three months capital goods orders are rising at a 24.7% pace up from an 11.7% pace over six months and from 6.7% Yr/Yr.

Intermediate goods orders also rose in March making gains of 2.8% after edging lower by 0.3% in February. Intermediate goods orders spurted at a 21% annual rate over three months compared to rising at a 10% over three months.

Manufacturing sales also were strong in March and their sequential growth rates show persisting strength.

On balance German orders were an upside surprise. The strength remains in the industrial sector with consumer goods starting to break out of their declining ways but still not clearly shaking off the lethargy. Orders grew at a 28% annualized rate in the quarter while sales grew at a 5% pace.

The weakening euro is going to help cement these trends as long as the financial problems in Greece do not spread too much and damp growth in the e-Zone and the surrounding environs. Right now tensions are running high as Moody’s warned on potential banking sector problems as banks hold a lot of government bonds and it is some of the debt-ridden European government‘s that issued those bonds that are under ratings pressure. If debt reschedulings were to occur there could be losses pushed onto bond holders and slapped onto bank balance sheets. In its meeting today the ECB held rates steady but that was all it held steady. So far it is not willing to do nay more, much to the markets consternation. Nervousness in the European markets is clear. The potential for knock-on effects even to an economy like Germany that seems to be doing so well is a real risk.

| German Orders and Sales By Sector and Origin | ||||||||

|---|---|---|---|---|---|---|---|---|

| Real and SA | % M/M | % Saar | ||||||

| Mar-10 | Feb-10 | Jan-10 | 3-MO | 6-Mo | 12-Mo | YrAgo | QTR-2-Date | |

| Total Orders | 5.0% | 0.0% | 5.2% | 49.1% | 22.1% | 26.0% | -32.8% | 28.5% |

| Foreign | 4.7% | 1.7% | 3.8% | 48.7% | 21.9% | 29.0% | -36.2% | 28.5% |

| Domestic | 5.4% | -1.7% | 6.7% | 48.9% | 22.0% | 22.8% | -28.6% | 28.2% |

| Real Sector Sales | ||||||||

| MFG/Mining | 2.9% | -0.2% | 1.2% | 16.3% | 7.8% | 8.5% | -21.8% | 5.6% |

| Consumer | 4.6% | -2.1% | -4.0% | -6.8% | -3.5% | 2.5% | -11.3% | -6.8% |

| Cons Durables | -0.7% | -2.4% | 4.1% | 3.7% | 1.8% | 5.4% | -22.7% | 6.4% |

| Cons Non-Durable | 5.4% | -2.2% | -5.0% | -8.2% | -4.2% | 2.1% | -9.4% | -8.6% |

| Captial Gds | 2.4% | 0.5% | 2.6% | 24.7% | 11.7% | 6.7% | -24.5% | 12.9% |

| Intermediate Gds | 2.8% | -0.3% | 2.3% | 21.0% | 10.0% | 15.2% | -24.4% | 4.6% |

| All MFG-Sales | 2.7% | -0.2% | 1.2% | 15.7% | 7.6% | 8.3% | -21.7% | 5.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief