Global| Jan 06 2017

Global| Jan 06 2017German Orders Fall Sharply in November But Acceleration Pattern Is Still in Place

Summary

German orders fell sharply in November but only after an even larger gain in October, one that in percentage terms was twice the size of the November drop. On balance, orders still carry upward momentum from their October spurt. [...]

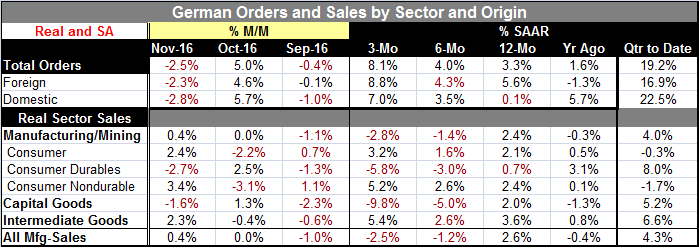

German orders fell sharply in November but only after an even larger gain in October, one that in percentage terms was twice the size of the November drop. On balance, orders still carry upward momentum from their October spurt. Overall orders as well as orders from both domestic and foreign components showed the same pattern of a huge rise in October and a substantial, though lesser, drop in November. As a result, the three-month growth rates for orders are 8.1% annualized overall, 8.8% for foreign orders, and 7.0% for domestic orders. Despite the large November drop, German orders are still hot and carry an accelerating uptrend.

German orders fell sharply in November but only after an even larger gain in October, one that in percentage terms was twice the size of the November drop. On balance, orders still carry upward momentum from their October spurt. Overall orders as well as orders from both domestic and foreign components showed the same pattern of a huge rise in October and a substantial, though lesser, drop in November. As a result, the three-month growth rates for orders are 8.1% annualized overall, 8.8% for foreign orders, and 7.0% for domestic orders. Despite the large November drop, German orders are still hot and carry an accelerating uptrend.

The sequential growth rates show overall order acceleration from 12-month to six-month to three-month and the same accelerating pattern for foreign and domestic orders. In the quarter-to-date, a slightly different arrangement for growth calculations than the three-month growth rate, all series are growing at annualized growth rates ranging from 16.9% to 22.5% in the quarter that has one more month to go.

Real sector sales are much slower in November and over three months. The series for real manufacturing sales has a 0.4% rise in November and an annual rate drop at a -2.8% pace over three months. But year-over-year the sales growth rate and the orders growth rate are relatively close with orders overall up by 3.3% over 12 months compared to sales up at a 2.6% pace. Historically, the year-on-year pace of real sector sales tracks closely with real orders growth. It's possible that the late surge in orders simply closes a gap that had developed between sales and orders and reflects make up in an order series that had lagged.

The closeness of the two growth rates over 12 months leads me to look at the two series a bit differently. The surge in growth no longer looks like some pull away acceleration. Instead it looks like a period of volatility and looks as though the two series on orders and sales remain closely united. Historically, orders generally have moved ahead of any acceleration or deceleration in sales. So there could be some acceleration afoot. It's just too soon to tell how significant that might be. The life in the orders series does dovetail nicely with the pick-up in some of the manufacturing PMI readings for Germany from Markit. But even those Markit readings are relatively constrained compared to Germany's history for that series. As yet, there are no clear signals, only suggestions.

Some context for growth

Other reports on the day showcase some back sliding in German and in EMU retail sales. The recent Global PMI readings highlight that there has been some pick up in strength among the developed economies while the developing and emerging economies are lagging. The U.S. employment report today was less glowing, showing ongoing job growth, but nothing spectacular with a step back from the super-low unemployment rate reported in November, moderate wage gains and modest increase in hours worked. The U.S. jobs data do not seem to offer a snap shot of an economy in an acceleration phase. Meanwhile, data from the U.K. have been very upbeat, but there continues to be concern that its buoyancy can't last and that there is another shoe yet to fall over Brexit. U.K. manufacturing had continued to do well and 2016 was a record for vehicle sales in the U.K. In Asia, China's two PMI reports give us conflicting evidence on its momentum, but both showed that manufacturing is expanding. Japan registered expansion in manufacturing as well in its PMI. The developed portion of the global economy is back on positive if not solid footing. The notion of acceleration for the global economy, however, still is not resolved.

Fears on all fronts

However, policymakers are in a conundrum and still worry. As someone that grew up in the Midwest, let me give you a real-life example of the concerns that the central bankers have especially at the U.S. central bank. They are like a couple of guys trying to push their stuck car, spinning wheels and all, out of a snowbank in winter. They desperately work to get the car unstuck. But they also worry how far it's going to skid down the slope of the icy road once it has even the smallest momentum and gets pushed back on track. Central bankers are afraid both of keeping their economies stuck in a low growth path and also of revival, fearing that revival could unexpectedly accelerate out of control. It's not a situation that breeds much confidence.

The policy conundrum

I get the sense that markets are beginning to be put off by this reluctance to be successful. Policy-makers fudge their view by saying policy is data dependent. But after months of talking about gradualism, the Fed is now raising the prospect that gradualism may no longer be appropriate. The Bundesbank's Jens Weidmann is focused on ECB policy as determined only by inflation as OPEC is hiking prices. Yet, EMU growth is hardly strong or even reliable. How are markets supposed to take that? Moreover, success in the form of reviving growth is far from assured despite recent central bank prevarications. What we are witnessing in policymakers is their inherent bias of being concerned that (1) they have overdone the stimulus, (2) that rates are too low for too long, (3) that the unemployment rate is too low, and (4) that it or something else will generate inflation. With policy perhaps on the verge of success they are so afraid of what comes next that they are afraid to follow through and provide that last push. And every time they have acted this way in the past, it has turned out that they have done too little...not too much. Is that the mistake we are going to revisit in 2017? Are central bankers going to lose their nerve on the brink of success? Or will this be the year that growth finally emerges from the shadows? And if it does, will it slip into overdrive and will the central banks have to chase it down to control it?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief