Global| Jun 06 2019

Global| Jun 06 2019German Orders Rise for Second Month in a Row But Remain Weak

Summary

Germany's real new orders rose by 0.3% in April, marking the second monthly rise in a row as orders rose by 0.8% in March. Orders last rose two months in a row in September-October of 2018. A rebound- but still weak While this news is [...]

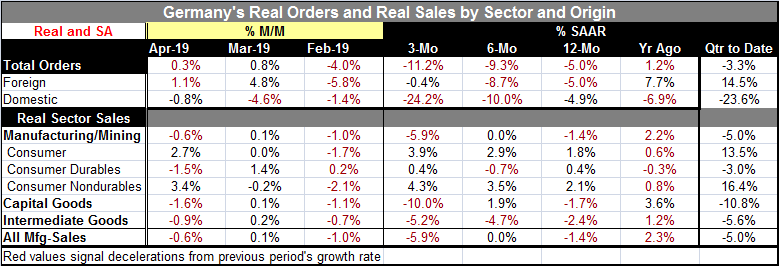

Germany's real new orders rose by 0.3% in April, marking the second monthly rise in a row as orders rose by 0.8% in March. Orders last rose two months in a row in September-October of 2018.

Germany's real new orders rose by 0.3% in April, marking the second monthly rise in a row as orders rose by 0.8% in March. Orders last rose two months in a row in September-October of 2018.

A rebound- but still weak

While this news is welcome, it is still not all that great. The quarter-to-date rise for Q2 that measures the April gain annualized over the Q1 base still shows a decline in Q2 2019. This is because the drops early in Q1 were so large that even with two months of gains in a row the first month in Q2 finds the level of orders below the Q1 average. Real orders, for example, are up by 1.1% over two months but were down by 4% in February alone.

Foreign vs. domestic trends

Foreign new orders are up for two months running. Domestic new orders are down for four months running. Foreign orders have enough strength that on a quarter-to-date basis they are rising early in Q2 at a 14.5% annual rate. However, domestic orders are falling at a 23.6% annual rate early in Q2.

New orders from the euro area were down 5.8% in April, while new orders from other countries increased 5.7% compared to March 2019. The weakness in the euro area is still quite severe judging from orders.

By industry

In April, the manufacturers of intermediate goods saw new orders fall by 0.4%, compared with March. Capital goods orders showed an increase of 0.9% on the previous month. Consumer goods, logged an increase in new orders of 0.1%. Clearly, whatever strength there is at the moment is being driven by capital goods orders. But with trade uncertainty so high, and concerns about the resolution of Brexit, there are still plenty of forces in play that could put a chill on capital goods orders.

Real sales by sector

Real sales data accompany the release for real orders data. Real sales data show mining and manufacturing real sales down by 0.6% in April, falling at a 5.9% annual rate over three months and declining at a 5.0% pace in the quarter-to-date.

Sector real sales are up in April for consumer goods by 2.7%, while falling by 1.6% for capital goods, and falling by 0.9% for intermediate goods. Over three months and 12 months, that same set of conditions prevails. Over six months, capital goods buck the pattern as sales rise. Quarter-to-date, consumer goods sales are up at a 13.5% pace while capital goods sales are falling at a 10.8% pace and intermediate goods are falling at a 5.6% pace.

Summing up

Clearly, real orders and real sales remain weak for Germany. Capital goods orders and sales show that uncertainty has not snuffed out all investment - at least not yet. The revival in foreign orders is all outside the EMU as EMU-area orders fell sharply in April. The quarter-to-date data demonstrate that the revival is not as yet applicable to Q2 results as even two monthly increases in a row in orders is leaving orders in a contracting mode for Q2. Germany's manufacturing sector is still floundering.

This is the same message we obtained from the Markit survey on German manufacturing for May. It's no wonder that the ECB is stretching out its estimate of how long rates will be on hold. Moreover, is this the right environment for the EU Commission to begin putting clamps on Italy to create more fiscal austerity? Based on remarks today the Germans still think so. But what will the EU Commission do besides warn Italy? Anything?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief