Global| Jul 06 2016

Global| Jul 06 2016German Orders Run Flat

Summary

German orders (all data in real terms) came up flat in May after a 1.9% decline in April. Despite the poor two-month run of orders, orders are still advancing at a 2.9% annual rate over three months and the real orders series actually [...]

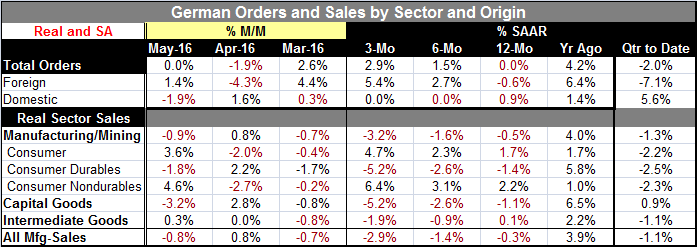

German orders (all data in real terms) came up flat in May after a 1.9% decline in April. Despite the poor two-month run of orders, orders are still advancing at a 2.9% annual rate over three months and the real orders series actually shows acceleration in train from 12-month (0%) to six-month (1.5%) to three-month (2.9%).

German orders (all data in real terms) came up flat in May after a 1.9% decline in April. Despite the poor two-month run of orders, orders are still advancing at a 2.9% annual rate over three months and the real orders series actually shows acceleration in train from 12-month (0%) to six-month (1.5%) to three-month (2.9%).

Foreign orders are the driving force for orders as they show acceleration from -0.6% over 12 months to a pace of 2.7% over six months to a pace of 5.4% over three months. Even though that sequence of growth rates seems to be a pretty clear signal, foreign orders have been volatile. The chart makes that clear as does the performance of the past few months which has seen foreign orders rise by 4.4% in March only to fall by 4.3% in April. It is hard to pin down what orders are in the process of doing. Over the last 18 months, foreign orders have been 33% more volatile than domestic orders. Still, foreign orders have not been especially volatile relative to their own history. Moreover, the share of orders divided between foreign and domestic orders has been relatively stable over the past few years. Foreign orders reveal good deal of compositional variability. They demonstrated strength from within the euro area this month where orders gained 4.0%. But orders from other foreign locations were off by 0.3%, subduing the impact on overall order trends.

Domestic orders are up by just 0.9% over 12 months and flat over three months and over six months. They have been subdued.

In May orders of intermediate goods were weak and fell by 2.9% month-to-month. Orders for capital goods rose by 1.9%. Consumer goods orders edged lower by 0.4%. The core of German orders strength remains lodged in capital goods.

The pace of real sales in Germany is contracting and decelerating. Consumer sector real sales are accelerating on the strength of nondurables while capital goods sales and intermediate goods sales both are contracting and decelerating.

Flat orders from Germany are not really good news. But strong orders from within the euro area are good news. Other European news today found Western European car sales up by 5.7% year-on-year despite weakness in the British market. Germany also reported its weakest construction sector PMI in 10 months. Industrial output in Spain slowed to a 1% pace its weakest year-on-year gain in more than one year.

Markets are feeling nervous this morning as sterling has hit a fresh 31-year low as Brexit issues continue to be digested. Sterling traded below 1.30 to the dollar, its weakest level since 1985. Stock markets are nervous, trading to the downside and bonds continue to post gains and hold to or near record low yields.

In this environment, German Chancellor Angela Merkel's cabinet met and decided to continue with its plan to balance the budget over the next four years. It is a time when the rest of Europe could use some added stimulus. Germany is one of the rare European economies with room to choose stimulus, but it has chosen not to do that. Ongoing German fiscal tightness will put pressure on other economies as it will tend to keep German prices low. But Germany already has a huge competitiveness advantage in the EMU. That advantage could be extended under this policy, further dividing the EMU.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief