Global| Dec 05 2014

Global| Dec 05 2014German Orders Rebound: Mixed Message

Summary

German new industrial orders in October surged by 2.5%, rising faster than had been expected. The rise follows a 1.1% increase in September. This comes after a period of severe volatility. Despite the rise in orders the Bundesbank has [...]

German new industrial orders in October surged by 2.5%, rising faster than had been expected. The rise follows a 1.1% increase in September. This comes after a period of severe volatility. Despite the rise in orders the Bundesbank has cut its expectation for growth for the year ahead, down to 1%.

German new industrial orders in October surged by 2.5%, rising faster than had been expected. The rise follows a 1.1% increase in September. This comes after a period of severe volatility. Despite the rise in orders the Bundesbank has cut its expectation for growth for the year ahead, down to 1%.

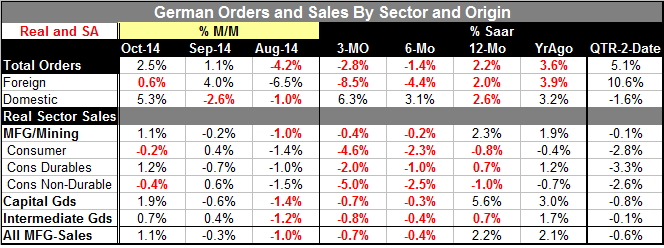

In October orders from foreign sources decelerated rising by 0.6% after gaining 0.4% in September. Orders from domestic sources accelerated rising by 5.3% after the dropping by 2.6% in September.

Sequential growth rates show that order growth is still decelerating. Over 12 months at a growth rate of 2.2%, orders drop to -1.4% over six months and slow again to -2.8% over three months. This degrading trend in growth rates stems from foreign orders which are up 2% over 12 months, down at a 4.4% rate over six months, and plunging at an 8.5% annual rate over three months. Domestic orders were actually accelerating. Domestic orders are up by 2.6% over 12 months at a 3.1% pace over six months and at a 6.3% annual rate over three months.

Foreign orders show clear weakness as they softened in October; they exhibit a clear declining trend to boot. German orders from within the euro-Area in October rose by 0.3% while orders from outside the euro-Area rose by 0.8%. Obviously the euro-Area is not adding much to German order growth and German orders, at least in terms of the trend, are not adding much to the prospects for growth as a member of the euro-Area itself.

However, orders in the quarter to date are growing much more briskly. Much of that stems in the specific pattern of orders with orders declining sharply in August and rising in September, on the last month of the quarter then rising by a brisk 2.5% in October, in the first month of the new quarter. This pattern leaves orders as of the first month of the fourth quarter rising at a 5.1% annual rate over the third quarter average. Foreign orders are rising at a 10.6% annual rate in the new quarter. While domestic orders are falling at a 1.6% annual rate. The quarter to date patterns are, in some sense, the opposite of the sequential growth rate pattern. Since October is only one month of the new quarter and since we have two more months of data to come on stream we should not take these growth rates very seriously.

Real sector sales were uneven in October with the overall manufacturing and mining sales up by 1.1%. Sales to consumers fell by 0.2%. Even though consumer nondurable sales rose by 1.2% sales of consumer nondurables fell by 0.4%, dominating the overall result. Capital goods sales are up a robust 1.9% while intermediate goods' sales rose by 0.7%. However, all the good news goes way over three months as real sector sales are falling in all the sectors. Moreover, sales over three months are falling at a faster rate than over six months in all sectors. And, yes, sales are also falling over six months in all sectors. Year-over-year real sector sales are uneven as they reveal some increases and some declines by sector. But six-month sales are uniformly weaker than all twelve-month growth rates.

The message is that the German economy is indeed weak. The Bundesbank's decision to cut the outlook makes sense- but it makes more headlines coming as it does on a day when industrial orders seem to pick up. . Month-to-month orders figures can be volatile. And this month, despite the rebound, we can see that the trend for orders continues to remain negative.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief