Global| Oct 06 2016

Global| Oct 06 2016German Orders Rise But Path Remains Listless

Summary

German orders rose by 1% in August, their second monthly gain in a row. It was the first back-to-back monthly gain since November. However neither domestic nor foreign orders have posted monthly gains back-to-back since March for [...]

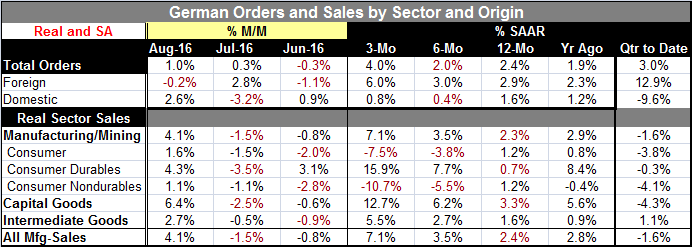

German orders rose by 1% in August, their second monthly gain in a row. It was the first back-to-back monthly gain since November. However neither domestic nor foreign orders have posted monthly gains back-to-back since March for domestic orders and January for foreign orders. The path of year-on-years order gains is still quite muted and its month-to-month success sits on a still-volatile base of domestic and foreign trends.

German orders rose by 1% in August, their second monthly gain in a row. It was the first back-to-back monthly gain since November. However neither domestic nor foreign orders have posted monthly gains back-to-back since March for domestic orders and January for foreign orders. The path of year-on-years order gains is still quite muted and its month-to-month success sits on a still-volatile base of domestic and foreign trends.

In the quarter-to-date, overall orders are rising at a 3% annualized pace with foreign orders spurting at a nearly 13% annual rate while domestic orders contract at a nearly 10% annual rate. With such underlying disparate trends, it is hard to confidence in the path for overall orders. Although today's report is being heralded as a watershed of sorts, that conclusion seems premature.

In August, intermediate goods new orders rose 1.7% compared with July 2016. Capital goods new orders increased 0.3% on the previous month. Consumer goods new orders gained 2.9% as all three categories of orders saw increases in orders of some sort on the month. Consumer goods are leading the way with the usual backbone of German orders, capital goods orders, lagging.

Orders inside the euro area were essentially flat in August. Orders from other countries fell by 1.2%. Intermediate goods orders inside the euro area gained 1.9% and from other countries rose by 0.7%. Capital goods orders from all foreign sources fell with euro area sourced orders falling by 1.5% and other foreign-sourced capital goods orders falling by a larger 3.7%. Consumer goods orders placed by foreign sources rose by 1.2% to euro area members. Outside the euro area, foreign orders for German consumer goods surged by 6.6%. The pick-up in consumer goods demand outside the euro area is particularly encouraging. But foreign demand from all sources for capital goods remains quite weak.

Real sector sales show weakening consumer sales trends and strengthening sales in capital goods. Intermediate products show mild gains but are gradually accelerating. In August all categories of sales saw increases led by strong capital goods sales.

With global growth still so weak, the WTO cutting its outlook for world trade growth, and the IMF warning about global risks, it's an environment in which to be cautious about drawing conclusions. Global PMI reports showed somewhat better manufacturing activity in their September report against a backdrop of mostly weakening service sector growth. That's mixed bag if ever I saw one. Of course, there have been upside surprises. The German IFO report for September was one; the U.S. ISM nonmanufacturing PMI was another. But until we see some positive trends developing, it is hard to take any of this as being all that upbeat. A one-off surprise is not the same as a string of strong data. And trends like that have simply not yet developed. We continue to look for anything that is really good news. So far, there is enough good news to keep the bad news at bay. But that continues to be a battle.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief