Global| Mar 08 2019

Global| Mar 08 2019German Orders Decline Again

Summary

In what has proved to be a ravaging week for markets and for the global economy and many individual forecasts, the German industrial orders series is at risk of getting a 15-yard penalty for piling on. German industrial orders fell by [...]

In what has proved to be a ravaging week for markets and for the global economy and many individual forecasts, the German industrial orders series is at risk of getting a 15-yard penalty for piling on.

In what has proved to be a ravaging week for markets and for the global economy and many individual forecasts, the German industrial orders series is at risk of getting a 15-yard penalty for piling on.

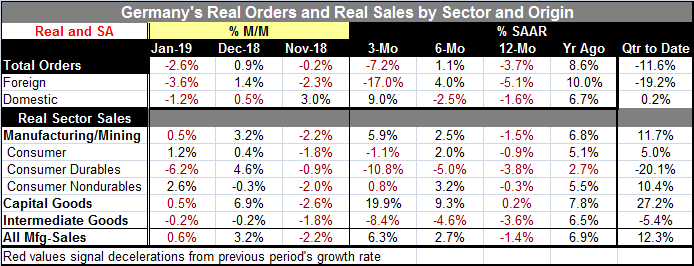

German industrial orders fell by a large 2.6% in January, a less devastating drop that it might have been in the wake of the sharp upward revision to December orders which previously had logged a decline. Still, it's a weak report and another in a series of disappointing assessments of growth in Europe. Orders fell 2.6% overall, by 3.6% from foreign sources and by 1.2% for domestic sources.

However, there is not a pattern of sales implosion or deceleration. For overall orders and foreign orders, sales accelerate over six months compared to 12 months then show negative growth over three months. For domestic orders, growth deteriorates over six months compared to 12 months, but then orders gain over three months at a 9% annual rate. So while there is clear weakness for orders, the pattern for deterioration is more equivocal. In the quarter-to-date, total orders are falling at an 11.6% annual rate as foreign-sourced orders fall at a 19.2% annual rate with a tiny offsetting gain at a 0.2% pace for domestic orders.

Real sales showed their second gain in a row, rising by 0.5% in January after a large, 3.2%, gain in December. Manufacturing alone showed similar gains for two months in a row. And manufacturing sales are up at a strong 12.3% annual rate in the quarter-to-date. QTD capital goods sales are extremely strong, rising at a 27.2% annual rate. Sequentially, capital goods sales are exploding as their 12-month pace of 0.2% yields to a 9.3% pace over six months and then a 19.9% annualized rate over three months. Consumer goods sales have no discernable pattern while intermediate goods sales are very weak, contracting on all horizons as well as sequentially slowing!

In contrast to the strength in real sector sales, real orders by sector show a lot of weakness. Orders for intermediate goods dropped 1.1% in January and those for capital goods plunged 3.6%. Orders for consumer goods decreased by 1.4%. Orders from within the euro area fell by 1.1% in January while orders from outside the euro area fell by 4.2%.

Recoiling from the shock-of-the-week

The highlight for this week was the sharp cut in forecast by the OECD followed by a very sharp reduction in the outlook by the ECB coupled with an ECB policy reversal that shook markets. In fact, the ECB policy announcement and forecast shift took markets by surprise that the reaction was not a positive one to the restart of the ECB loan program but rather a negative reaction to the sharp reduction in the ECB forecast. As a result, the euro took a pounding on exchange markets as well.

Asian trade trends: The Baltic dry goods index continues to show deteriorating shipping trends. Today China reported an extremely sharp drop in its exports with Taiwan reporting the fourth consecutive month of its own export declines. In Taiwan, exports are off by 8.8% year-on-year while imports are lower by 19.7% over 12 months. China's exports posted their largest drop in three years with exports falling by 20.7% year-on-year – this was shocking compared to the 9.1% gain for exports in January. China's imports also fell by 5.2%. Even though there are lunar year shifts in comparisons at work here and trade flows are very much affected by the timing of the lunar year, once adjusted the lunar shift, trade flows in China appear much weaker than expected. Japan also reported export results for January that show an export drop of 6.7% year-on-year.

Asian trade trends: The Baltic dry goods index continues to show deteriorating shipping trends. Today China reported an extremely sharp drop in its exports with Taiwan reporting the fourth consecutive month of its own export declines. In Taiwan, exports are off by 8.8% year-on-year while imports are lower by 19.7% over 12 months. China's exports posted their largest drop in three years with exports falling by 20.7% year-on-year – this was shocking compared to the 9.1% gain for exports in January. China's imports also fell by 5.2%. Even though there are lunar year shifts in comparisons at work here and trade flows are very much affected by the timing of the lunar year, once adjusted the lunar shift, trade flows in China appear much weaker than expected. Japan also reported export results for January that show an export drop of 6.7% year-on-year.

European reports: German orders did disappoint today. And while there has been a weight of bad news and a trend to slower growth across Europe, there are also reports that buck the bad-news-trend. In January in Europe, French manufacturing IP gained 1%, Italian manufacturing IP gained 1.2%, Spain's volatile manufacturing IP index gained 7.1%, while Ireland, Greece and Portugal all logged output increases. Among the early European reports, only Norway reported a decline in manufacturing output in January and that was only at -0.2%. Still, it's true that Italy, Ireland and Portugal all show IP declines over three months, six months and 12 months. European trends continue to point lower, but the monthly reports are not collapsing and some are providing some pushback. And so far, there is enough pushback to keep the real pessimists at bay.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief