Global| Oct 07 2008

Global| Oct 07 2008German Orders Rebound in Surprise Show of Resiliency

Summary

The German economy shows some resilience in its factory sector in August as orders reverse a string of eight months of declines to rise by 3.6% in August. Overall and foreign orders had previously each fallen for eight months in a [...]

The German economy shows some resilience in its factory sector in August as orders reverse a string of eight months of declines to rise by 3.6% in August. Overall and foreign orders had previously each fallen for eight months in a row. Such a string of negativism does simply go way without some good reason. AND right now we don’t have any reason at all. The upward surprise builds on a similar upward surprise from retail sales in the month. Even so trends in both sectors still point lower. In the case of retail sales, some calendar effects may have helped to boost those sales. In the case of factory orders there appears to be some lumpy orders that constitute ‘one-off’ events leaving us expecting more weakness in the months ahead.

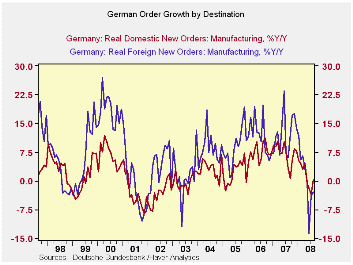

German foreign orders remain in a consistent weak pattern with flatness or sequential slowing in trends well in train. Domestic orders are more resilient actually showing an accelerating profile from 12-months to 6-months to 3-months. This pattern appears to be more the result of some statistical oddity than something that is in sync with the realities of the economic data we have been seeing. The domestic German economy definitely is not accelerating.

Still the MFG sales trends continue to be upbeat for most classes of goods except consumer nondurables. Consumer durables sales jumped in August after a drop in July.

All this may raise some question marks about the future. But, with the euro still overly strong and the financial crisis spreading in Europe, the safest bet is that this month’s buoyancy is an unrepeatable bit of good news. Economic conditions in Germany will continue to get worse.

| German Orders and Sales By Sector and Origin | ||||||||

|---|---|---|---|---|---|---|---|---|

| Real and SA | % M/M | % Saar | ||||||

| Aug-08 | Jul-08 | Jun-08 | 3-MO | 6-Mo | 12-Mo | YrAgo | QTR-to-Date | |

| Total Orders | 3.6% | -1.3% | -2.6% | -1.2% | -0.6% | -1.3% | 4.7% | -7.7% |

| Foreign | 3.5% | -0.3% | -4.5% | -5.5% | -2.8% | -3.0% | 6.1% | -7.3% |

| Domestic | 3.7% | -2.2% | -0.5% | 3.2% | 1.6% | 0.4% | 3.3% | -8.2% |

| Real Sector Sales | ||||||||

| MFG/Mining | 4.1% | -2.4% | -0.2% | 5.3% | 2.6% | 2.2% | 5.8% | -4.0% |

| Consumer | 2.3% | -0.4% | -1.4% | 2.0% | 1.0% | -1.7% | 1.6% | -1.0% |

| Cons Durables | 7.1% | -4.2% | 1.7% | 18.4% | 8.8% | -1.0% | 0.8% | -3.7% |

| Cons Non-Durable | 1.5% | 0.3% | -1.9% | -0.8% | -0.4% | -1.8% | 1.7% | -0.4% |

| Capital Goods | 5.3% | -4.0% | 0.9% | 7.9% | 3.9% | 4.1% | 7.9% | -8.2% |

| Intermediate Goods | 3.5% | -1.7% | -1.0% | 2.9% | 1.4% | 2.1% | 5.6% | -0.8% |

| All MFG-Sales | 4.0% | -2.2% | -0.3% | 5.4% | 2.6% | 2.2% | 5.2% | -3.6% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief