Global| Mar 06 2014

Global| Mar 06 2014German Orders Recover and Show Strength

Summary

German orders returned to their expansion path in January. Orders rose by 1.2% in January after slipping by 0.2% in December. Foreign orders rose by 1% while domestic orders advanced by 1.6% in January. Foreign orders rose for the [...]

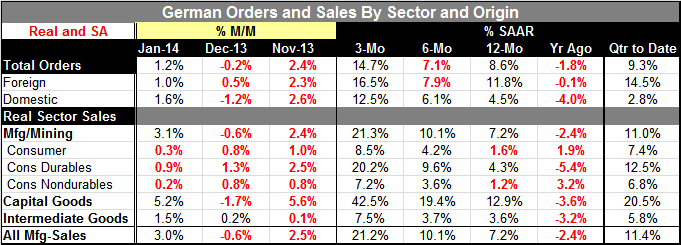

German orders returned to their expansion path in January. Orders rose by 1.2% in January after slipping by 0.2% in December. Foreign orders rose by 1% while domestic orders advanced by 1.6% in January. Foreign orders rose for the third consecutive month while domestic orders rose following a drop a month earlier.

German orders returned to their expansion path in January. Orders rose by 1.2% in January after slipping by 0.2% in December. Foreign orders rose by 1% while domestic orders advanced by 1.6% in January. Foreign orders rose for the third consecutive month while domestic orders rose following a drop a month earlier.

Foreign orders' rate of growth exceeds growth for domestic orders over three-months, six-months and twelve-months. Year-over-year foreign orders are up by 11.8% compared to a 4.5% advance for domestic orders. Year-over-year foreign orders have been exceeding domestic orders with regularity since May of 2012. These statistics are for the country with the largest current account surplus in the world.

In addition to running this persistent huge surplus, Germany's growth is being led predominately by export growth, not by rising domestic demand. Foreign orders are rising faster than domestic orders in nineteen of the last twenty months in terms of year-over-year rates of growth. Germany is sucking domestic demand out of the rest of the world to fire its economy and replacing it with inferior domestic demand growth.

This mix of growth is reflected in German-reported sales growth as well. Sales of capital goods items are soaring, rising by 12.9% year-over-year and by 5.2% (not annualized!) in January. Intermediate goods sales are up by 3.6% over one year. Consumer goods sales are up by just 1.6% over the last twelve months. Germany's hot exports are not giving rise to much domestic stimulus. And a pick-up in German domestic demand would contribute to export growth across the EMU, as other countries could tap into German demand growth. But they can't tap into German supply expansion so Germany's success in servicing foreign demand has no legs except through firing up domestic demand. German domestic growth is hampered as German population growth is working against domestic demand strength.

Germany has become a black hole for the forces of global domestic demand. German firms exploit that demand and take it off-stream- as other countries cannot exploit it after Germany does. When the impact of servicing this demand has its full force back home in Germany, domestic demand does not fire up by all that much.

Germany needs to become a proactive force for growth in the EMU. So long as German exports are growing faster than German imports there is a clear signal that Germany is living off export-led growth at a time when much weaker countries need to increase their output and hire their workers to keep their respective recoveries going. They need to reduce rates of unemployment around the EMU area, rates that tend to dwarf Germany's own rate of unemployment. Since these nations all are locked in the same currency area, EMU members cannot depreciate their currencies to regain lost competitive ground to Germany. Instead their road back to being competitive with Germany is long and hard. Germany will retain most of the advantage it has over fellow EMU members for many years even if those members set their sights and policies on redressing this competitiveness gap now. The process of getting back lost competitiveness is a tough one.

When you are in a currency union, national policies have to be much less about the greedy solution. Germany, for its own sake and prosperity, needs to make sure that its fellow EMU members are growing and prospering or tensions could build in the EMU again. As long as Germany's surplus is large and the gap is getting larger, we know that Germany is doing the euro area no favors.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.