Global| Sep 05 2013

Global| Sep 05 2013German Orders Deflate..for a Moment...Longer?

Summary

The month-to-month drop in German orders in July of 2.7% is a bit of a tempest in a teapot. The decline comes after an outsized 5% jump in June. The three-month growth rate for orders is still a very robust 6.7% at an annual rate. [...]

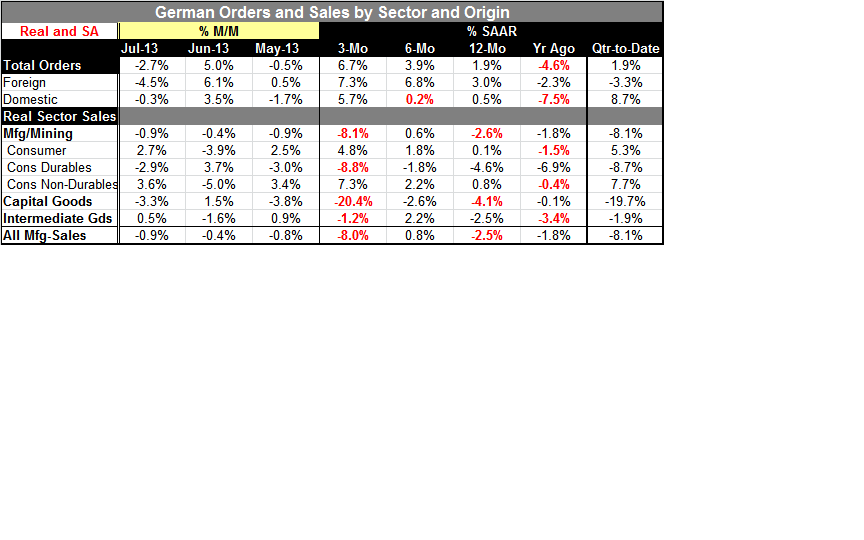

The month-to-month drop in German orders in July of 2.7% is a bit of a tempest in a teapot. The decline comes after an outsized 5% jump in June. The three-month growth rate for orders is still a very robust 6.7% at an annual rate. German orders show an acceleration with a three-month pace above the 3.9% six-month pace and that 3.9% pace above the 1.9% twelve-month pace. That's a classic configuration of growth accelerating. But is it dependable?

The month-to-month drop in German orders in July of 2.7% is a bit of a tempest in a teapot. The decline comes after an outsized 5% jump in June. The three-month growth rate for orders is still a very robust 6.7% at an annual rate. German orders show an acceleration with a three-month pace above the 3.9% six-month pace and that 3.9% pace above the 1.9% twelve-month pace. That's a classic configuration of growth accelerating. But is it dependable?

Foreign orders have been very volatile recently. In July foreign orders collapsed, falling by 4.5%. However, before you start wondering about what happened to the global revival, recognize that June orders had posted a 6.1% increase. Over three months foreign orders are rising at a 7.3% annual rate a bit stronger than their 6.8% pace over six months and both of those are much stronger than the 3% annual rate over 12 months. All horizons signal growth.

German domestic orders also slightly deflated in July falling by a small -0.3%. That followed a sharp increase in orders of 3.5% in June. Domestic orders are up at a very firm 5.7% annual rate over three months. However, that three-month growth rate is up from 0.2% over six months and 0.5% over 12- months. While the performance indicates a clear acceleration over three months (and relative weakness and flatness from 12-months to six months) we also know that the three-month growth rates are fickle.

Compare the path of domestic orders to that of foreign orders. What's clear is that foreign orders, while volatile over the last two months, just like domestic orders, are carrying much more momentum over broader periods of time. While it's possible to interpret the domestic report as saying that domestic orders are just beginning to pick up steam, it is also quite reasonable to interpret the domestic orders as being volatile and not having earned their stripes in terms of confirming a true pick-up since the six-month growth rate is near zero and the twelve-month growth rate is not much better than that. Moreover, when we look at domestic and foreign orders in tandem, we find that domestic orders are digging out of a very deep hole; a year ago they were declining by 7.5% year-over-year in July while foreign orders were only falling by 2.3% year-over-year. Still, domestic orders can't sustain strength from that weak base.

The sequential growth rates are important for several different reasons. One of them, of course, is to assess whether growth is picking up or not. Another is to assess if the changing growth that we see over a shorter horizon is confirmed by the trend over the longer horizons. For foreign orders this confirmation appears to be in place. For German domestic orders it seems to be lacking.

German real sector sales fell in July by 0.9% and have dropped for three months in a row. Real sector sales in Germany are falling at an 8.1% annual rate over three months, rising by 0.6% at an annual rate over six months, and falling by 2.6% over 12 months. These are not very encouraging figures from the standpoint of assessing domestic demand. Sales of consumer goods are up after having some months of fairly volatile behavior. There, growth shows acceleration from 12 months to six months to three months; the three-month pace is up to 4.8% at an annual rate. However, that comes with a marked divergence between what's going on with consumer durables and nondurables, with nondurables (oddly) showing relatively more strength recently. The capital goods sector that tends to be the backbone of the German economy shows sales falling by 3.3% in July and rising by 1.5% in June after having fallen by 3.8% in May. Putting all that together, that's a -20.4% annual rate decline over three months. It's not so bad over six months at only a -2.6% annual rate of decline, but over 12 months the decline is at a -4.1% annual rate. This is not a very good assessment of demand for the German economy. Intermediate goods sales rose by 0.5% in July but are still falling at a 1.2% pace over three months rising at a 2.2% annual rate over six months and falling by 2.5% over 12 months.

We have seen the PMI data for Europe in August and from that we know the euro-Zone continues to mark progress. However, demand in the German economy doesn't seem quite so robust. This gets back to a point that we keep making about the German economy not being a locomotive. The German economy typically is being led by capital goods sales which are fueled by exports and therefore by foreign demand. That means, as Europe begins to recover, Germany is going to take; it's not going to give.

We see that pattern reflected in orders where German foreign orders are growing faster than German domestic orders over three months, over six months and over 12 months. Despite that clear set of trends there is a quirk in the data that has foreign orders in the quarter-to-date weaker than domestic orders. In the quarter to date foreign orders are falling by 3.3% at an annual rate while domestic orders are surging at 8.7% annual rate. This is just an artifact of how you cut the data up around the end of the quarter. The current quarter-to-date calculation is at odds with all the other trends. Also German sales in the current quarter-to-date are falling at a better than 8% annual rate led by a nearly 20% annual rate decline in capital goods sales.

The decline in German orders in July also appears to be an artifact of monthly data and monthly data patterns. The more disturbing element is the continued lagging behavior of the German domestic economy in the face of what appears to be somewhat robust foreign order growth. Germany continues to have soft spots in its economy and the rest of the euro-Zone has not so clearly turned the corner. Oh, there is progress in the rest of Europe, but it does not have good footing.

While there have been some countries posting stronger export figures, it is not exactly clear yet to whom everyone is exporting. However, it's good to see that there some trade revival. But, trade revival cannot persist unless there are persisting increases in domestic demand somewhere. And when foreign exports exploit that domestic demand the stimulative effects of that domestic demand on the economy that generates it are siphoned off to the economy that benefits from the export-led growth. That's the paradox of Germany being the strong economy in Europe. It's the strong economy but it feeds off growth in its fellow members that are struggling and, in many cases, are still under the yoke of austerity and need to keep all the domestic demand that they can generate.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief