Global| May 09 2016

Global| May 09 2016German Orders Recover But Go Both North and South by Origin

Summary

German orders rose by 1.9% in March, their strongest gain since June of last year. But the gain came on a 4.3% spurt in foreign orders which only rebounded from a 2.1% drop in February. Domestic orders fell by 1.2% in March. And there [...]

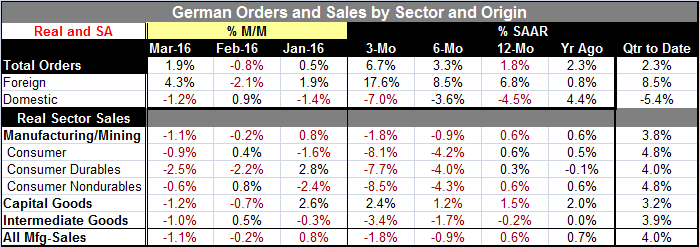

German orders rose by 1.9% in March, their strongest gain since June of last year. But the gain came on a 4.3% spurt in foreign orders which only rebounded from a 2.1% drop in February. Domestic orders fell by 1.2% in March. And there is a real schism between domestic and foreign orders and conditions not just a one month runaround. Foreign orders are up on all horizons (three-month, six-month and 12-month) as well as accelerating. But much of that result is only on its recent strength in March. Still, foreign orders have been up year-over-year for three-month running after a series of drops. Whether that stands as a trend will depend on future months' performance. Domestic orders are falling over these same horizons, and while not uniformly decelerating, the three-month growth rate is less than the 12-month growth rate. Real domestic order growth year-on-year has been on a dodgy path for the last four months. Trends seem to be shifting.

German orders rose by 1.9% in March, their strongest gain since June of last year. But the gain came on a 4.3% spurt in foreign orders which only rebounded from a 2.1% drop in February. Domestic orders fell by 1.2% in March. And there is a real schism between domestic and foreign orders and conditions not just a one month runaround. Foreign orders are up on all horizons (three-month, six-month and 12-month) as well as accelerating. But much of that result is only on its recent strength in March. Still, foreign orders have been up year-over-year for three-month running after a series of drops. Whether that stands as a trend will depend on future months' performance. Domestic orders are falling over these same horizons, and while not uniformly decelerating, the three-month growth rate is less than the 12-month growth rate. Real domestic order growth year-on-year has been on a dodgy path for the last four months. Trends seem to be shifting.

Once again we find evidence of Germany extending its run of growth like a vampire living off the life blood of demand in overseas economies. Instead of Germany creating its own demand, Germany is filling orders from other economies while running a huge current account surplus, one that is especially large relative to GDP. Germany also is trying to run a fiscal surplus, further containing its own domestic demand while piggy-backing on demand growth in other countries that themselves are struggling but are less competitive and therefore import from Germany.

German competiveness, boosted by the weak euro, is helping to cement German order and export growth. Orders are advancing, but exports have been cooling.

New orders from countries within the euro area were up by 1.1% in April while orders from outside the euro area spurted by 6.2%.

Domestic sector by sector weakness

The trend for real sector sales shows declines up and down the line in March with manufacturing and mining off by 1.1% led by a 2.5% drop in consumer durables. Capital goods sales fell by 1.2%; intermediate goods sales fell by 1.0%. Real sector sales are decelerating from 12-month to six-month to three-month with manufacturing and mining sales falling on balance over six-month and three-month. Consumer goods sales (both durables and nondurables) also are decelerating on that time line and falling over six-month and three-month. Intermediate goods sales are decelerating and falling on all the time lines. Capital goods sales are contrarily consistently expanding and have accelerated over three-month.

Despite all the month-to-month weakness in the recently completed first quarter, orders are up on balance in Q1 compared to their Q4 average, led by strong gains in foreign orders with domestic orders falling at a sharp 5.4% annual rate. There is a real dichotomy between domestic-sourced and foreign-sourced orders in Germany that is persisting.

Despite all the recent weakness in sales, real sector sales show solid to strong gains all through the sectors in Q1 on average compared to Q4 on average. But the jumping off point for Q2 is very weak. March growth over the Q1 average shows a -4.6% annual rate of change compared to -13.6% pace for consumer durables. Even capital equipment sales will start Q2 in a hole.

The inherited growth calculation looks at the annualized rate of growth in March over the Q1 average level of spending to get a sense of the jumping off point for sales in Q2. In all cases, this jumping off point for sales and domestic orders begins in a hole at the end of Q1 (in March).

On balance, the sector data show a great deal of sector weakness (except capital goods) while orders speak of substantial ongoing domestic weakness. Overall orders are riding high only on foreign demand especially by serving demand outside the euro area. However, after a long period of weakening, the real broadly defined euro exchange rate has moved higher for two consecutive months by a net of 3% year-over-year as of March. This is a marked change for this currency which was falling on this basis year-on-year by 5.9% in November and by 12.1% April, nearly one year ago. The firming up of the euro (for the moment, at least) is taking away some of the competitiveness gained by the euro. But the euro has been falling since 2009 and the degree of backtracking so far is minor. Germany maintains an edge in competitiveness from its low real effective exchange rate and Germany's growth continues to benefit from it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief