Global| May 06 2021

Global| May 06 2021German Orders Spurt... Will Sales Follow?

Summary

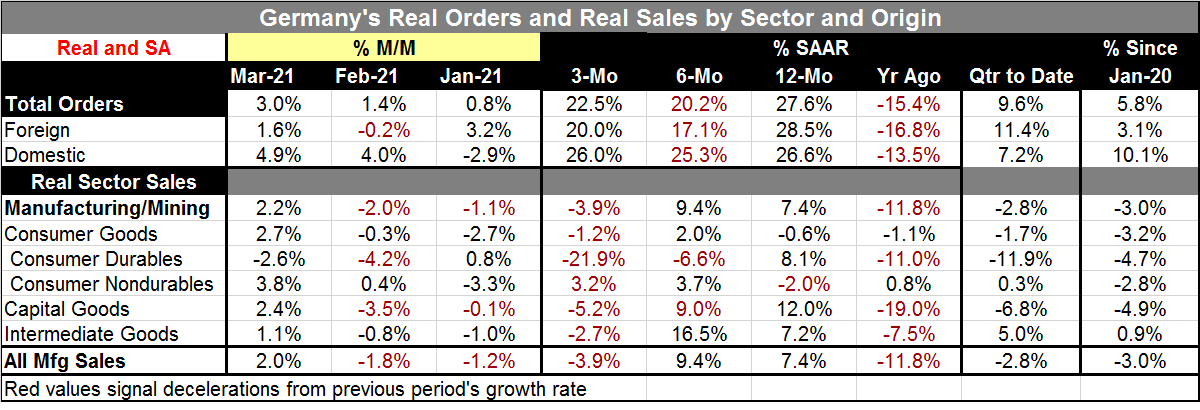

German orders surged in March rising by 3% after gaining by 1.4% in February and 0.8% in January. The surge was being pushed ahead by domestic orders that spurted by 4.9% in March after a substantial 4% boost in February, a surge that [...]

German orders surged in March rising by 3% after gaining by 1.4% in February and 0.8% in January. The surge was being pushed ahead by domestic orders that spurted by 4.9% in March after a substantial 4% boost in February, a surge that was in part a rebound from a 2.9% drop in January.

German orders surged in March rising by 3% after gaining by 1.4% in February and 0.8% in January. The surge was being pushed ahead by domestic orders that spurted by 4.9% in March after a substantial 4% boost in February, a surge that was in part a rebound from a 2.9% drop in January.

Orders on a tear

From August 2020, orders have generally been on a tear with domestic orders as well as foreign orders each falling in only two of eight months over that span. Both order series showed their last sharp losses in April 2020. Since that low point in April, foreign orders have risen by 84% and domestic orders have risen by 68%. Over the last six months, foreign orders have risen by 8% and domestic orders by 12%.

An economy plugged into globalism

Germany has tapped into the international economy for its growth. German foreign orders rise faster than domestic orders over most any long stretch of time. The ratio of foreign to domestic orders has structurally risen. Foreign order growth has exceeded domestic order growth over six of the last eight intervals of six quarters in length. However, over the last two months, it has been domestic orders that have broken out with strong growth as foreign orders have cooled.

During this period, differences in foreign/domestic rates of order growth are almost certainly predominately caused by differences in an economy’s openness or closed state because of the virus.

Order trends

Order growth rates annualized are at 22.5% over three months, 20.2% over six months and 27.6% over 12 months. That is very strong and consistent growth. The bases for those calculations are December, September 2020 and March 2020, respectively. That accounts for the all the strength since these periods are nearly all post-virus (the 12-month calculation takes in one month of sharply falling orders/sales).

Comparison to pre-virus

Note that orders overall, as well as for foreign and domestic components separately, are higher on balance than their previous levels of January 2020. By comparison, real sales are still 3% below their levels of January 2020. And all sales components are lower on balance except for intermediate goods.

Sales trends

Trends in real sales are much more equivocal than for orders. Total real and foreign orders each are growing strongly over three months, six months and 12 months. For real sector sales among the several headlines and components, six are declining over three months, and one declines over six months as well as over 12 months. Real sector sales are relatively strong over the longer periods that give them the advantage of comparison to periods that were very weak. But the growth rates over the last three months do not have that advantage and as a result the recent momentum for sales is mostly contracting.

Orders lead

However, orders usually call the tune for growth. The chart (at the top) shows that orders generally lead sales and that sales do follow that lead.

The virus caveat

However, as we have seen time and gain what matters for the period ahead is what the virus does. India is a reminder that even if the virus has one wave that does not mean that the next wave can’t be worse. Most Western countries have had second waves (or more) and in most cases the second wave brings a new peak of infections but a lower death rate. India is an exception to that. India is now blaming a new variant for its problems. The fact that Europe is under-vaccinated makes me less eager to jump on any positive industrial trend and anoint it as the truth. Europe is still vulnerable. And as we can see with Spain wanting to open up for its vacation-dependent economy, Europe still wants to ‘normalize’ and it wants this even though it is at risk to normalization. That will be something to watch closely.

Summing up

For now Germany has another wave in progress; it has not out-peaked its second wave in terms of the rate of infections. And the death rate from it has been muted. So far Germany tells a story of acquiring more natural immunity and at a much lower cost than India. But the risks are still there and the vaccinations are still behind schedule. Industrial trends should continue to extend their gains if the virus continues to behave. That is what to watch.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief