Global| Jul 06 2015

Global| Jul 06 2015German Orders Sink Slowly in May as Foreign Orders Stay Firm

Summary

The euro area, perhaps also to be known as the land of bifurcation, has just witnessed a vote in which the Greek people have rejected the EU austerity plan, leaving much of the future for Greece and the euro area itself in limbo. The [...]

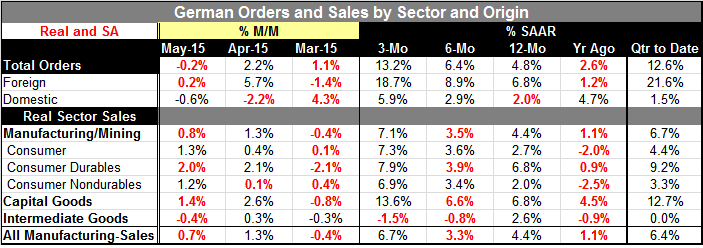

The euro area, perhaps also to be known as the land of bifurcation, has just witnessed a vote in which the Greek people have rejected the EU austerity plan, leaving much of the future for Greece and the euro area itself in limbo. The German economy that has been the backbone of Europe, meanwhile, appears to be much less of a locomotive of growth and much more a parasite on the world and on the EMU itself. German overall orders fell by 0.2% in May after rising strongly by 2.2% in April. Foreign orders were the driver of growth with a 0.2% increase, offsetting some of the 0.6% drop in German domestic orders. Over three months, foreign orders are up at an 18.7% annual rate. Year-over-year foreign orders are up by 6.8%, compared to domestic orders that are crawling ahead at a 2% pace.

The euro area, perhaps also to be known as the land of bifurcation, has just witnessed a vote in which the Greek people have rejected the EU austerity plan, leaving much of the future for Greece and the euro area itself in limbo. The German economy that has been the backbone of Europe, meanwhile, appears to be much less of a locomotive of growth and much more a parasite on the world and on the EMU itself. German overall orders fell by 0.2% in May after rising strongly by 2.2% in April. Foreign orders were the driver of growth with a 0.2% increase, offsetting some of the 0.6% drop in German domestic orders. Over three months, foreign orders are up at an 18.7% annual rate. Year-over-year foreign orders are up by 6.8%, compared to domestic orders that are crawling ahead at a 2% pace.

The German economy, one of the best growth stories in Europe, is making its growth go by tapping into domestic demand in countries less fortunate than itself. Meanwhile, Germans are the harshest critics of Greece and its foundering economy. Greece's GDP has dropped by 25% from tis peak and still austerity is deemed not to have been enough.

The euro crisis has pushed the euro exchange rate even lower, further enhancing German competiveness outside the euro area. The euro crisis has been very good for German exports at least to those outside of the monetary union. Even then, we must qualify that by mentioning the adverse effect of sanctions on Russia and the adverse effect of China's slowdown on demand and on German exports to those destinations. But then, simple currency depreciation can do only so much.

German shipments inside the euro area fell in May while shipments to foreign countries outside the euro area increased. However, German exports to destinations inside the euro area are up by 9% over 12 months while exports to countries outside the euro area have increased by only 5.5% on that timeline. Despite the fall in the euro, Germany has had more export success over the past year within the euro area where economic conditions have been very uneven.

Meanwhile the euro area faces some huge issues this week as Greece has rejected the EU austerity plan. While Greece has suffered much since austerity was imposed, it has fought austerity every inch of the way and has clung to keeping social payments intact and trying to hike taxes rather than to pursuing pro-growth polices as Ireland has done so successfully. As a result, Greece today is in terrible shape and blames the austerity plan while Europe sees Greece as still failing to impose the kind of austerity that could help it recover, live within its means, and grow its own economy successfully.

These two views are like night and day. They explain also why Greek PM Alexis Tsipras could say a `no' vote was not a vote to leave the EMU while other Europeans said just the opposite. Greece and Europe have failed to communicate for some time. Both talk; neither listens.

Needless to say, the future of Europe's growth and the prosperity of member countries, including Germany, are going to depend on how the EU/EMU/ECB/IMF decide to end this crisis. There are many paths to worse economic times ahead and relatively few paths to better times. Will Europe be able to pull a rabbit out of its hat, or will Greece follow its PM down the rabbit hole to drachma land?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief