Global| Mar 08 2018

Global| Mar 08 2018German Orders Drop Sharply in January and Crimp Momentum

Summary

German orders are still growing rapidly after their sharp plunge in January. Year-on-year growth is 8.3% overall, 9.5% for foreign orders and 6.6% for domestic orders. But momentum has been sharply reduced with three-month and six- [...]

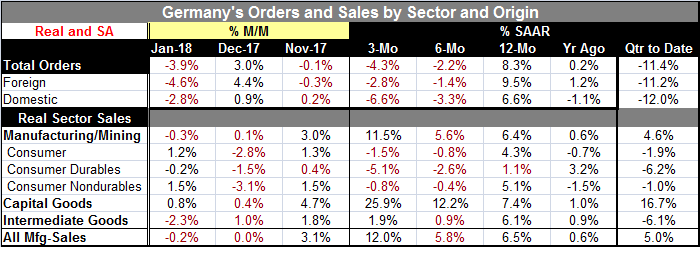

German orders are still growing rapidly after their sharp plunge in January. Year-on-year growth is 8.3% overall, 9.5% for foreign orders and 6.6% for domestic orders. But momentum has been sharply reduced with three-month and six-month growth rates negative for total orders as well as foreign orders and domestic orders. Sequential growth rates show deceleration in progress, but we know that is less a statement about trend and more the result of the one-month plunge which may or may not reverse out next month.

German orders are still growing rapidly after their sharp plunge in January. Year-on-year growth is 8.3% overall, 9.5% for foreign orders and 6.6% for domestic orders. But momentum has been sharply reduced with three-month and six-month growth rates negative for total orders as well as foreign orders and domestic orders. Sequential growth rates show deceleration in progress, but we know that is less a statement about trend and more the result of the one-month plunge which may or may not reverse out next month.

Sales also show some weakness, dropping moderately in January after a weak December gain and flatness in manufacturing. Sales show a pattern of ongoing expansion on all horizons. There is somewhat disturbing weakness (1.1% growth over 12 months) for durable goods sales and declines over six months and six months have eaten away at previous strength. Overall consumer sales are still expanding as are nondurable goods sales but both still show these vexing three-month and six-month declines. This is something to bear in mind. Globally, it is the consumer sector that has been weak and it is hard to imagine an expansion that is going to gain breadth without a strong contribution from the consumer. We have seen some weakness in U.S. consumer spending and in vehicle sales as well as weakness in EMU-area retail sales and in U.K. car sales. There has been enough to this spottiness to not ignore it.

Quarter-to-date figures are weak because of the sharp declines in orders in January. It is too early to tell if that will crimp Q1 strength, but at the very least it is starting Q1 off in a hole from which it must rebound even to achieve moderate results.

Orders always are a volatile series. It is hard to know what to do with sharp changes when they appear. Most often there is some mean reversion at work that has a sharp gain followed by a reversing decline and vice versa. But sometimes a sharp move simply sets a new level in place and the move signals a change in trend. This will bear watching.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief