Global| Mar 07 2016

Global| Mar 07 2016German Orders Erode in January on Domestic Weakness

Summary

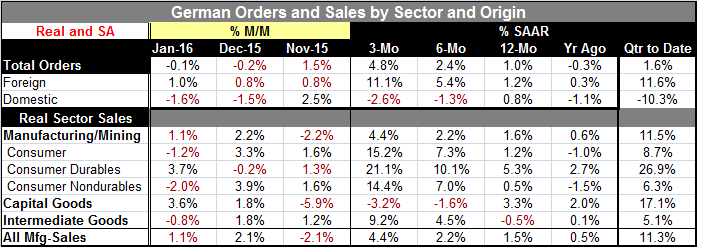

German orders fell in January for the second straight month. However, each month the declines were relatively small, and together, they fail to offset the 1.5% order gain in November so that the three-month change is still positive. [...]

German orders fell in January for the second straight month. However, each month the declines were relatively small, and together, they fail to offset the 1.5% order gain in November so that the three-month change is still positive. Over three months orders are up at a 4.8% pace, up from 2.4% over six months which also was up from 1% over 12 months. Orders are expanding and accelerating sequentially despite the two-month drop.

German orders fell in January for the second straight month. However, each month the declines were relatively small, and together, they fail to offset the 1.5% order gain in November so that the three-month change is still positive. Over three months orders are up at a 4.8% pace, up from 2.4% over six months which also was up from 1% over 12 months. Orders are expanding and accelerating sequentially despite the two-month drop.

German orders: A tale of two trends

German orders are fighting two opposite trends. Foreign orders are accelerating sharply sequentially while domestic orders are weakening sequentially. So far, foreign order strength is dominating the trend based on stronger shorter term rates of growth. However, year-over-year, the growth in foreign and domestic orders is nearly identical at about 1% (i.e., 1.2% foreign; 0.8% domestic). The year-over-year growth rate in foreign orders has just turned positive.

Sector sales are mostly strong with one glaring omission

Real sector sales trends generally support the acceleration trend but with one glaring omission. Capital goods trends are decelerating, showing sales dropping over three months and over six months. Other sectors show both growth and acceleration. Normally the preponderance of strength would simply make that the end of the story. But for Germany, capital goods tend to be at the core of its strength so the progressive weakness and deceleration there gives me pause. There are anecdotal stories about how small German firms are worried about the outlook and may be cutting back investment. These stories stress how small firms are so very important to German export success. All of this simply muddies the waters on what we should be thinking about the future.

Investor sentiment erodes

The euro area Sentix index dropped in March. It is an index of investor confidence and now has fallen for three consecutive months. The recent PMI data were showing weakness in manufacturing and services. For the EMU, both manufacturing and services weakened. In Germany, the total index weakened with manufacturing lower and services slightly higher. Global trends in February show much more weakness.

The outlook

The global outlook is in flux. At the recent G20 meeting (last weekend), the IMF argued for more stimulus and said it could be lowering its outlook again. This weekend China cuts its growth expectations and forward plan from 7% to a 6.5% to 7% range. The JPMorgan global services index has been weaker only 6.5% of the time since 2008. Oil prices are firming but oddly as the oil glut has worsened. The oil price rebound may be wholly technical, but for now it has been a basis for equity markets to rally. In truth, the strengthening in equity markets has seemed without much foundation as well.

BIS warns...policy on thin ice?

Over the weekend, the BIS warned of the danger of negative rates. The BOJ said it was studying the impact of negative rates, having already adopted the policy. We live in an age of experimental monetary policy. The BIS has warned that markets may be losing their faith in central banks' healing power. In the U.S., diplomats are getting complaints about the campaign language of Donald Trump. It is a world turned upside down in many ways. Investors wonder if after a strong Friday U.S. job report, the Fed rate hike signal is turned back on. No one knows and that statement applies to a lot of things. We seem to know less about how the word works and what is happening than we thought we did.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief