Global| Mar 06 2020

Global| Mar 06 2020German Orders Make Strong Rebound

Summary

German orders rose by 5.5% in January after falling in each of the two previous months. The sharp gain is enough to boost growth positive over both three months and six months and to put orders on an accelerating path. The January [...]

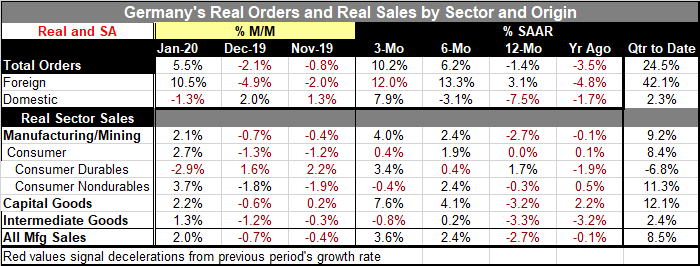

German orders rose by 5.5% in January after falling in each of the two previous months. The sharp gain is enough to boost growth positive over both three months and six months and to put orders on an accelerating path. The January strength is in foreign orders that rose by 10.5% after falling by 4.9% and 2%, respectively, in each of the two previous months. Domestic orders fell in January after rising in December. Both domestic and foreign orders show an improving path from 12-months to six-months to three-months. Growth rates in the quarter-to-date period are explosive.

German orders rose by 5.5% in January after falling in each of the two previous months. The sharp gain is enough to boost growth positive over both three months and six months and to put orders on an accelerating path. The January strength is in foreign orders that rose by 10.5% after falling by 4.9% and 2%, respectively, in each of the two previous months. Domestic orders fell in January after rising in December. Both domestic and foreign orders show an improving path from 12-months to six-months to three-months. Growth rates in the quarter-to-date period are explosive.

Orders were led higher by a 15.1% surge in demand from other countries in the 19-nation euro area. Orders from other countries were up 7.8%. Orders from within Germany declined 1.3%. Germany reported that January's performance was boosted by an above-average number of bulk orders

Real sales by sector also show broad-based gains in January. Manufacturing as well as manufacturing and mining show sales increases. Sector sales are still lower year-on-year in all sectors except for consumer durables. However, sales are up over six months in all categories. Over three months sales are up in all but two sectors or subsectors and that is enough to drive and increase in overall manufacturing sales.

Looking at momentum, we find momentum is negative over 12 months compared to 12 months ago. Over six months momentum is sharper better with sector sales stronger that their 12-month growth rate nearly across the board. Over three months it is a mixed bag with only two sector or subsector advances but still with enough juice to push overall manufacturing sales to acceleration as well.

On balance, the German report is a real surprise. It interrupts a long stretch of weak orders. Year-on-year orders still are falling and they have been dropping for 18 months in a row. Domestic and foreign orders have seen three-month growth rates rise in four of the last seven months. This hint of improvement likely reflects world trade trends at the time that the U.S. and China signed their Phase-One deal and there may have been some lingering optimism. As we move forward, there are going to be more data points affected by the new weakness spawned by the discovery and spread of the coronavirus. The slight pause and the rebound we see in the data this month may only be a fading flash of good news soon to be replaced by dislocation and supply chain interruptions as well as the knock-on effects from the discovery and spread of the coronavirus as well as by the actions taken to contain it…that is until global conditions eventually start to improve again.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief