Global| Jan 08 2020

Global| Jan 08 2020German Orders Sink But the Outlook Remains Mixed

Summary

Reports for the New Year continue to come in emitting erratic signals. Global PMI data from Markit remain weak with poor momentum but also throw out some hints of stabilizing. In the U.S., the ISM is delivering a split decision but [...]

Reports for the New Year continue to come in emitting erratic signals. Global PMI data from Markit remain weak with poor momentum but also throw out some hints of stabilizing. In the U.S., the ISM is delivering a split decision but still with poor standings for both surveys. This orders report for Germany is an important indicator as well. Germany is a highly industrialized economy and is more plugged into the global trading system than any other large economy. In November, it shows consistent weakness but with some evidence of improvement in domestic orders.

Reports for the New Year continue to come in emitting erratic signals. Global PMI data from Markit remain weak with poor momentum but also throw out some hints of stabilizing. In the U.S., the ISM is delivering a split decision but still with poor standings for both surveys. This orders report for Germany is an important indicator as well. Germany is a highly industrialized economy and is more plugged into the global trading system than any other large economy. In November, it shows consistent weakness but with some evidence of improvement in domestic orders.

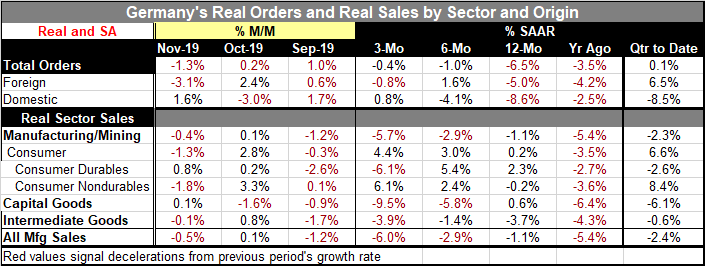

Total German orders rose in both September and October. But in November overall orders are falling again, dropping by 1.3% on split trends between domestic and foreign order sources. Foreign orders were up for two months running ahead of November while domestic orders were saw-toothed. Foreign orders have been peppered with sharp declines and several modest or stronger monthly increases for intervening months. Domestic orders ended a string of persistent declines in April and have been saw-toothed ever since.

These erratic behaviors have left overall orders falling over three months, six months and 12 months but falling at a reduced, decelerating pace sequentially. Foreign orders fell sharply over 12 months but made a net gain over six months and are falling at a pace of less than 1% over three months. Domestic orders show secular improvement with a net gain in orders of 0.8% over three months.

However, durable trends are hard to pin down since both domestic and foreign orders have tendencies that are somewhat unstable. The chart shows that year-over-year trends are negative with foreign orders trending upward toward smaller declines and domestic orders sinking toward deeper declines.

Quarter-to-date total orders are up at a 0.1% annual rate in the new quarter (Q4). Foreign orders are rising at a 6.5% pace quarter-to-date. Domestic orders are sinking at an 8.5% annualized rate in the quarter with one month left to go.

Real sector sales show that overall manufacturing sales are lower in November and negative over 12 months, six months and three months with growth rates getting progressively weaker over more recent periods. The manufacturing sales trends tell a clear story of weakening trends while the orders stories tell tales of mixed weakness. Possibly this means that legacy weakness is going by the boards as the orders series which is more forward-looking and less weak than sales per se.

Within sectors consumer sales are on the rise and clearly accelerating from 12-months to six-months to three-months. Consumer nondurables underpin this trend with durables showing improvement except for a reversal and sharp drop in sales over three months. Capital goods show secular deterioration in growth rates. Intermediate goods show negative growth rates on all horizons, but there is a growth improvement from 12-months to six-months followed by a relapse of weakness over three months.

The sector sales show that there is a good deal of weakness. But it is not uniform as might be expected if there were an economic downturn progressing. The strength in consumer sales is a notable exception. Weakness is lodged in capital goods especially over three months and six months.

The developing patterns of sales and orders are still not clear and after an extended period of weakness that by itself may be a good sign. Weakness still is not cumulating and the consumer sector has been able to sustain its momentum. This speaks to wage gains, and the ongoing job growth globally that has spread the resistance of the job market to increases in unemployment. Right now that is looking like the dividing line or barrier to the development of recession and to the spreading of this weakness.

However, the Baltic dry goods index has continued its run of weakness. The freight index has fallen for the 20th straight session to an eight-month low. The Baltic index speaks to a global environment of continuing weakness for the trade in goods. It is to some extent at odds with the orders data in the German report that show a lessening in downward order trends compared to sales. However, there are lingering questions and as yet undeveloped trends in the German data as we saw above.

However, the Baltic dry goods index has continued its run of weakness. The freight index has fallen for the 20th straight session to an eight-month low. The Baltic index speaks to a global environment of continuing weakness for the trade in goods. It is to some extent at odds with the orders data in the German report that show a lessening in downward order trends compared to sales. However, there are lingering questions and as yet undeveloped trends in the German data as we saw above.

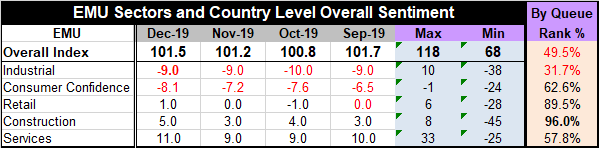

The European Commission indexes for the EMU shed light on these observations. They show the overall EMU gauge at a rank of 49.5%, just below its midpoint on data back to 1988. The industrial data featured in the German orders report pertain to the weakest sector in the EMU. Meanwhile, retail sales in the EMU continue to post an 89th percentile standing and consumer confidence a 62.6 percentile standing. The construction sector is even stronger at a 96th percentile standing. Services, however, come in weaker at a 57th percentile standing.

There has not been much additional slippage in these various sectors since September. Only consumer confidence has seen its assessment fall on balance over those four months. And current readings, while weak in ranking, are very far from the sorts of lows they have tended to in past recessions. On balance, it looks like there is a slowdown that is still in place. Time will tell if there is enough positive news in the U.S.-China trade deal to provide any real lift to the global economy. German should be a good litmus test for that.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief