Global| Oct 08 2013

Global| Oct 08 2013German Orders Fall for the Second Month in a Row

Summary

There is some consternation this morning that German orders fell in August. The drop of 0.3% was small but it makes the second drop in a row and that reduces the year-over-year growth rate to 3%. Should we be worried? While I remain [...]

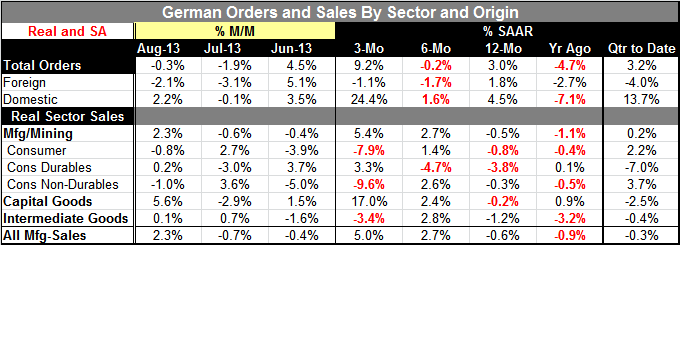

There is some consternation this morning that German orders fell in August. The drop of 0.3% was small but it makes the second drop in a row and that reduces the year-over-year growth rate to 3%. Should we be worried?

There is some consternation this morning that German orders fell in August. The drop of 0.3% was small but it makes the second drop in a row and that reduces the year-over-year growth rate to 3%. Should we be worried?

While I remain suspect of the strength of the euro-recovery, the German figure today is not evidence of any new problems. Since September 2010 the German orders headline has fallen month to month in 19 out of those 36 months. That means orders have been rising and falling every other month on average for the last three years (and longer, actually) with, in fact, a few more monthly declines than increases. This is the third pair of back-to-back declines over the period and there was one episode of FOUR declines in a row. In short, there is nothing new here.

German domestic orders are looking even more solid in the wake of this report. They are rising on the month, and are accelerating, advancing at a 24% annualized rate over 3-months. Domestic orders are also rising at a 13.7% rate in the quarter to date, as foreign orders are falling at a 4% annual rate.

If we take the German orders report as a statement about the German economy, that economy seems to be doing just fine. If we want to broaden it to a statement about the eurozone, it is no longer so upbeat. German orders from the eurozone fell by 2.9%.

Germany has an economy geared to run on weak demand. The German economy is the most efficient in Europe and German firms will under-sell just about all the competition. So, if European growth is weak, we can expect German factories to be servicing most of it, leaving the scraps for the less efficient. A rising tide in Europe will lift German boats; the rest may find that they are left grounded on shore unless the tide rises by enough. Right now demand conditions in Europe are not exactly looking robust.

The German orders data reflect this dilemma with strong domestic sales/orders and weak foreign orders. German domestic sales are weak for consumption but are typically strong for capital goods. Capital goods sales are rising at a 17% annual rate in the most recent three-months.

While historically we might find a strong correlation between German performance and the rest of Europe, we should be guarded about expecting the same in the future. The German economy is not only very competitive but its fiscal state is much better than the rest of the eurozone. However, in viewed in conventional terms one thing to ponder is that German domestic orders are rising faster than foreign orders, and that has not historically been a good development if it is sustained. The situation is ripe for Germany to make even more separation from the rest of Europe. And if that happens, tensions in the eurozone could rise. We need to watch the rest of Europe to see if the rest of the eurozone's incipient pick-up can be sustained in the face of all the problems its nations must deal with. Germany may turn out to be an exception instead of a bellwether. Its rising ratio of domestic orders to foreign orders is a hint that such a development may be progress even now.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief