Global| Sep 04 2020

Global| Sep 04 2020German Orders Slow Sharply

Summary

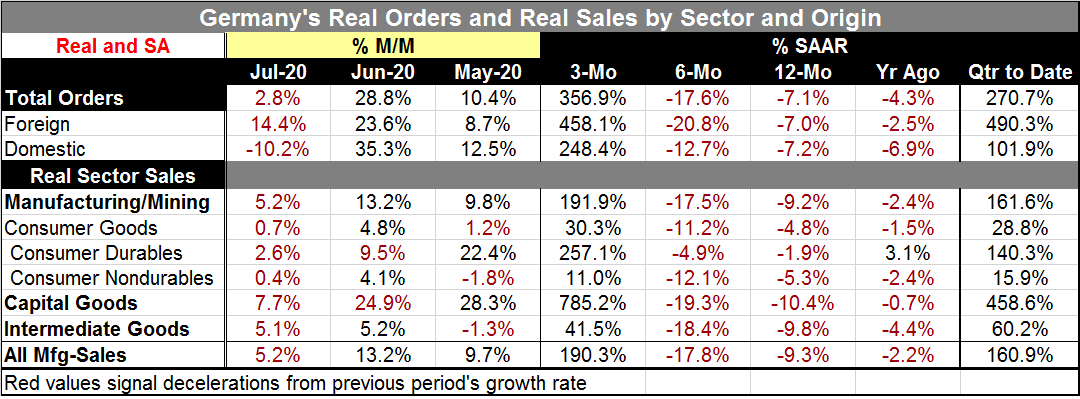

German orders rose by 2.8% in July but are still lower over 12 months by 7.1%. This is a sharp slowing from the 28.8% one-month jump orders made in June. Both foreign and domestic orders slowed in July. Foreign orders rose by a still- [...]

German orders rose by 2.8% in July but are still lower over 12 months by 7.1%. This is a sharp slowing from the 28.8% one-month jump orders made in June. Both foreign and domestic orders slowed in July. Foreign orders rose by a still-robust 14.4% month-to-month, still a sharp deceleration from 23.6% in June. But domestic orders actually fell, dropping by an outsized 10.2% in July after rising by 35.3% (!) in June. Foreign orders are lower by 7.0% over 12 months while domestic orders are lower by 7.2% on that same timeline. Both domestic and foreign orders are lower over 12 months and were lower over 12-months one year ago, underscoring that the German economy is not just in a funk over the coronavirus but has been in a losing mode for some time.

German orders rose by 2.8% in July but are still lower over 12 months by 7.1%. This is a sharp slowing from the 28.8% one-month jump orders made in June. Both foreign and domestic orders slowed in July. Foreign orders rose by a still-robust 14.4% month-to-month, still a sharp deceleration from 23.6% in June. But domestic orders actually fell, dropping by an outsized 10.2% in July after rising by 35.3% (!) in June. Foreign orders are lower by 7.0% over 12 months while domestic orders are lower by 7.2% on that same timeline. Both domestic and foreign orders are lower over 12 months and were lower over 12-months one year ago, underscoring that the German economy is not just in a funk over the coronavirus but has been in a losing mode for some time.

The sequential growth rates do not add a lot to the story. They show orders of all sorts falling over 12 months. Growth rates are falling over six months then skyrocketing from a period of extreme weakness three-months ago to post some really eye-popping growth rates in triple digits. That strength carries through, of course, to the incipient quarter-to-date growth rates that also show triple-digit growth for total orders, domestic orders and foreign orders one month into the third quarter (on a quarter-to-date basis).

The coronavirus – or more correctly, the response to the coronavirus- is responsible for these setbacks. The virus struck, slammed the economy, there was a recovery, and then another outbreak and an economic breaking. That is the main reason that so many of these figures are behaving more or less the same way. All sectors are affected. Some are affected more than others. Since this is an industrial report we do not see the impact of the virus on the services sector directly, but that has been worse and that sector has also been much slower to recover and although we do not observe its impact here directly, it has helped to hold back recovery in industry as well.

Sector sales trends show us more industrial detail. But here the main points are all the same. Sales decline over 12 months. They decline faster over six months. They show various degrees of growth over three months. Capital goods and consumer durable goods are showing the fastest real sales recovery over three months. Intermediate goods sales are rising at a 41.5% annual rate over three months, less than triple-digits. Consumer nondurable purchases are up at just an 11% annual rate.

On balance, the trends have been turning higher very rapidly and strongly until this month. Economists always say ‘one month does not determine a trend’ (...such wisdom!), but in this case the past trend was so strong and this month’s slowing so marked that seems to be a clear marker for an inflection point for the growth rate.

The re-infection by the virus in Germany, the rest of Europe, and elsewhere, is having its impact and slowing growth...again. But this is the reality of our agreed way to deal with the virus. If containment is the strategy and given that the ‘nature of the virus’ is contagious and hard to play defense against, it will occasionally get loose, create a bubble of infection and something will have to get shut down to contain it. We are on what Chuck Todd has called the hamster wheel or what I have called the hokey-pokey process of growth. We have an endless cycle of open up and shut down with little overall change in the proportion of infection made because each time we try to restrict growth of the infection so the infection at each cycle end progresses very little in extending the ranks of the infected –and that is a matter of policy. And that policy keeps the number of those uninfected large like a bundle of dry tinder waiting to be set ablaze by the next spark of virus – which we know will occur. And so it goes.

I suppose one bit of good news is that the Russian vaccine has been shown to generate an antibody response. That is something. We still do not know how effective or safe any of the vaccine candidates are going to be. Until we clarify that, spin the hamster wheel and dance the hokey-pokey. It’s the new reality. Happy Labor Day holiday to all. And be kind…don’t make someone ask where you left your mask… Right or wrong it is the new reality, so play along.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief