Global| Nov 05 2015

Global| Nov 05 2015German Orders Send Ominous Signals

Summary

German orders send ominous signals as they drop for the third consecutive month in September. Orders are not just falling; they are decelerating with successively larger annualized negative rates of growth from 12-month to six-month [...]

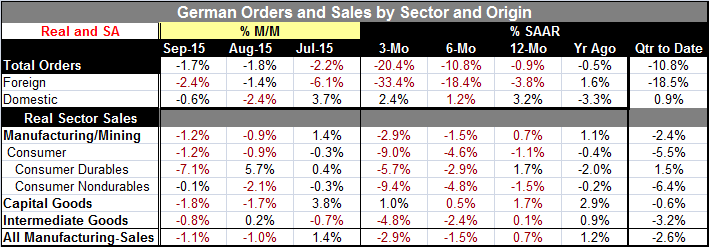

German orders send ominous signals as they drop for the third consecutive month in September. Orders are not just falling; they are decelerating with successively larger annualized negative rates of growth from 12-month to six-month to three-month. This weakness is led by the international sector where the three-month annual rate of decline is -33.4% and the six-month rate is -18.4%. German domestic orders are still hovering at low growth rates: 2.4% for three-month, 1.2% for six-month and 3.2% for 12-month.

German orders send ominous signals as they drop for the third consecutive month in September. Orders are not just falling; they are decelerating with successively larger annualized negative rates of growth from 12-month to six-month to three-month. This weakness is led by the international sector where the three-month annual rate of decline is -33.4% and the six-month rate is -18.4%. German domestic orders are still hovering at low growth rates: 2.4% for three-month, 1.2% for six-month and 3.2% for 12-month.

In the just-completed third quarter, orders are falling at 10.8% annual rate, led by a -18.5% pace of drop in foreign orders with domestic order eking out less than a 1% growth pace. Annual real sector sales are falling at a 2.4% annual rate; all of manufacturing has sales falling at 2.4% annualized pace. If not grim, the situation is not very good either in real time or as expected from orders good.

German real sector sales show declines for two months running. They also show progressive growth rate deterioration from 12-month to six-month to three month, with sales declining on balance over six-month and three-month. So conditions are poor in terms of current sales and conditions and are expected to worsen as depicted by orders. The weakness in German sales across various industries and time horizons is sobering.

This is not Greece. This is Germany. It is the most competitive developed economy in the world and its competiveness is being helped by the floundering euro exchange rate. But Germany's matrix of trade flows is hurting it as it finds itself with too much exposure to China as China slows sharply and as high end conspicuous consumption has come under scrutiny there. Germany's best export has been high-end automobiles. Germany is sure to get hit by the many problems being felt by its largest industrial company, Volkswagen, especially since its environmental cheating has just been demonstrated to have gone beyond its diesel engine products.

If Germany's factory sector is about to take a turn for the worse, what about the rest of Europe? The recent PMI indices for Europe were weak, albeit showing a creeping, slow-creeping, growth for the community as a whole. In data announced today, EMU-wide retail sales volumes fell in September after being flat in August.

Will the ECB step up its asset-buying operation? It is expected. But QE worked best where it was applied early and in the midst of crisis. The ECB -if it does step up its asset purchases- will be doing this in an environment with already low rates. And it is far from clear how economics are going to be affected if short terms rates run negative as a result.

For now this is policymakers' nightmare. Fiscal policy is set aside at a time when it might be the most effective tool because it has been overused in the past. Monetary policy has been used to the hilt instead. With moderate growth in the U.S. and lots of evidence of growth irregularities there, the Federal Reserve seems to be lowering the bar to a rate hike in December. Rate hiking in this environment is really a hard thing to understand. But it could wind up helping Europe as we have seen some upward move in the dollar and downward move in the euro as a result. Still, U.S. growth is weak and there will not be much of a market for foreign exports to penetrate there. One wonders about consumer acceptance of German-made cars under any terms in the coming months.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief