Global| Dec 04 2015

Global| Dec 04 2015German Orders Show First Growth in Four Months

Summary

German orders snapped a three-month losing streak to rise by 1.8% in October month-to-month. Both foreign and domestic order rose in October. Foreign orders had fallen for three months in a row previously and domestic orders had [...]

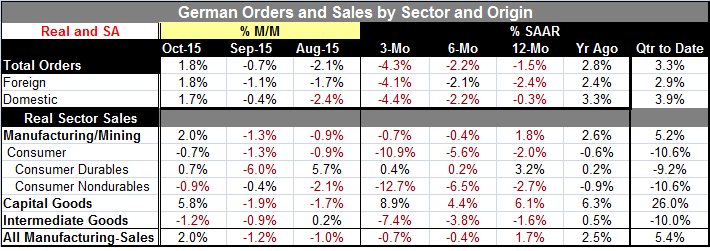

German orders snapped a three-month losing streak to rise by 1.8% in October month-to-month. Both foreign and domestic order rose in October. Foreign orders had fallen for three months in a row previously and domestic orders had fallen for two months in a row.

German orders snapped a three-month losing streak to rise by 1.8% in October month-to-month. Both foreign and domestic order rose in October. Foreign orders had fallen for three months in a row previously and domestic orders had fallen for two months in a row.

The order trends from 12-month to six-month to three-month show ongoing weakness and order declines across the breadth of the categories for total orders, foreign orders and domestic orders. The escape from weakness is only in the gains in October. There is no telling if they will have any legs.

Real sector sales in Germany show a proliferation of gains but also some important sectors with ongoing weakness. Manufacturing and mining saw sales rise in October and so did manufacturing alone. Capital goods sales were up a strong 5.8%. Consumer durables showed real sales gains in October, but there are still declines in consumer nondurables and for consumer goods sales overall. Intermediate goods real sales were lower in October and are sharply lower over three months.

The sequential pattern of real sales shows weakness and progressive weakness in all sectors except consumer durables and capital goods.

The Bundesbank today refreshed its forecasts and did not cut its outlook. It is looking for exports to pick up and for GDP to expand by 1.7% this year and by 1.8% in 2016. Up to this point, most forecasts, whether made by central banks or by international organizations, have been cutting back their view of the future. Germany takes the lead in keeping its outlook unchanged.

Of course, Germany is already the best performing economy in the EMU and the ECB has just announced a program of stimulus. However, markets did not react positively to the ECB's news yesterday. Time will tell if the global environment has improved enough to allow Germany to exploit its competitiveness advantage in the export market next year. And there is also the issue of Volkswagen and early evidence that VW vehicle sales are being affected by its corporate difficulties. That sort of weakness could hit German exports hard. The Bundesbank's outlook at this point looks as though it might be optimistic.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief